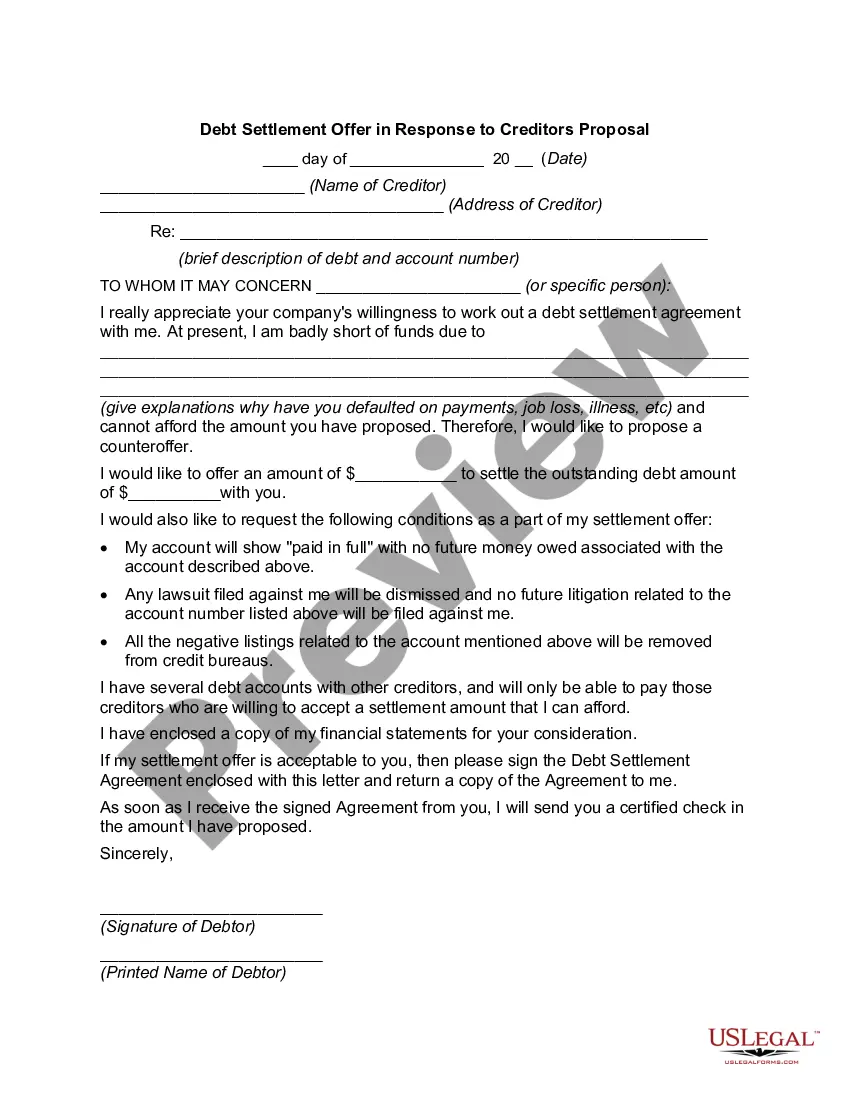

Chicago Illinois Debt Settlement Offer in Response to Creditor's Proposal: When faced with mounting debt and financial hardships, individuals in Chicago, Illinois often seek out debt settlement options to find a feasible solution to their situation. One such option is the Chicago Illinois Debt Settlement Offer in Response to Creditor's Proposal. A Debt Settlement Offer is a negotiation process between a borrower and their creditors to reach a mutually acceptable agreement on the repayment of owed debt. In Chicago, Illinois, this offer is a response to a proposal put forward by the creditor regarding a debtor's outstanding debts. The purpose of this Chicago Illinois Debt Settlement Offer is to present a counterproposal that aims to settle the debt for less than the initial owed amount, providing a debtor with an opportunity to repay their debts in a more manageable way. This offer serves to alleviate the debtor's financial burden while ensuring that creditors receive a portion of the debt owed. Different types of Chicago Illinois Debt Settlement Offers in Response to Creditor's Proposal may exist, targeting various types of debts or financial situations. These may include: 1. Credit Card Debt Settlement Offer: This type of settlement offer focuses on negotiating with credit card companies to reduce outstanding credit card debts. It allows Chicago individuals to potentially pay a reduced amount or establish a repayment plan that suits their financial capacity. 2. Medical Debt Settlement Offer: This settlement offer pertains to outstanding medical bills and aims to negotiate a lower amount or an affordable payment plan that accommodates a debtor's financial situation. This offer enables individuals struggling with medical debts in Chicago, Illinois, to resolve their obligations without further strain on their finances. 3. Personal Loan Debt Settlement Offer: When faced with personal loan debts, individuals in Chicago, Illinois, can respond to a creditor's proposal with a personalized settlement offer. This type of offer seeks to renegotiate the terms, potentially reducing the principal amount, lowering interest rates, or restructuring the repayment plan. The Chicago Illinois Debt Settlement Offer in Response to Creditor's Proposal serves as a valuable tool for individuals seeking debt relief. It allows debtors to assert their financial stability and negotiate more favorable terms with creditors, alleviating the burden of overwhelming debt. By exploring debt settlement options, Chicago residents can take proactive steps towards financial freedom and a brighter future.

Chicago Illinois Debt Settlement Offer in Response to Creditor's Proposal

Description

How to fill out Chicago Illinois Debt Settlement Offer In Response To Creditor's Proposal?

Whether you plan to start your company, enter into a deal, apply for your ID renewal, or resolve family-related legal issues, you need to prepare specific documentation corresponding to your local laws and regulations. Finding the correct papers may take a lot of time and effort unless you use the US Legal Forms library.

The service provides users with more than 85,000 professionally drafted and verified legal templates for any individual or business occurrence. All files are grouped by state and area of use, so picking a copy like Chicago Debt Settlement Offer in Response to Creditor's Proposal is quick and simple.

The US Legal Forms website users only need to log in to their account and click the Download key next to the required template. If you are new to the service, it will take you a couple of additional steps to obtain the Chicago Debt Settlement Offer in Response to Creditor's Proposal. Adhere to the instructions below:

- Make certain the sample fulfills your individual needs and state law requirements.

- Look through the form description and check the Preview if available on the page.

- Make use of the search tab specifying your state above to find another template.

- Click Buy Now to get the file when you find the correct one.

- Choose the subscription plan that suits you most to proceed.

- Log in to your account and pay the service with a credit card or PayPal.

- Download the Chicago Debt Settlement Offer in Response to Creditor's Proposal in the file format you require.

- Print the copy or complete it and sign it electronically via an online editor to save time.

Forms provided by our website are reusable. Having an active subscription, you are able to access all of your previously purchased paperwork at any moment in the My Forms tab of your profile. Stop wasting time on a endless search for up-to-date formal documentation. Join the US Legal Forms platform and keep your paperwork in order with the most extensive online form collection!

Form popularity

FAQ

Typical debt settlement offers range from 10% to 50% of what you owe. The longer you allow debt to go unpaid, the greater your risk of being sued. Creditors are under no obligation to reduce your debt, even if you are working with a reputable debt settlement company.

It depends on what you can afford, but you should offer equal amounts to each creditor as a full and final settlement. For example, if the lump sum you have is 75% of your total debt, you should offer each creditor 75% of the amount you owe them.

While it's generally better to settle a debt before there is a judgment, in the event you don't have such a luxury, you should aim to pay 50% or less of your unsecured debt. Most creditors are willing to take 30% to 50%.

Paid in full means the remaining balance of your debt, including interest, was paid off. Paying in full is an option whether your account is current, past due or in collections. It's better to pay in full than settle in full when it comes to paying off debt.

Two Options for Taking the Settlement Offer Read the settlement offer carefully or have an attorney review the offer to be sure it's legally binding ? that the creditor or collector can't come after you for the remaining balance at some point in the future. Or, you can even try to negotiate a lower settlement.

Typically, a creditor will agree to accept 40% to 50% of the debt you owe, although it could be as much as 80%, depending on whether you're dealing with a debt collector or the original creditor. In either case, your first lump-sum offer should be well below the 40% to 50% range to provide some room for negotiation.

Offer a specific dollar amount that is roughly 30% of your outstanding account balance. The lender will probably counter with a higher percentage or dollar amount. If anything above 50% is suggested, consider trying to settle with a different creditor or simply put the money in savings to help pay future monthly bills.

Start by offering cents on every dollar you owe, say around 20 to 25 cents, then 50 cents on every dollar, then 75. The debt collector may still demand to collect the full amount that you owe, but in some cases they may also be willing to take a slightly lower amount that you propose. A payment plan.

Your creditors do not have to accept your offer of payment or freeze interest. If they continue to refuse what you are asking for, carry on making the payments you have offered anyway. Keep trying to persuade your creditors by writing to them again.

Aim to Pay 50% or Less of Your Unsecured Debt If you decide to try to settle your unsecured debts, aim to pay 50% or less. It might take some time to get to this point, but most unsecured creditors will agree to take around 30% to 50% of the debt. So, start with a lower offer?about 15%?and negotiate from there.

Interesting Questions

More info

When a creditor makes a claim, the borrower is supposed to prove that he or she actually has this money in the account. If the creditor can show that you have no savings, you can't refute the claim. In the case of Havarti Student Loan Refunds, you won't have to repay anything! The creditor can get your money and sue you without proving your identity. The burden of proof stays with the creditor. Step Three: Make the Claim! Once you make the claim, if it is approved by the federal government, you qualify to have the payment paid to the creditor. If the claim isn't approved, the creditor goes to court with your signature attesting to your existence. That's what's important: your signature. If the creditor shows you an invoice for the payment, and you don't sign it, you're out of luck. Be prepared! If you owe Havarti Student Loan Refunds now, you can avoid being sued and get a refund.

Disclaimer

The materials in this section are taken from public sources. We disclaim all representations or any warranties, express or implied, as to the accuracy, authenticity, reliability, accessibility, adequacy, or completeness of any data in this paragraph. Nevertheless, we make every effort to cite public sources deemed reliable and trustworthy.