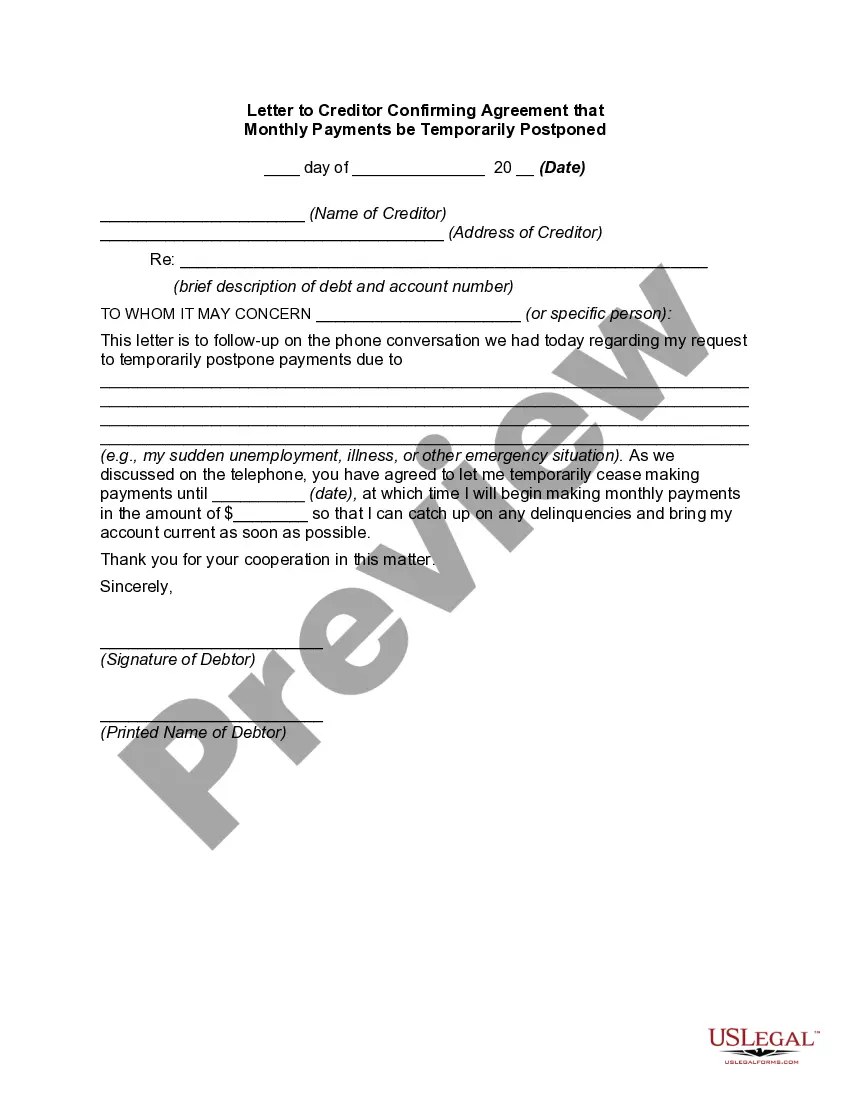

Newark New Jersey Letter to Creditor Confirming Agreement that Monthly Payments be Temporarily Postponed

Category:

State:

Multi-State

City:

Newark

Control #:

US-1115BG

Format:

Word;

Rich Text

Instant download

Description

Section 368(A)(1) of the Internal Revenue Code of 1986 outlines a format for tax treatment to reorganizations, as described in the Internal Revenue Code of 1986. These reorganization transactions, however, have to meet certain legal requirements to classify for favorable treatment. Additionally, there has been further precedent outside from the codified requirements that have developed in case law. A Type A reorganization allows the buyer to use either voting stock or nonvoting stock, common stock or preferred stock, or even other securities. A Type A reorganization must fulfill the continuity of interests requirement. That is, the shareholders in the acquired company must receive enough stock in the acquiring firm that they have a continuing financial interest in the buyer.