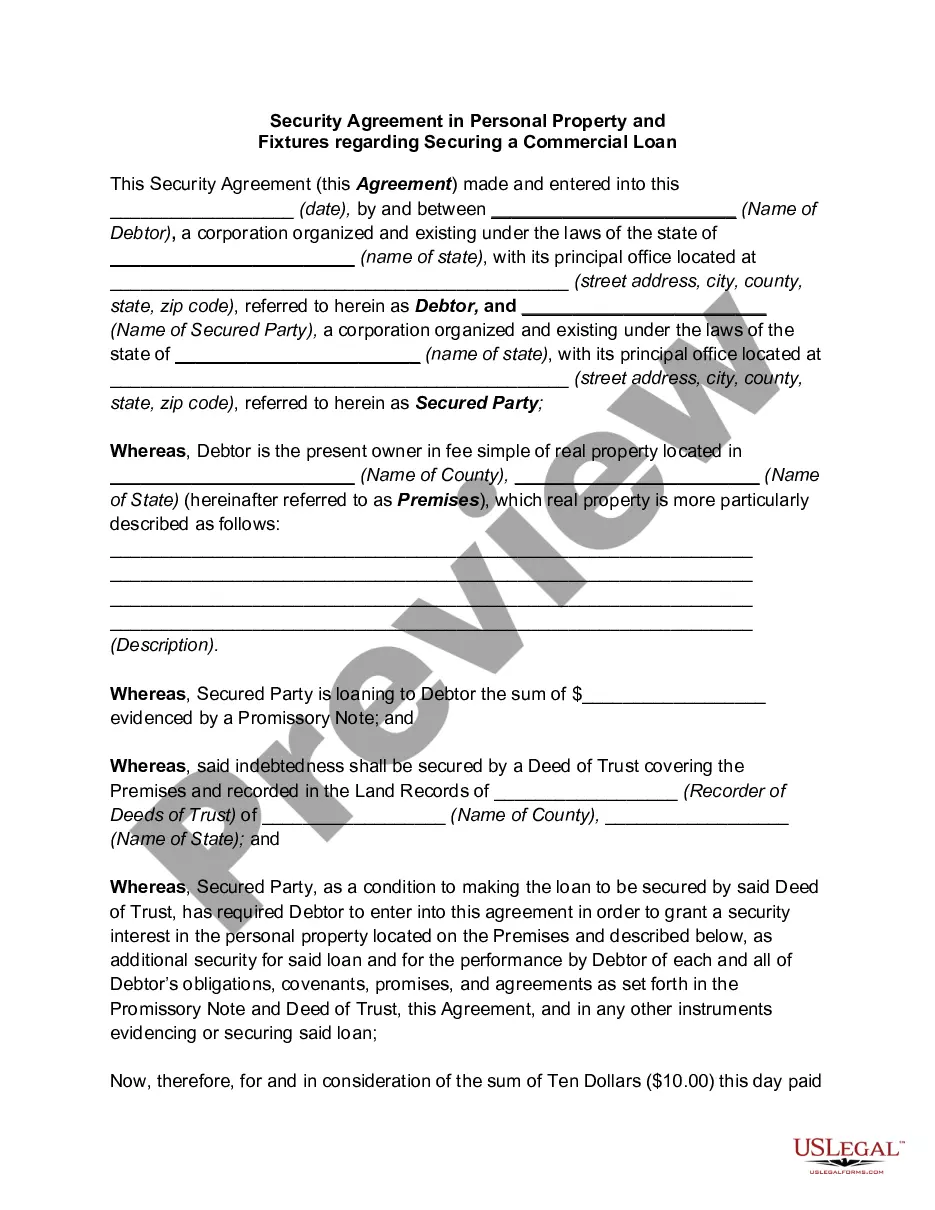

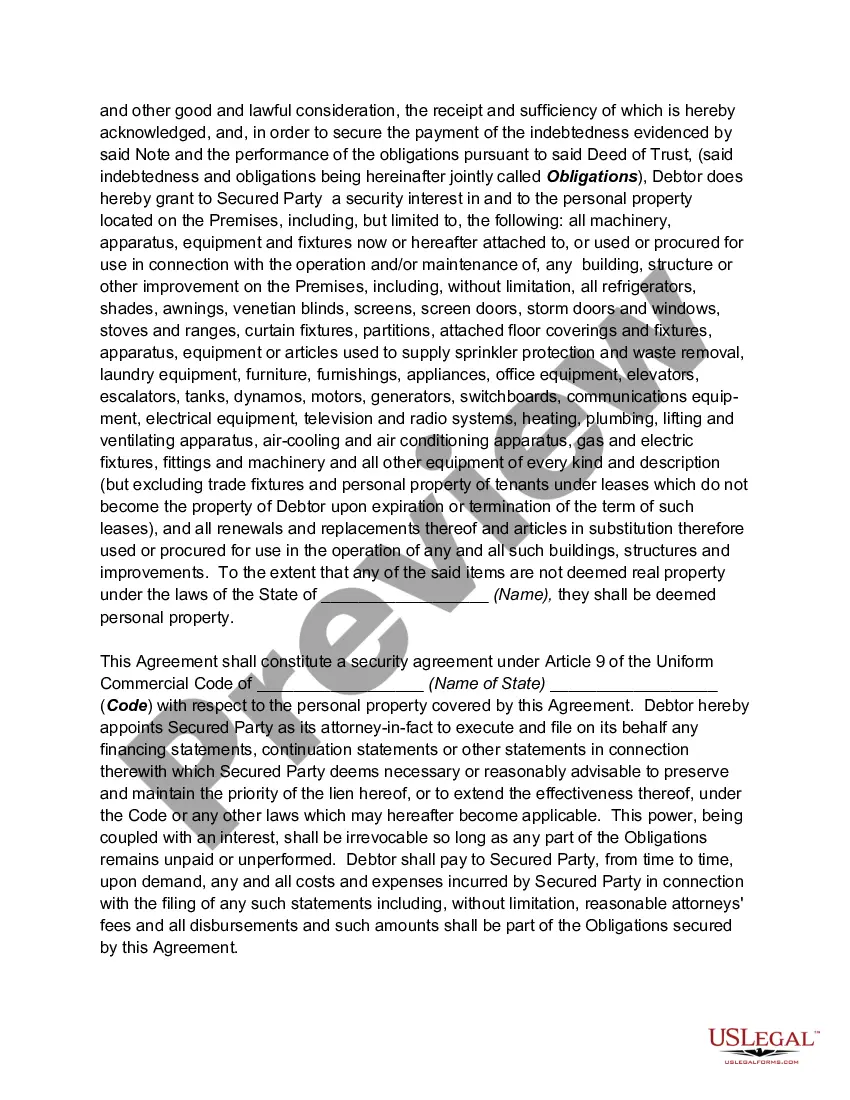

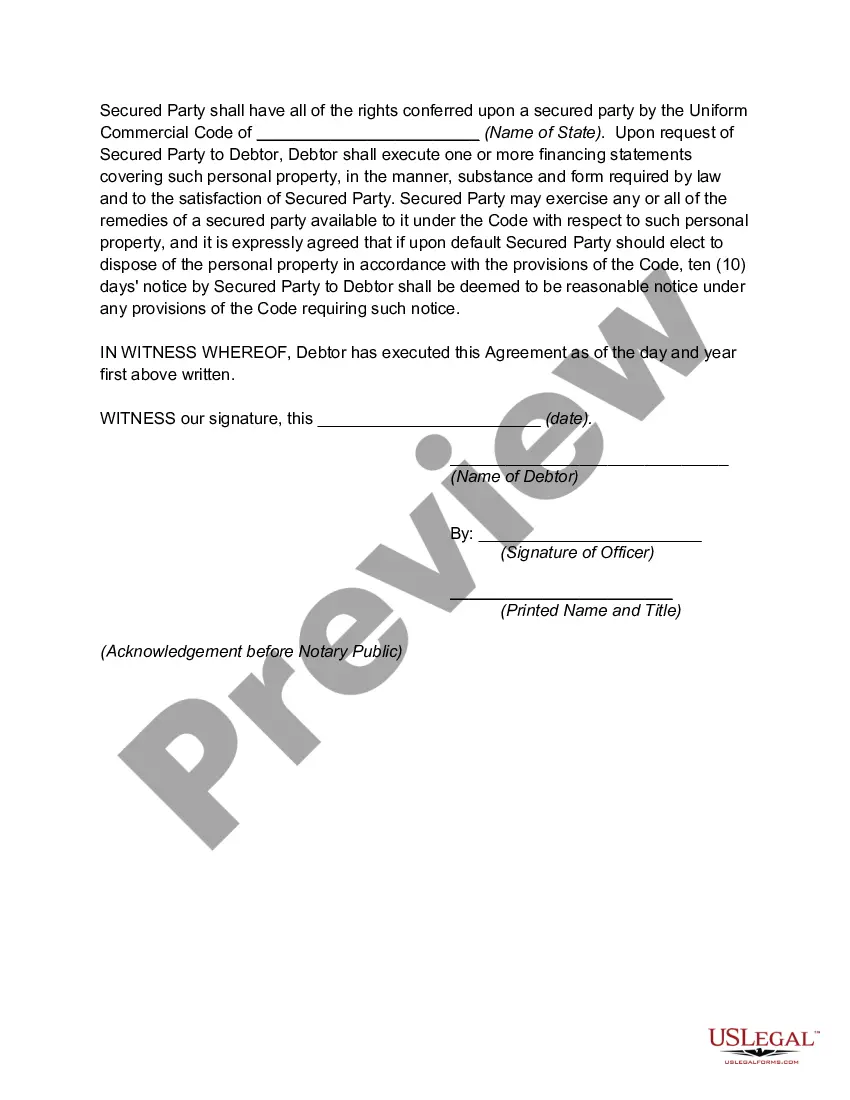

Fairfax Virginia Security Agreement in Personal Property Fixtures is an essential legal document that plays a crucial role in securing a commercial loan in the Fairfax, Virginia area. This agreement is a contract between a lender and a borrower, outlining the terms and conditions for using personal property fixtures as collateral. In this type of security agreement, personal property fixtures refer to items that are affixed or attached to an immovable property. These could include equipment, machinery, appliances, signage, or any other item that enhances the functionality of a commercial property. These fixtures can be vital assets for businesses seeking financing, as they provide additional security for lenders. The Fairfax Virginia Security Agreement in Personal Property Fixtures is designed to protect the lender's interests by establishing a lien on the property fixtures. This lien grants the lender the right to seize and sell the fixtures in the event of default or non-payment by the borrower. By including personal property fixtures in the collateral agreement, lenders can mitigate the risks associated with providing a commercial loan. This security agreement outlines various terms and conditions, such as: 1. Identification of the parties involved: The agreement clearly states the names and contact details of both the lender and the borrower. 2. Description of property fixtures: Each item being used as collateral is thoroughly described, including its make, model, serial number, and any other identifying information. 3. Grant of security interest: The borrower grants a security interest in the personal property fixtures to the lender, giving them the right to possess and sell the fixtures in case of default. 4. Perfection of the security interest: This section explains how the lender will perfect their security interest, often through the filing of a Uniform Commercial Code (UCC) financing statement with the appropriate government authority. 5. Representations and warranties: The borrower typically makes various representations and warranties regarding their ownership of the fixtures, their legal right to pledge them as collateral, and other relevant details. 6. Default and remedies: The agreement clearly defines events of default, such as non-payment, and outlines the remedies available to the lender, including repossession, sale, and any other legally permissible means to recover the outstanding amount. There may not be different types of Fairfax Virginia Security Agreement in Personal Property Fixtures regarding securing a commercial loan. However, the terms and conditions within the agreement can vary depending on the specific requirements of the lender and borrower. In conclusion, the Fairfax Virginia Security Agreement in Personal Property Fixtures provides a comprehensive framework for securing a commercial loan by using personal property fixtures as collateral. By carefully crafting the agreement with the help of legal professionals, lenders can establish a higher level of security, while borrowers can access the funds necessary to grow and expand their businesses.

Fairfax Virginia Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan

Description

How to fill out Fairfax Virginia Security Agreement In Personal Property Fixtures Regarding Securing A Commercial Loan?

A document routine always accompanies any legal activity you make. Creating a business, applying or accepting a job offer, transferring property, and lots of other life scenarios require you prepare formal documentation that differs throughout the country. That's why having it all collected in one place is so beneficial.

US Legal Forms is the largest online library of up-to-date federal and state-specific legal forms. On this platform, you can easily locate and download a document for any individual or business objective utilized in your county, including the Fairfax Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan.

Locating templates on the platform is extremely simple. If you already have a subscription to our service, log in to your account, find the sample through the search bar, and click Download to save it on your device. After that, the Fairfax Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan will be accessible for further use in the My Forms tab of your profile.

If you are using US Legal Forms for the first time, adhere to this simple guide to get the Fairfax Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan:

- Make sure you have opened the right page with your local form.

- Make use of the Preview mode (if available) and browse through the sample.

- Read the description (if any) to ensure the template satisfies your requirements.

- Look for another document using the search option if the sample doesn't fit you.

- Click Buy Now when you locate the necessary template.

- Decide on the appropriate subscription plan, then log in or register for an account.

- Select the preferred payment method (with credit card or PayPal) to continue.

- Opt for file format and save the Fairfax Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan on your device.

- Use it as needed: print it or fill it out electronically, sign it, and send where requested.

This is the easiest and most reliable way to obtain legal documents. All the templates provided by our library are professionally drafted and checked for correspondence to local laws and regulations. Prepare your paperwork and manage your legal affairs efficiently with the US Legal Forms!