Fairfax, Virginia Jury Instruction — 10.10.1 Reasonable Compensation to Stockholder-Employee In Fairfax, Virginia, the jury instruction 10.10.1 provides guidance for determining reasonable compensation to a stockholder who is also an employee of a company. This instruction aids juries in understanding the principles and factors that may be considered when evaluating the reasonableness of compensation given to stockholder-employees. Reasonable compensation is an important aspect in corporate governance and tax compliance, as it ensures fairness in the distribution of corporate income and prevents abusive practices such as excessive compensation to avoid taxes. Understanding and applying this jury instruction is crucial to make informed decisions regarding compensating stockholders who are also employees within the jurisdiction of Fairfax, Virginia. The jury instruction 10.10.1 highlights several key factors to consider when evaluating the reasonableness of compensation to stockholder-employees: 1. Industry standards and norms: Juries should take into account the typical compensation practices observed within the industry in which the company operates. This involves considering the compensation levels for similar positions within comparable companies. 2. Job duties and responsibilities: Juries must assess the stockholder-employee's specific roles, responsibilities, and contributions to the company. Compensation should align with the scope and complexity of these duties. 3. Qualifications and experience: The jury needs to consider the stockholder-employee's qualifications, experience, and expertise when evaluating compensation. Higher levels of education, professional certifications, or industry-related achievements may justify higher compensation. 4. Financial condition of the company: The financial health and performance of the company should play a role in determining reasonable compensation. Juries should consider the company's profitability, revenues, and ability to sustain compensation levels. 5. Comparison to non-stockholder employees: Juries should compare the compensation of stockholder-employees to that of non-stockholder employees in similar roles. If there are significant disparities, it may indicate a need for further scrutiny. Different types of Fairfax, Virginia Jury Instruction — 10.10.1 Reasonable Compensation to Stockholder-Employee: 1. Standard Reasonable Compensation Instruction: This instruction serves as a general guideline for determining reasonable compensation to stockholder-employees. 2. Specific Industry Instruction: The court may provide modified versions of the instruction tailored to specific industries to account for unique compensation practices and norms within that industry. 3. Tax Compliance Instruction: This instruction may focus on the implications of reasonable compensation for tax compliance and preventing abusive practices related to excessive compensation. In conclusion, Fairfax, Virginia Jury Instruction — 10.10.1 Reasonable Compensation to Stockholder-Employee provides a framework for evaluating and determining reasonable compensation for stockholder-employees, considering factors such as industry standards, job responsibilities, qualifications, financial condition of the company, and comparisons to non-stockholder employees. This instruction ensures fairness and compliance within corporate governance and tax regulations.

Fairfax Virginia Jury Instruction - 10.10.1 Reasonable Compensation To Stockholder - Employee

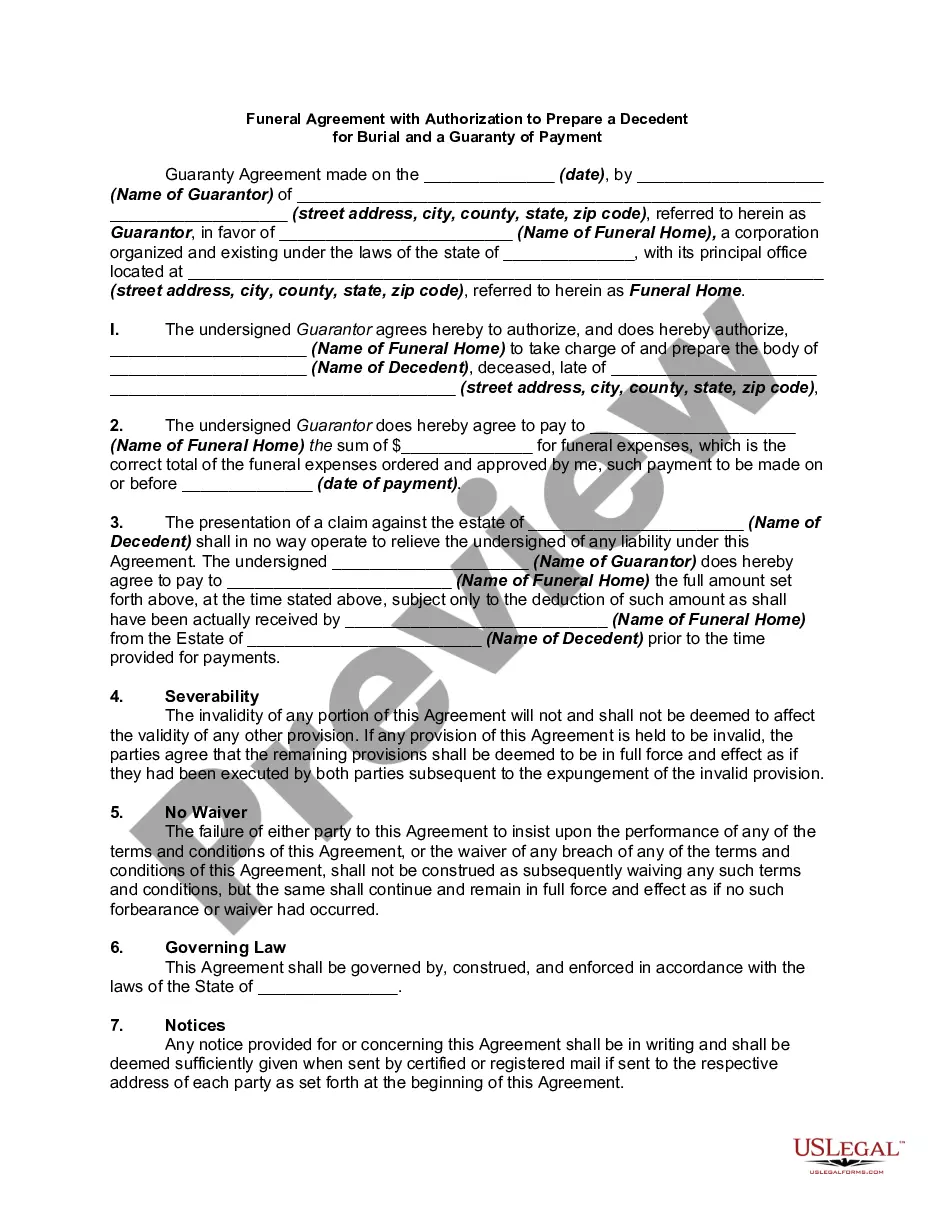

Description

How to fill out Fairfax Virginia Jury Instruction - 10.10.1 Reasonable Compensation To Stockholder - Employee?

Are you looking to quickly create a legally-binding Fairfax Jury Instruction - 10.10.1 Reasonable Compensation To Stockholder - Employee or probably any other document to take control of your personal or corporate affairs? You can select one of the two options: contact a professional to write a legal paper for you or create it completely on your own. Thankfully, there's an alternative option - US Legal Forms. It will help you receive neatly written legal papers without paying unreasonable fees for legal services.

US Legal Forms offers a huge catalog of over 85,000 state-specific document templates, including Fairfax Jury Instruction - 10.10.1 Reasonable Compensation To Stockholder - Employee and form packages. We provide documents for an array of life circumstances: from divorce papers to real estate document templates. We've been on the market for more than 25 years and got a spotless reputation among our customers. Here's how you can become one of them and get the necessary document without extra hassles.

- First and foremost, carefully verify if the Fairfax Jury Instruction - 10.10.1 Reasonable Compensation To Stockholder - Employee is adapted to your state's or county's regulations.

- In case the document comes with a desciption, make sure to check what it's intended for.

- Start the search again if the form isn’t what you were looking for by using the search box in the header.

- Choose the subscription that is best suited for your needs and proceed to the payment.

- Select the file format you would like to get your document in and download it.

- Print it out, complete it, and sign on the dotted line.

If you've already set up an account, you can simply log in to it, find the Fairfax Jury Instruction - 10.10.1 Reasonable Compensation To Stockholder - Employee template, and download it. To re-download the form, simply head to the My Forms tab.

It's stressless to buy and download legal forms if you use our services. Additionally, the templates we provide are reviewed by law professionals, which gives you greater peace of mind when dealing with legal affairs. Try US Legal Forms now and see for yourself!