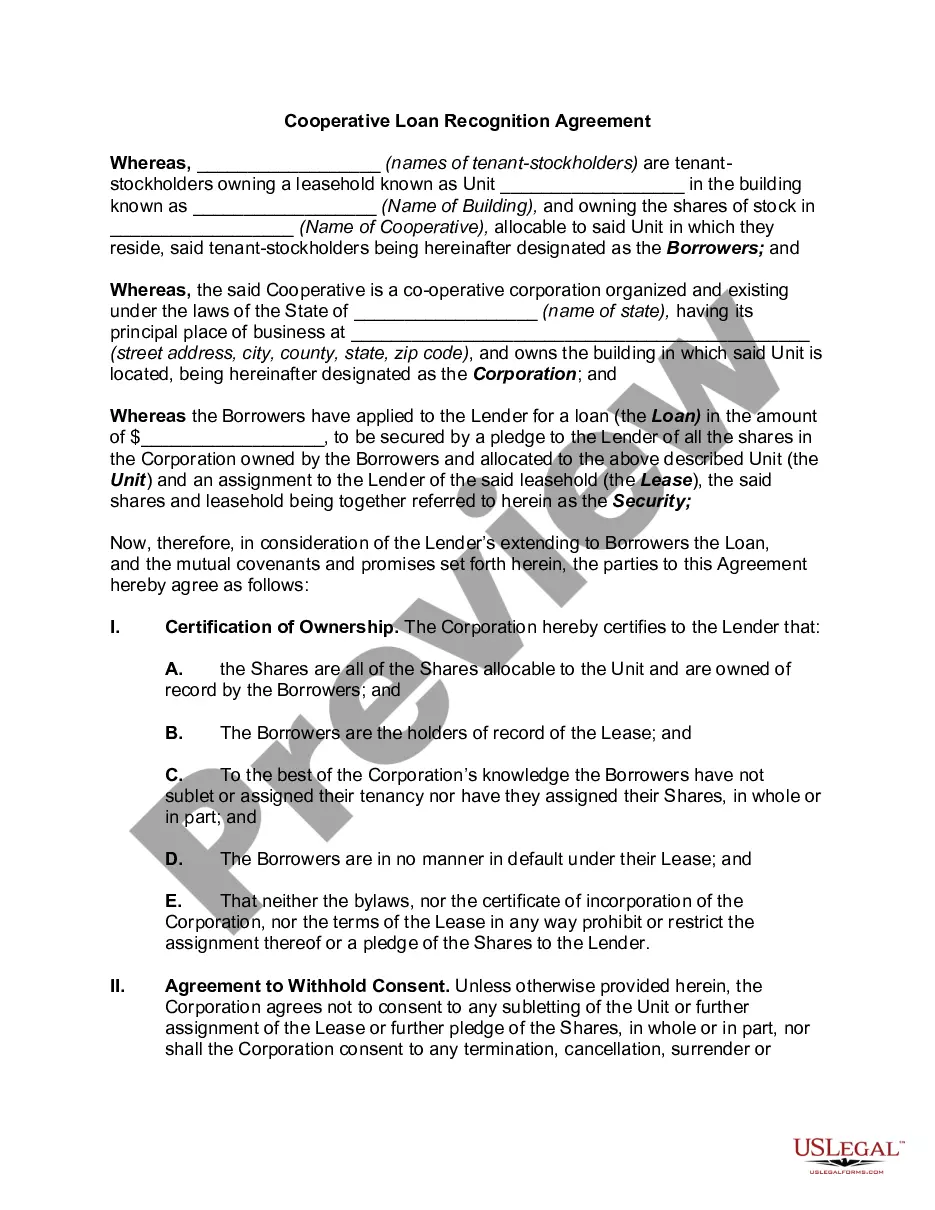

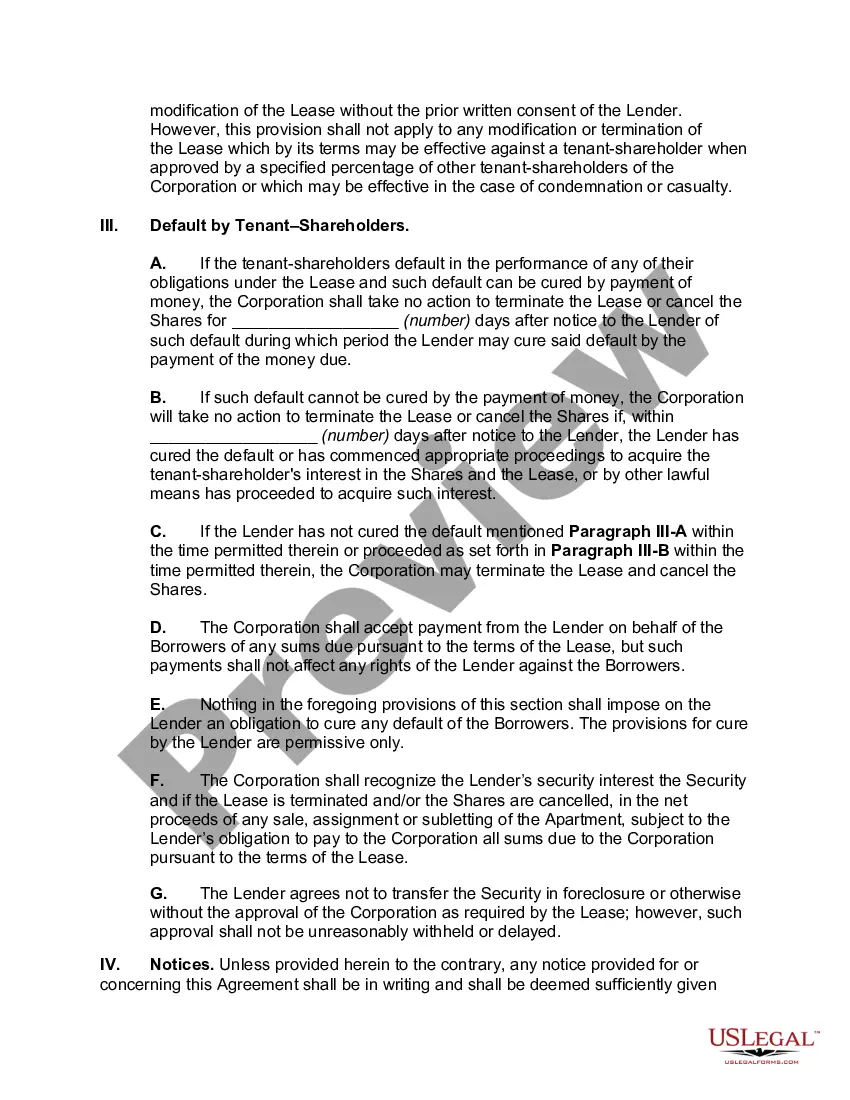

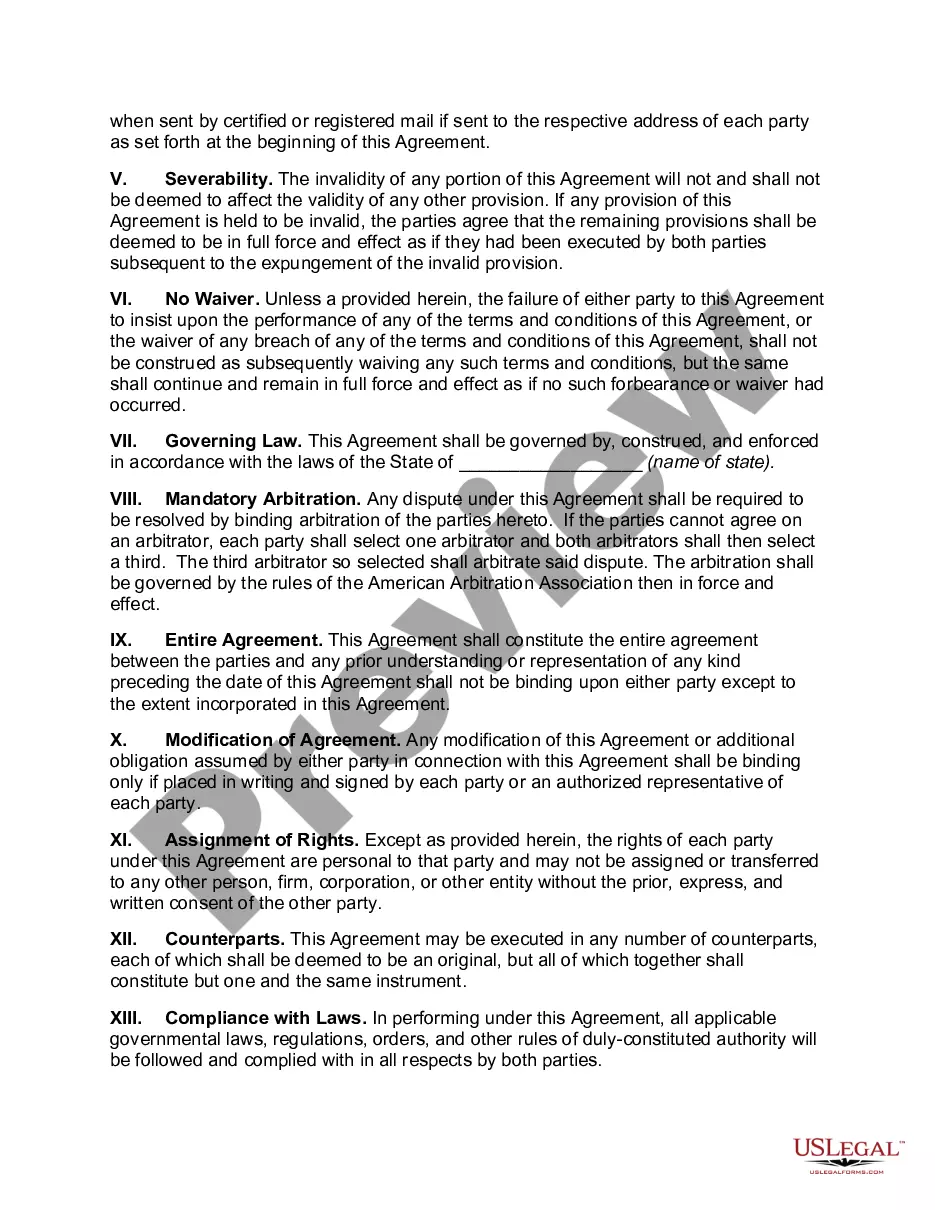

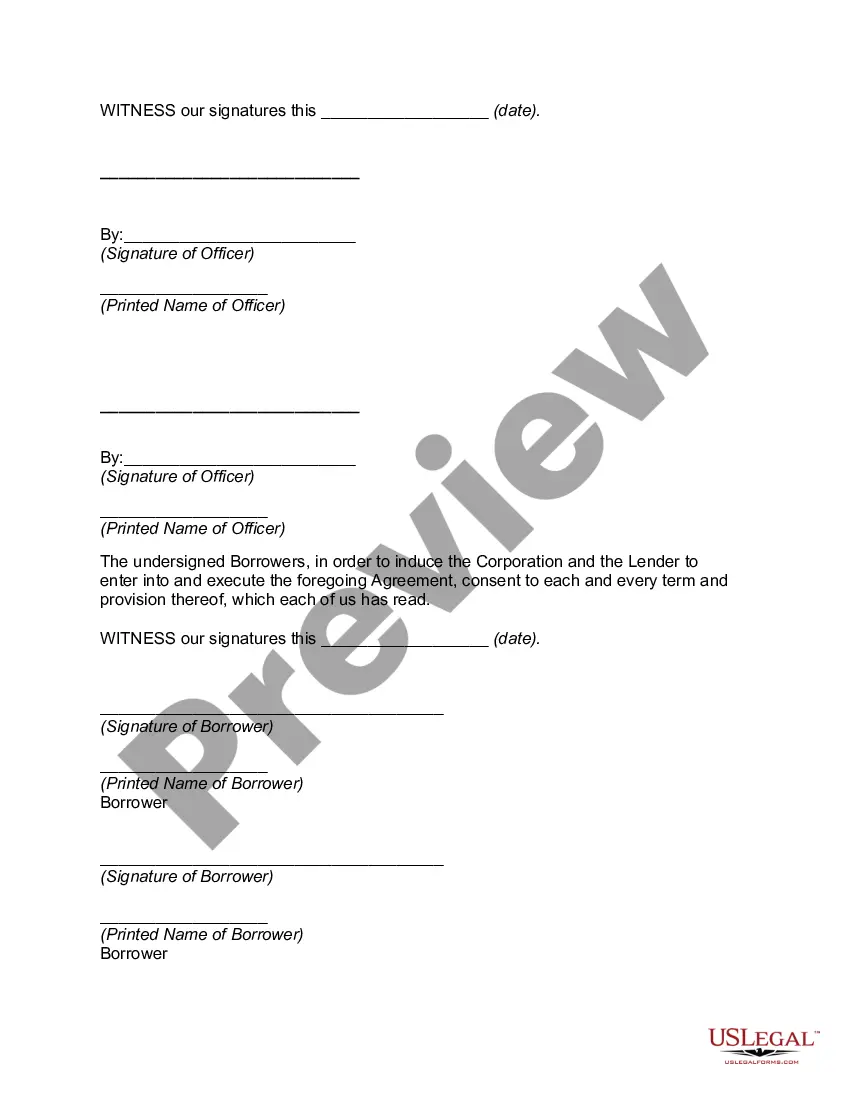

Contra Costa California Cooperative Loan Recognition Agreement is a legal contract commonly used in cooperative financing transactions within Contra Costa County, California. It outlines the terms and conditions under which a loan is granted and acknowledged by a cooperative and its members. This agreement serves as a vital document ensuring clarity and protection for both lenders and borrowers involved in cooperative financing arrangements. The Contra Costa California Cooperative Loan Recognition Agreement establishes the cooperative's obligation to recognize and honor a loan made to the cooperative as agreed upon. It specifies the loan amount, interest rate, repayment terms, and any other relevant provisions necessary for the loan transaction. By signing this agreement, the cooperative commits to repaying the loan in accordance with the agreed-upon terms, including timely payment of installments and adherence to any collateral requirements. To ensure complete understanding and consideration of various cooperative loan scenarios, there might be specific types or variations of the Contra Costa California Cooperative Loan Recognition Agreement. These variations could include: 1. Standard Cooperative Loan Recognition Agreement: This type outlines the fundamental terms and conditions applicable to most cooperative financing transactions within Contra Costa County. It covers aspects such as interest rates, repayment schedules, default consequences, and collateral requirements. 2. Multi-phase Cooperative Loan Recognition Agreement: This variation caters specifically to cooperative projects that involve multiple phases or stages of development. It provides provisions for progressive financing, disbursement criteria, and documents each phase's loan recognition obligations separately. 3. Refinancing Cooperative Loan Recognition Agreement: This type focuses on recognizing and acknowledging loans that specifically replace or refinance existing cooperative debts. It outlines the process and terms of refinancing, including the settlement of previous loans and any necessary modifications to the existing repayment structure. 4. Cooperative Loan Modification Agreement: In cases where cooperative financing terms need to be modified due to changing circumstances, this type of agreement allows for alterations in interest rates, repayment schedules, or other specific terms. It requires mutual consent from both the lender and the cooperative, ensuring transparency and clarity regarding the modified loan recognition. In summary, the Contra Costa California Cooperative Loan Recognition Agreement is a crucial legal document that specifies the terms and obligations surrounding cooperative loans within Contra Costa County. These agreements ensure that all parties involved are aware of their responsibilities, protecting the interests of lenders and borrowers alike.

Contra Costa California Cooperative Loan Recognition Agreement

Description

How to fill out Contra Costa California Cooperative Loan Recognition Agreement?

Laws and regulations in every sphere vary around the country. If you're not a lawyer, it's easy to get lost in countless norms when it comes to drafting legal documentation. To avoid high priced legal assistance when preparing the Contra Costa Cooperative Loan Recognition Agreement, you need a verified template legitimate for your region. That's when using the US Legal Forms platform is so helpful.

US Legal Forms is a trusted by millions web catalog of more than 85,000 state-specific legal forms. It's a great solution for professionals and individuals searching for do-it-yourself templates for various life and business scenarios. All the forms can be used many times: once you obtain a sample, it remains accessible in your profile for further use. Thus, if you have an account with a valid subscription, you can simply log in and re-download the Contra Costa Cooperative Loan Recognition Agreement from the My Forms tab.

For new users, it's necessary to make a few more steps to obtain the Contra Costa Cooperative Loan Recognition Agreement:

- Examine the page content to make sure you found the right sample.

- Use the Preview option or read the form description if available.

- Look for another doc if there are inconsistencies with any of your criteria.

- Use the Buy Now button to get the document once you find the right one.

- Opt for one of the subscription plans and log in or create an account.

- Choose how you prefer to pay for your subscription (with a credit card or PayPal).

- Select the format you want to save the document in and click Download.

- Complete and sign the document on paper after printing it or do it all electronically.

That's the easiest and most affordable way to get up-to-date templates for any legal scenarios. Find them all in clicks and keep your paperwork in order with the US Legal Forms!