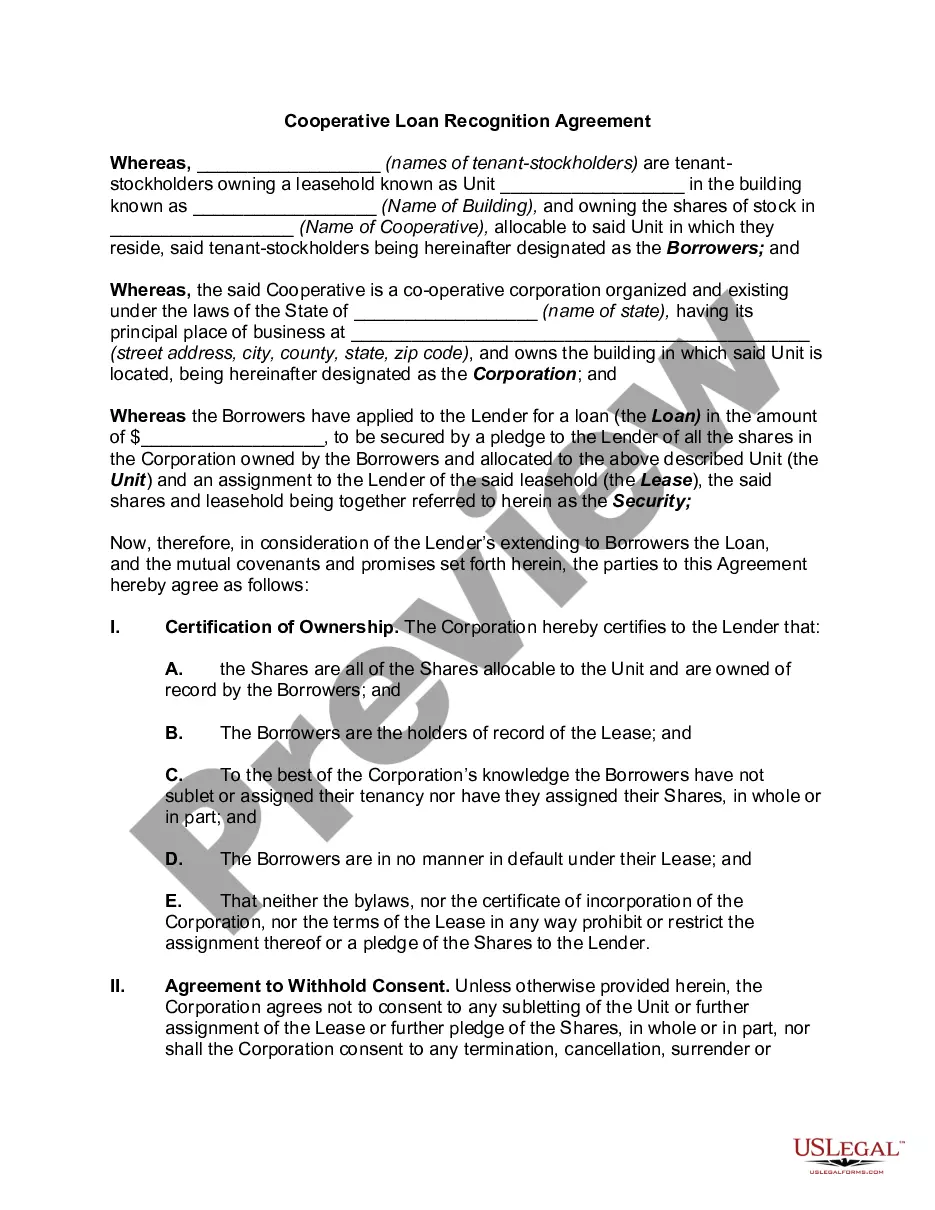

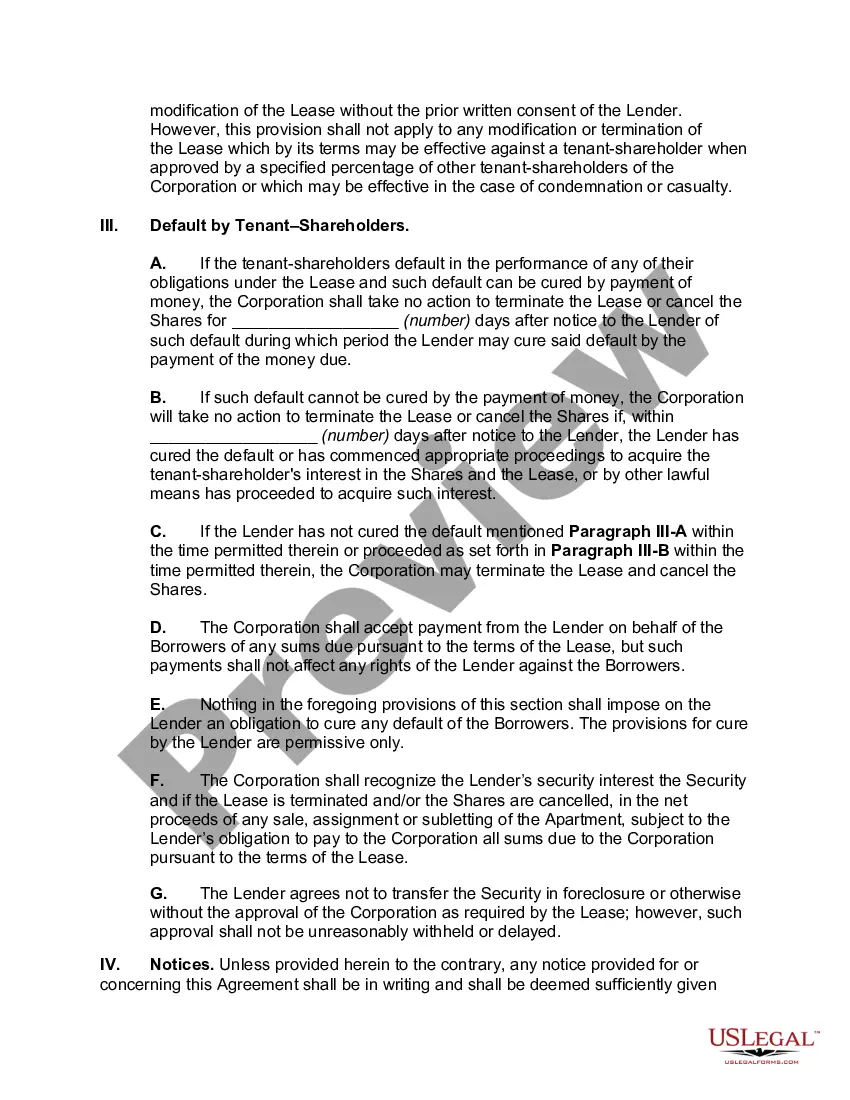

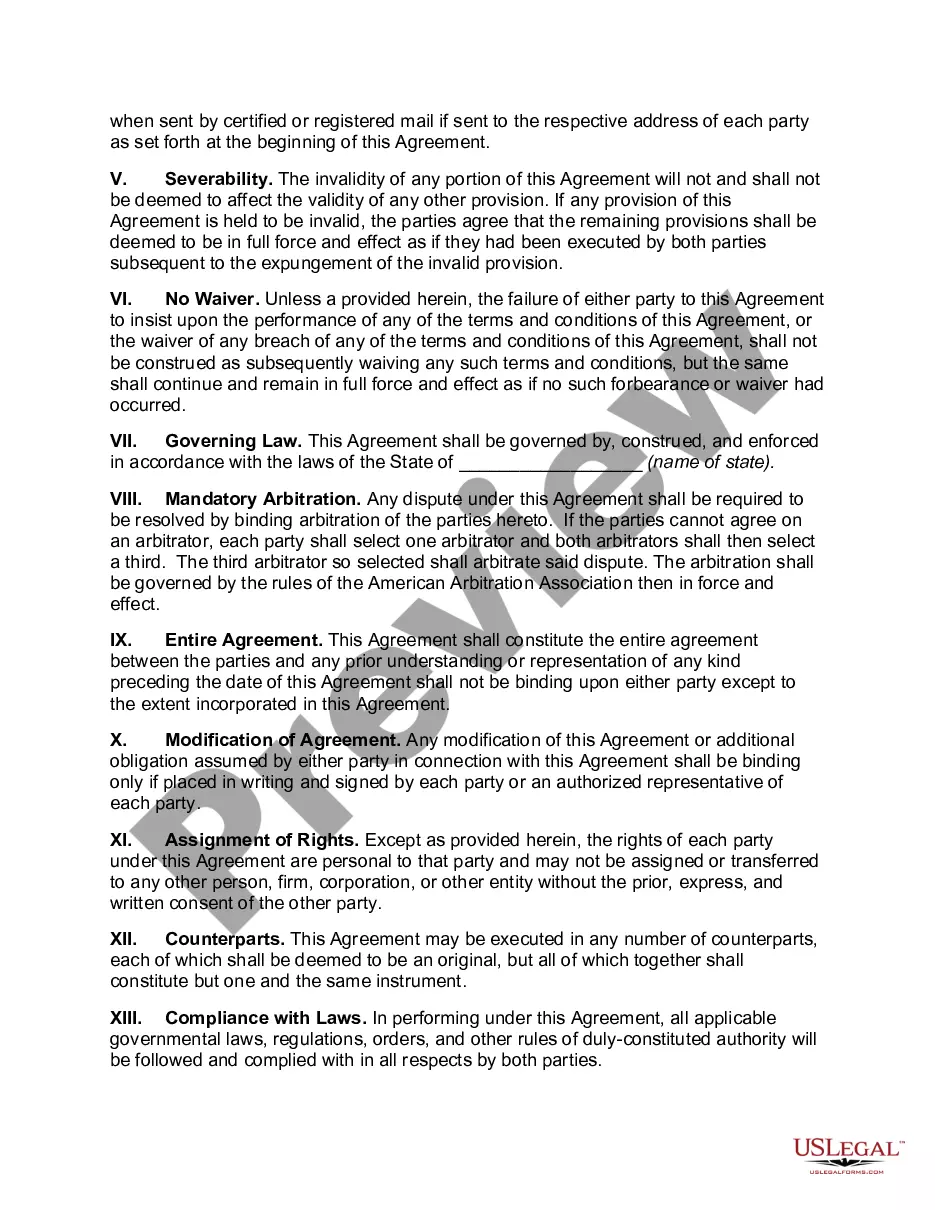

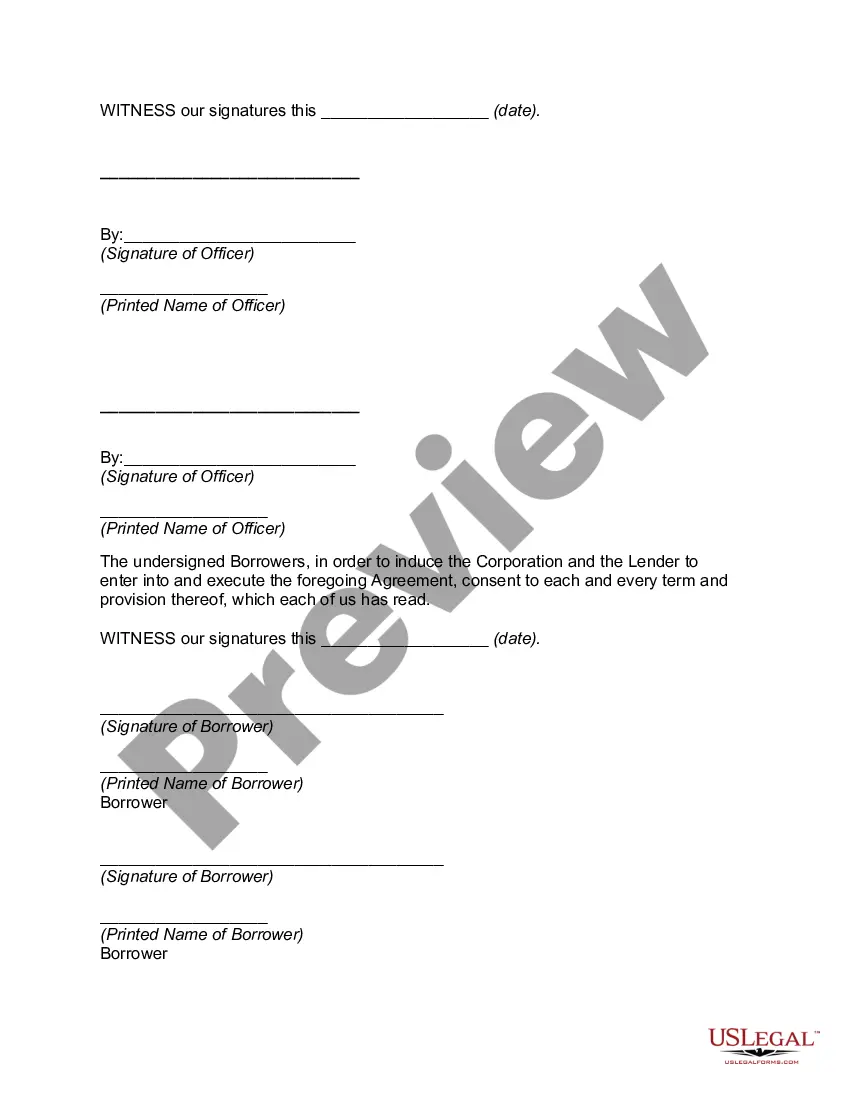

The Cook Illinois Cooperative Loan Recognition Agreement is a legal document that outlines the terms and conditions between the Cook Illinois Cooperative and the borrower in the context of a loan. This agreement serves as proof of the loan, demonstrating that the borrower has agreed to repay the amount borrowed along with applicable interest and fees. The Cook Illinois Cooperative Loan Recognition Agreement lays out the responsibilities and obligations of both parties involved. It includes important details such as the loan amount, interest rate, repayment schedule, and any additional fees or charges that may be applicable. This agreement ensures that both the cooperative and the borrower are aware of their rights and duties throughout the loan term. Different types of Cook Illinois Cooperative Loan Recognition Agreements may exist, depending on the specific purpose or circumstances of the loan. Some common variations include: 1. Personal Loan Recognition Agreement: This type of agreement is typically used when an individual borrower seeks financial assistance from the Cook Illinois Cooperative for personal reasons, such as funding for education, medical expenses, or home improvements. 2. Business Loan Recognition Agreement: In the case of a business seeking financial support from the Cook Illinois Cooperative, a separate type of agreement may be used. This agreement outlines the terms and conditions specific to the business, addressing factors like cash flow projections, potential collateral, and expected return on investment. 3. Agricultural Loan Recognition Agreement: For borrowers involved in agricultural activities, such as farming or livestock production, the Cook Illinois Cooperative may offer specialized loan recognition agreements. These agreements address the unique nature of agricultural operations, including factors like seasonal income, insurance requirements, and the use of farm assets as collateral. 4. Microfinance Loan Recognition Agreement: Cook Illinois Cooperative may also provide access to microfinance loans, which are small loans aimed at supporting individuals or small businesses with limited resources. This type of agreement typically includes flexible terms and lower interest rates to encourage entrepreneurship and economic development. It is essential for both parties involved in a Cook Illinois Cooperative Loan Recognition Agreement to thoroughly review and understand the terms and conditions outlined in the agreement before signing it. Seeking legal advice or assistance, if necessary, can help ensure that the agreement accurately reflects the expectations and obligations of all parties involved.

Cook Illinois Cooperative Loan Recognition Agreement

Description

How to fill out Cook Illinois Cooperative Loan Recognition Agreement?

Creating documents, like Cook Cooperative Loan Recognition Agreement, to manage your legal affairs is a tough and time-consumming process. Many situations require an attorney’s participation, which also makes this task expensive. However, you can get your legal affairs into your own hands and manage them yourself. US Legal Forms is here to the rescue. Our website comes with over 85,000 legal documents created for various cases and life situations. We make sure each document is in adherence with the laws of each state, so you don’t have to be concerned about potential legal issues associated with compliance.

If you're already familiar with our website and have a subscription with US, you know how straightforward it is to get the Cook Cooperative Loan Recognition Agreement form. Simply log in to your account, download the template, and customize it to your needs. Have you lost your document? Don’t worry. You can get it in the My Forms folder in your account - on desktop or mobile.

The onboarding process of new customers is just as easy! Here’s what you need to do before getting Cook Cooperative Loan Recognition Agreement:

- Ensure that your template is compliant with your state/county since the regulations for creating legal documents may differ from one state another.

- Discover more information about the form by previewing it or going through a brief description. If the Cook Cooperative Loan Recognition Agreement isn’t something you were hoping to find, then take advantage of the search bar in the header to find another one.

- Sign in or create an account to begin utilizing our website and get the document.

- Everything looks great on your end? Click the Buy now button and choose the subscription option.

- Select the payment gateway and enter your payment details.

- Your template is ready to go. You can try and download it.

It’s an easy task to locate and buy the appropriate template with US Legal Forms. Thousands of organizations and individuals are already benefiting from our rich library. Subscribe to it now if you want to check what other perks you can get with US Legal Forms!