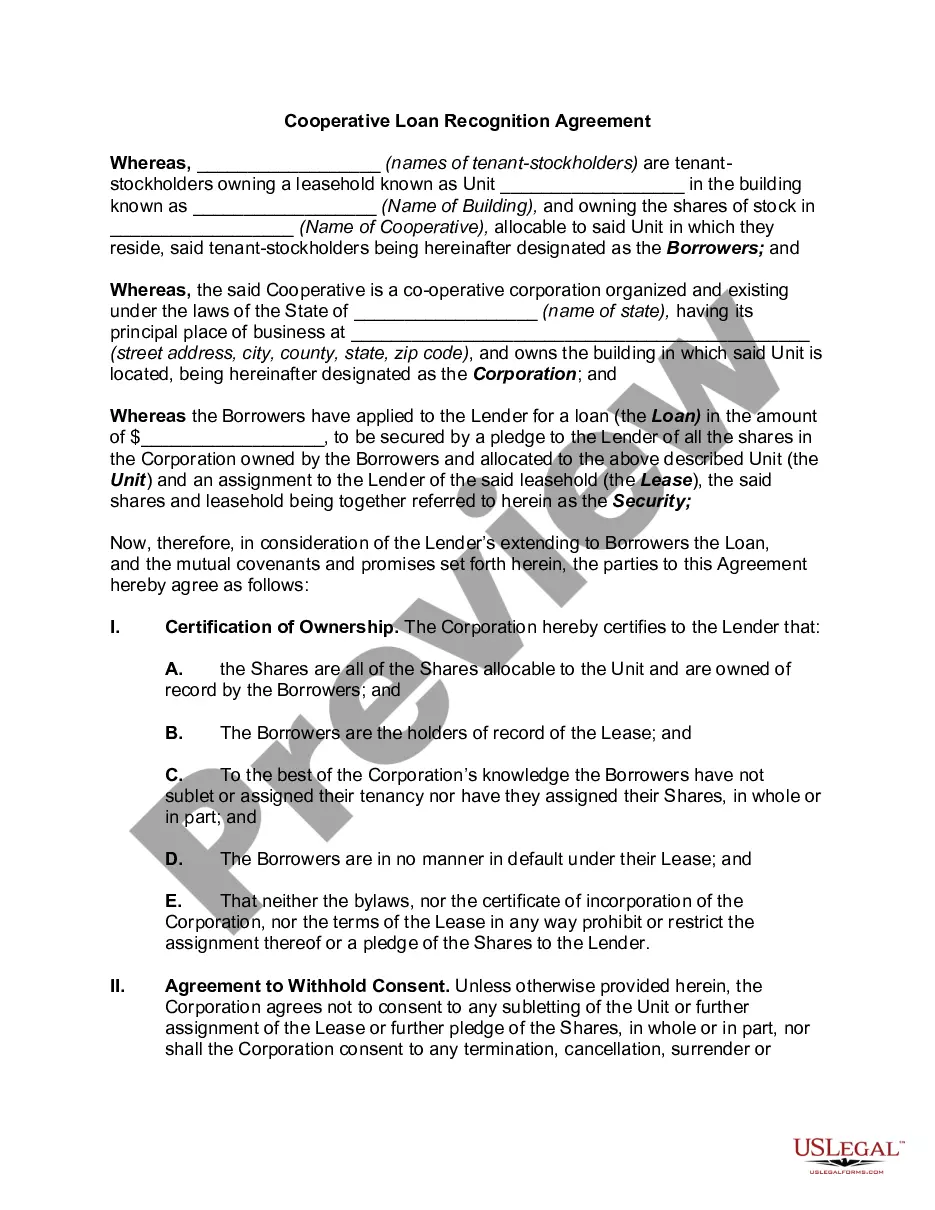

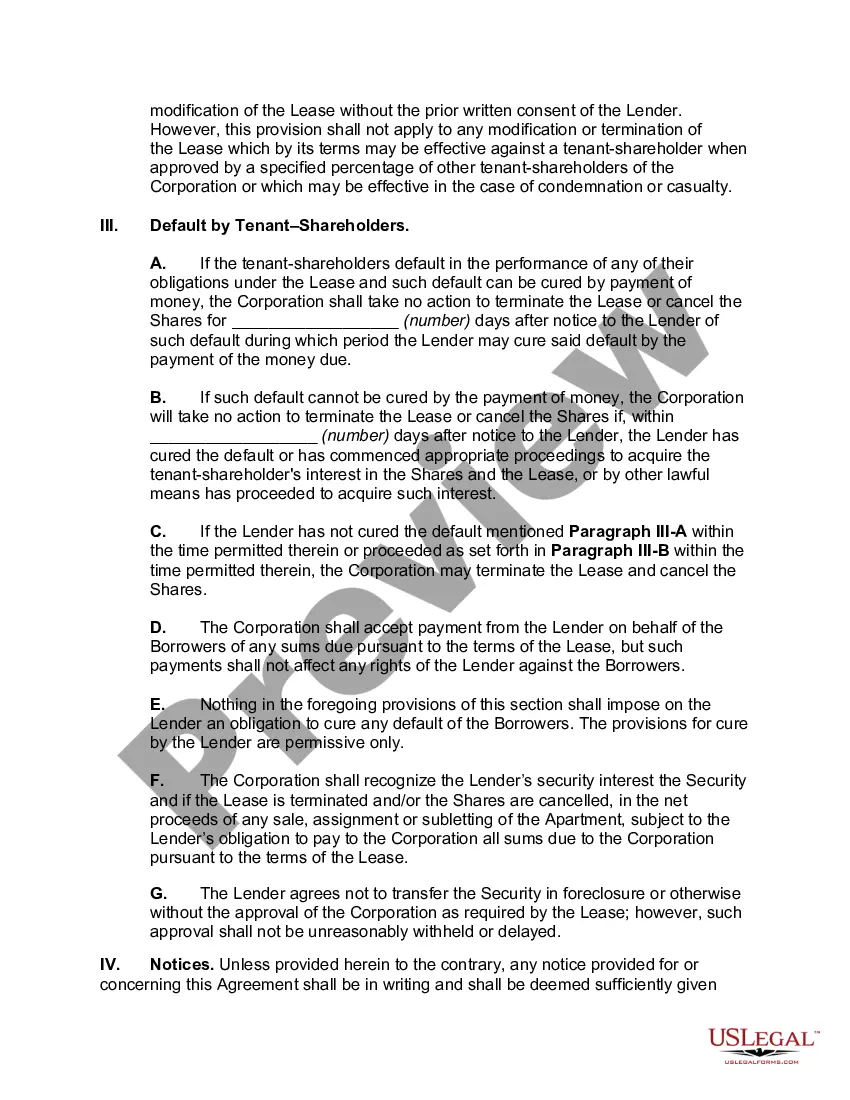

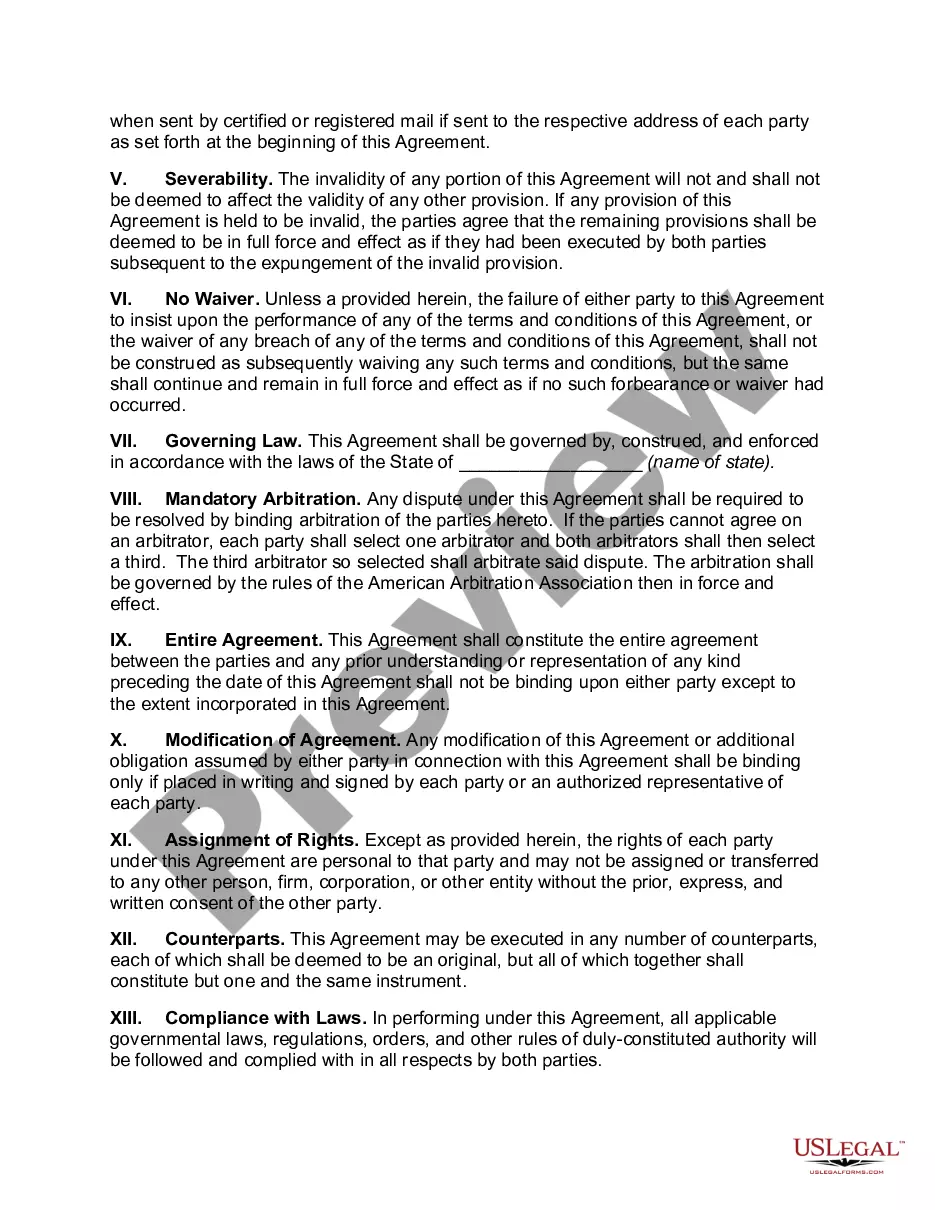

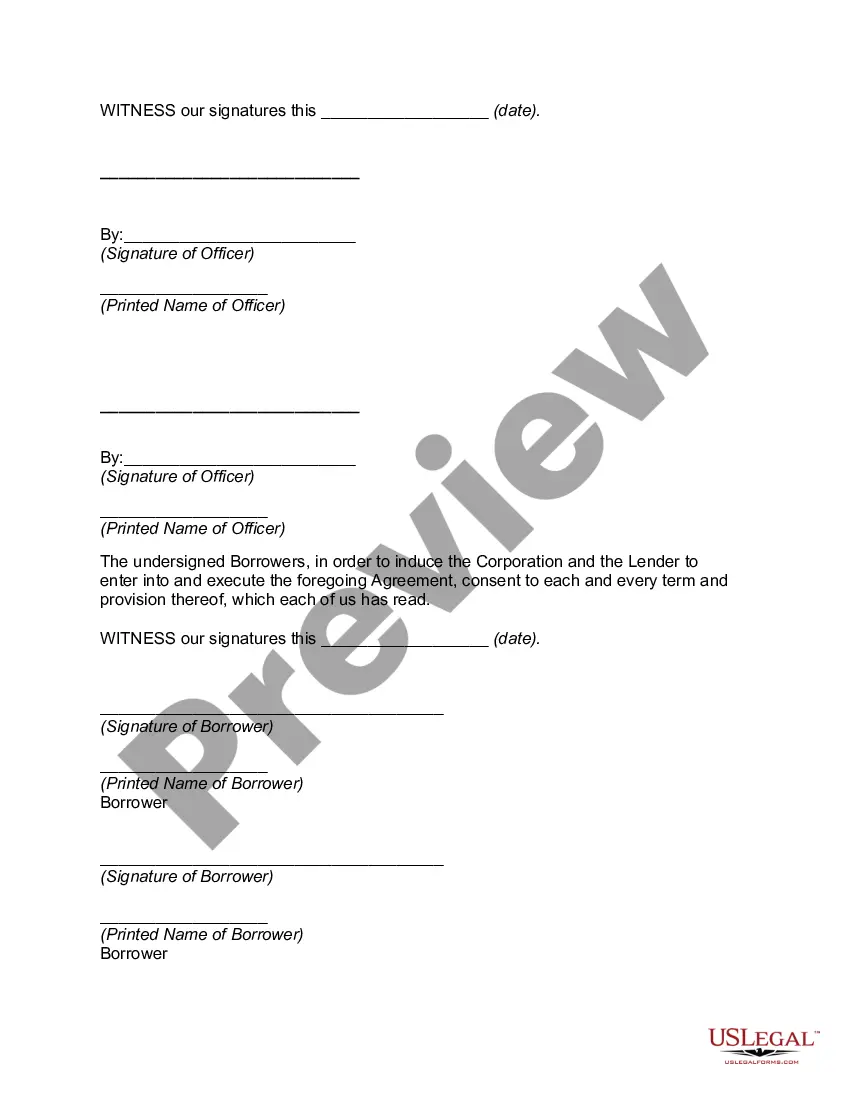

Nassau New York Cooperative Loan Recognition Agreement is a legal document that establishes the terms and conditions between a cooperative and a lender when obtaining a loan for the purchase or development of a property in Nassau, New York. This agreement, also known as a Loan Recognition Agreement or Cooperative Financing Agreement, outlines the responsibilities, obligations, and rights of both parties involved in the loan process. The Nassau New York Cooperative Loan Recognition Agreement addresses various key aspects related to the loan, such as the loan amount, interest rate, repayment schedule, collateral, and the cooperative's responsibilities to provide necessary documentation and access to information to the lender. This agreement ensures that the cooperative and the lender have a clear understanding of their roles and responsibilities, safeguarding the interests of both parties. Different types of Nassau New York Cooperative Loan Recognition Agreement may exist based on specific circumstances or requirements. Some of these variations include: 1. Purchase Loan Recognition Agreement: This type of agreement is used when a cooperative seeks financing for the acquisition of a property in Nassau, New York. It sets out the terms and conditions related to the loan amount, down payment, interest rate, and repayment schedule. 2. Development Loan Recognition Agreement: When a cooperative intends to undertake a development project, such as renovating or expanding existing properties or constructing new units, this agreement is used. It outlines the terms and conditions specific to the development loan, addressing aspects like loan disbursement stages, completion deadlines, and requirements for inspections or progress reports. 3. Refinancing Loan Recognition Agreement: In cases where a cooperative wishes to replace an existing loan with a new loan having better terms or interest rates, a refinancing loan recognition agreement is used. This agreement outlines the terms of the new loan, including the loan amount, interest rate, repayment schedule, and any associated fees or costs. 4. Secured Loan Recognition Agreement: When a cooperative offers collateral, such as the property itself or other assets, to secure the loan, this agreement is used. It establishes the terms related to the collateral, including appraisal processes, release conditions, and provisions for default or foreclosure. Overall, the Nassau New York Cooperative Loan Recognition Agreement is a crucial legal document in the cooperative lending process. It ensures clarity, transparency, and accountability between the cooperative and the lender, helping to facilitate a smooth loan transaction for the development or acquisition of properties in Nassau, New York.

Nassau New York Cooperative Loan Recognition Agreement

Description

How to fill out Nassau New York Cooperative Loan Recognition Agreement?

Laws and regulations in every sphere vary throughout the country. If you're not a lawyer, it's easy to get lost in various norms when it comes to drafting legal documents. To avoid costly legal assistance when preparing the Nassau Cooperative Loan Recognition Agreement, you need a verified template legitimate for your region. That's when using the US Legal Forms platform is so helpful.

US Legal Forms is a trusted by millions web library of more than 85,000 state-specific legal forms. It's an excellent solution for professionals and individuals looking for do-it-yourself templates for various life and business situations. All the documents can be used multiple times: once you purchase a sample, it remains available in your profile for future use. Thus, when you have an account with a valid subscription, you can just log in and re-download the Nassau Cooperative Loan Recognition Agreement from the My Forms tab.

For new users, it's necessary to make several more steps to get the Nassau Cooperative Loan Recognition Agreement:

- Take a look at the page content to make sure you found the appropriate sample.

- Take advantage of the Preview option or read the form description if available.

- Search for another doc if there are inconsistencies with any of your criteria.

- Use the Buy Now button to get the template once you find the correct one.

- Choose one of the subscription plans and log in or sign up for an account.

- Choose how you prefer to pay for your subscription (with a credit card or PayPal).

- Pick the format you want to save the document in and click Download.

- Fill out and sign the template in writing after printing it or do it all electronically.

That's the simplest and most cost-effective way to get up-to-date templates for any legal purposes. Find them all in clicks and keep your documentation in order with the US Legal Forms!