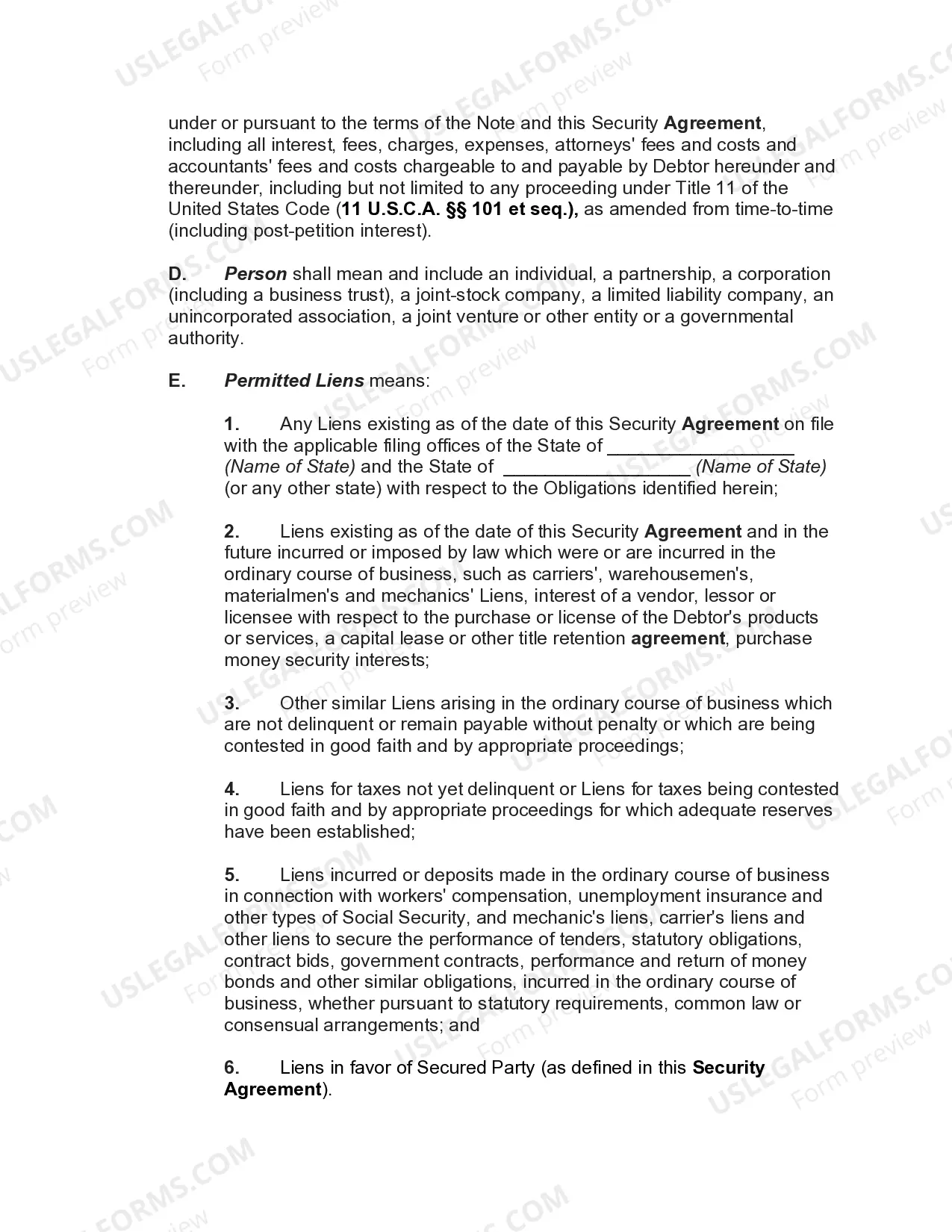

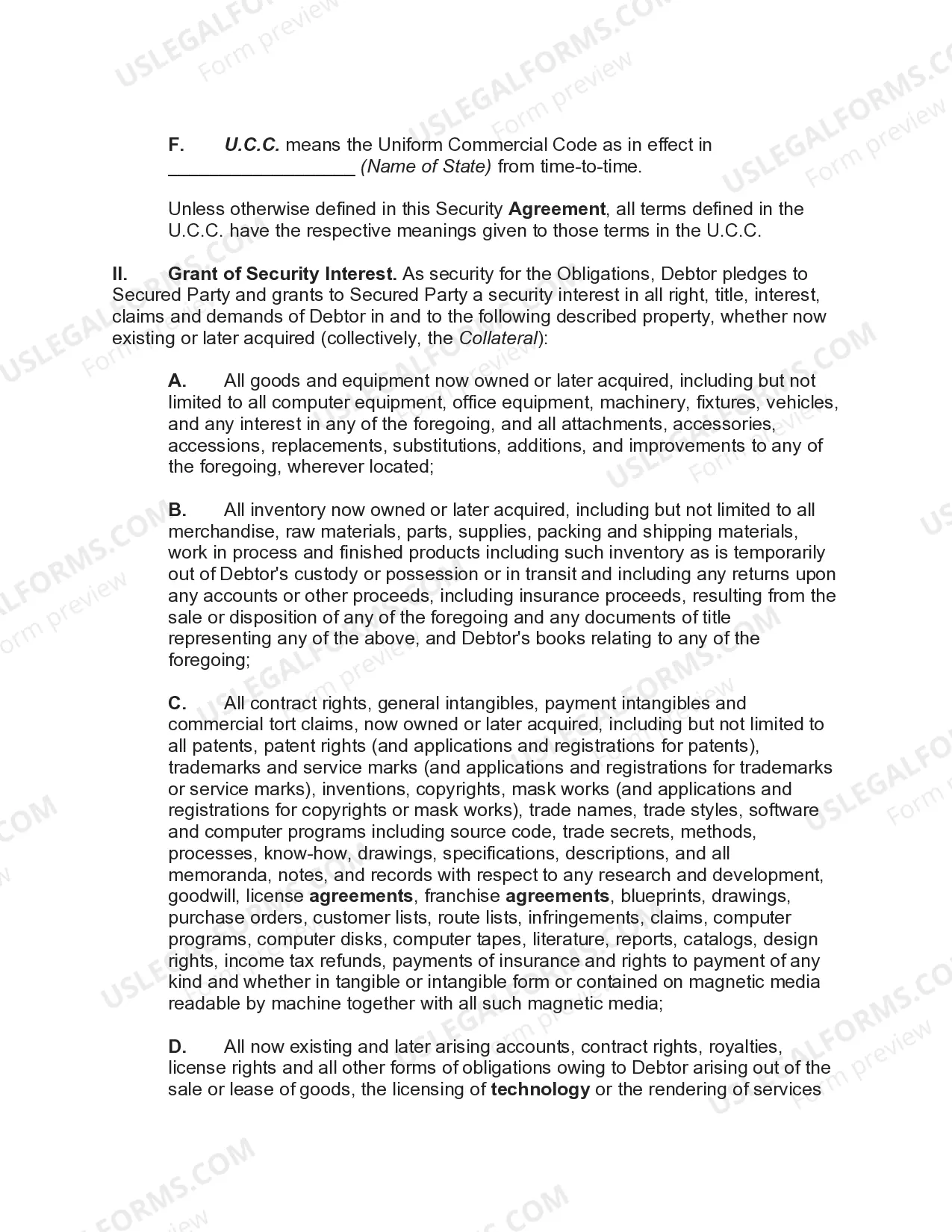

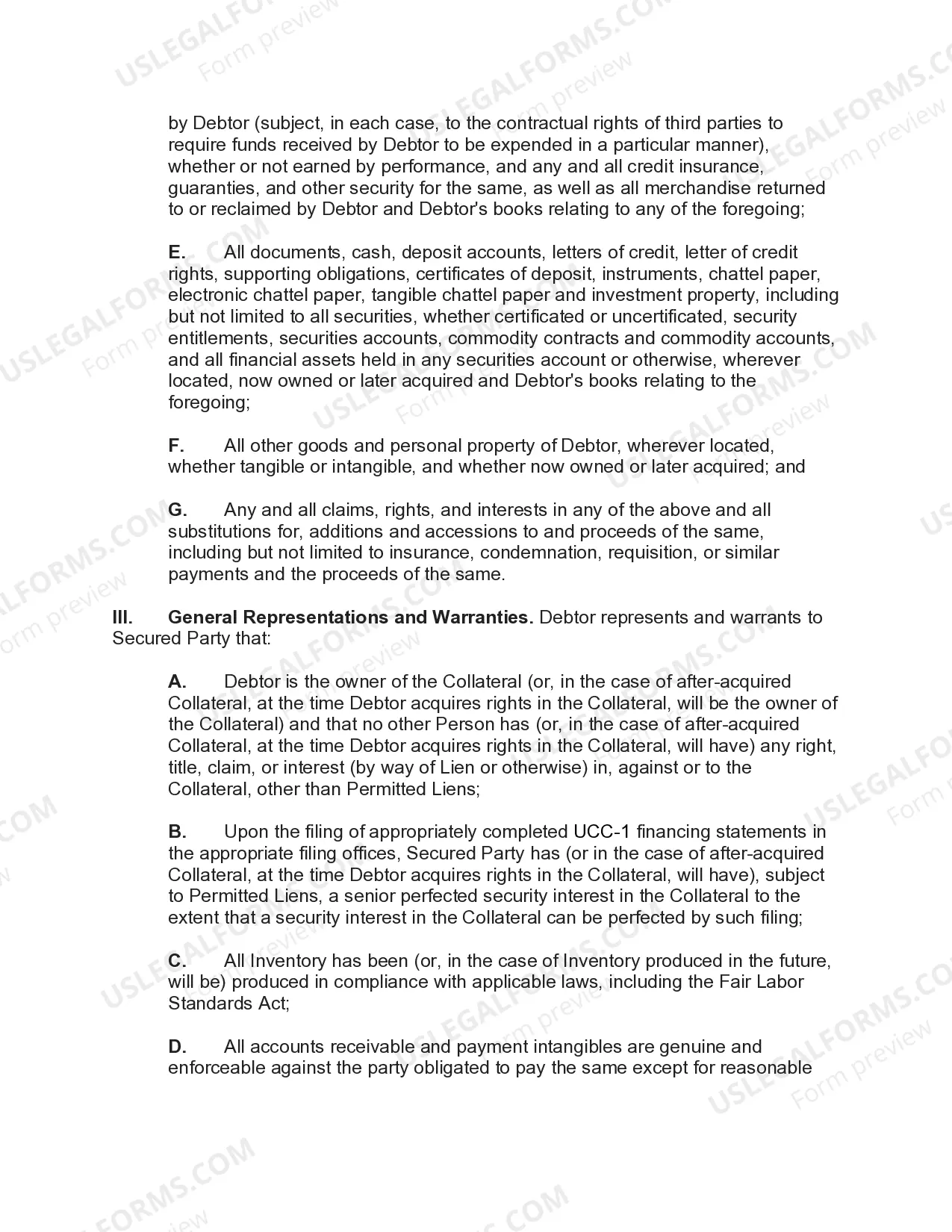

A Fairfax Virginia Security Agreement Covering Goods, Equipment, Inventory, Etc., also known as a security agreement or collateral agreement, is a legal contract between a lender and a borrower. This agreement ensures that the lender has a legal interest in certain assets or property owned by the borrower, serving as collateral for a loan or debt. By creating a security interest, the lender obtains the right to repossess and sell the collateral to recover the outstanding debt if the borrower defaults on their loan payments. In Fairfax Virginia, there are different types of security agreements covering various types of assets, including goods, equipment, and inventory. These agreements provide protection to lenders in the case of default, ensuring they can recoup their investment. Here's a breakdown of the different types: 1. Fairfax Virginia Security Agreement Covering Goods: This type of security agreement covers movable assets such as inventory, vehicles, machinery, or other personal property that has value or can be sold to repay the loan. It establishes the lender's right to take possession of these goods if the borrower fails to meet their repayment obligations. 2. Fairfax Virginia Security Agreement Covering Equipment: This specific type focuses on including equipment or machinery as collateral. Lenders often require this type of agreement when extending loans for the purchase or lease of costly equipment. By securing the equipment, lenders minimize risks associated with loan defaults. 3. Fairfax Virginia Security Agreement Covering Inventory: This agreement pertains explicitly to the borrower's inventory, typically for businesses involved in retail, manufacturing, or wholesale. Lenders use this type of security agreement to secure their interest in the borrower's current and future inventory to protect their investments. In Fairfax Virginia, security agreements covering goods, equipment, inventory, etc., typically outline the terms and conditions of the loan and contain detailed descriptions of the collateral, such as serial numbers, models, or identification markers. These agreements are legally binding and require borrowers to maintain the collateral's value and protect it from damage or loss until they repay the loan in full. It's important to note that Fairfax Virginia Security Agreements are governed by state and federal laws, including the Uniform Commercial Code (UCC), which establishes the legal framework for secured transactions. Lenders may also require additional documents, such as financing statements, to perfect their security interest and ensure they have priority over other creditors. Having a comprehensive Fairfax Virginia Security Agreement Covering Goods, Equipment, Inventory, Etc., in place safeguards both lenders and borrowers and serves as a vital tool to secure loans and maintain financial integrity in business transactions within the state.

Fairfax Virginia Security Agreement Covering Goods, Equipment, Inventory, Etc.

Description

How to fill out Fairfax Virginia Security Agreement Covering Goods, Equipment, Inventory, Etc.?

Do you need to quickly draft a legally-binding Fairfax Security Agreement Covering Goods, Equipment, Inventory, Etc. or maybe any other form to take control of your own or corporate matters? You can go with two options: contact a professional to draft a legal paper for you or draft it entirely on your own. Luckily, there's an alternative solution - US Legal Forms. It will help you receive professionally written legal documents without having to pay unreasonable fees for legal services.

US Legal Forms offers a huge collection of over 85,000 state-compliant form templates, including Fairfax Security Agreement Covering Goods, Equipment, Inventory, Etc. and form packages. We provide templates for an array of use cases: from divorce paperwork to real estate documents. We've been out there for over 25 years and gained a spotless reputation among our customers. Here's how you can become one of them and obtain the needed document without extra troubles.

- To start with, double-check if the Fairfax Security Agreement Covering Goods, Equipment, Inventory, Etc. is adapted to your state's or county's laws.

- In case the form comes with a desciption, make sure to check what it's intended for.

- Start the searching process again if the form isn’t what you were hoping to find by using the search bar in the header.

- Choose the subscription that best suits your needs and move forward to the payment.

- Select the format you would like to get your form in and download it.

- Print it out, complete it, and sign on the dotted line.

If you've already registered an account, you can simply log in to it, find the Fairfax Security Agreement Covering Goods, Equipment, Inventory, Etc. template, and download it. To re-download the form, simply go to the My Forms tab.

It's stressless to find and download legal forms if you use our catalog. In addition, the templates we provide are reviewed by law professionals, which gives you greater confidence when writing legal matters. Try US Legal Forms now and see for yourself!