Nassau New York Grantor Retained Annuity Trust

Description

How to fill out Grantor Retained Annuity Trust?

Creating documents for business or personal needs is consistently a significant obligation.

When formulating a contract, a public service request, or a power of attorney, it's crucial to consider all federal and state regulations of the specific region.

Nevertheless, small counties and even municipalities also possess legislative rules that must be taken into account.

The advantage of the US Legal Forms library is that all the documents you have ever obtained remain accessible - you can view them in your profile within the My documents tab at any time. Join the platform and effortlessly obtain verified legal templates for any situation with just a few clicks!

- All these factors contribute to the pressure and time-consuming nature of preparing a Nassau Grantor Retained Annuity Trust without expert assistance.

- It's straightforward to save on legal fees by drafting your own paperwork and ensuring a legally valid Nassau Grantor Retained Annuity Trust utilizing the US Legal Forms online library.

- It is the largest digital repository of state-specific legal documents that are professionally vetted, ensuring their legitimacy when selecting a document for your county.

- Formerly registered users only need to Log In to their accounts to retrieve the necessary form.

- If you do not have a subscription yet, follow the step-by-step instructions below to acquire the Nassau Grantor Retained Annuity Trust.

- Browse through the page you’ve accessed and confirm if it contains the document you need.

- To accomplish this, utilize the form description and preview if these features are available.

Form popularity

FAQ

Grantor-Retained Income Trust (GRIT) is an old form of Grantor-Retained Trust set up by individuals to reduce taxes on an estate. To create a GRIT, a grantor creates an irrevocable trust that is for a limited period of time, paying taxes at the outset of the trust.

A grantor trust can, in a given case, be either revocable or irrevocable, although most types of grantor trusts involve an irrevocable trust. Certain types of trusts (such, as for example, a revocable trust) are disregarded not only for income tax purposes but also for federal estate and gift tax purposes.

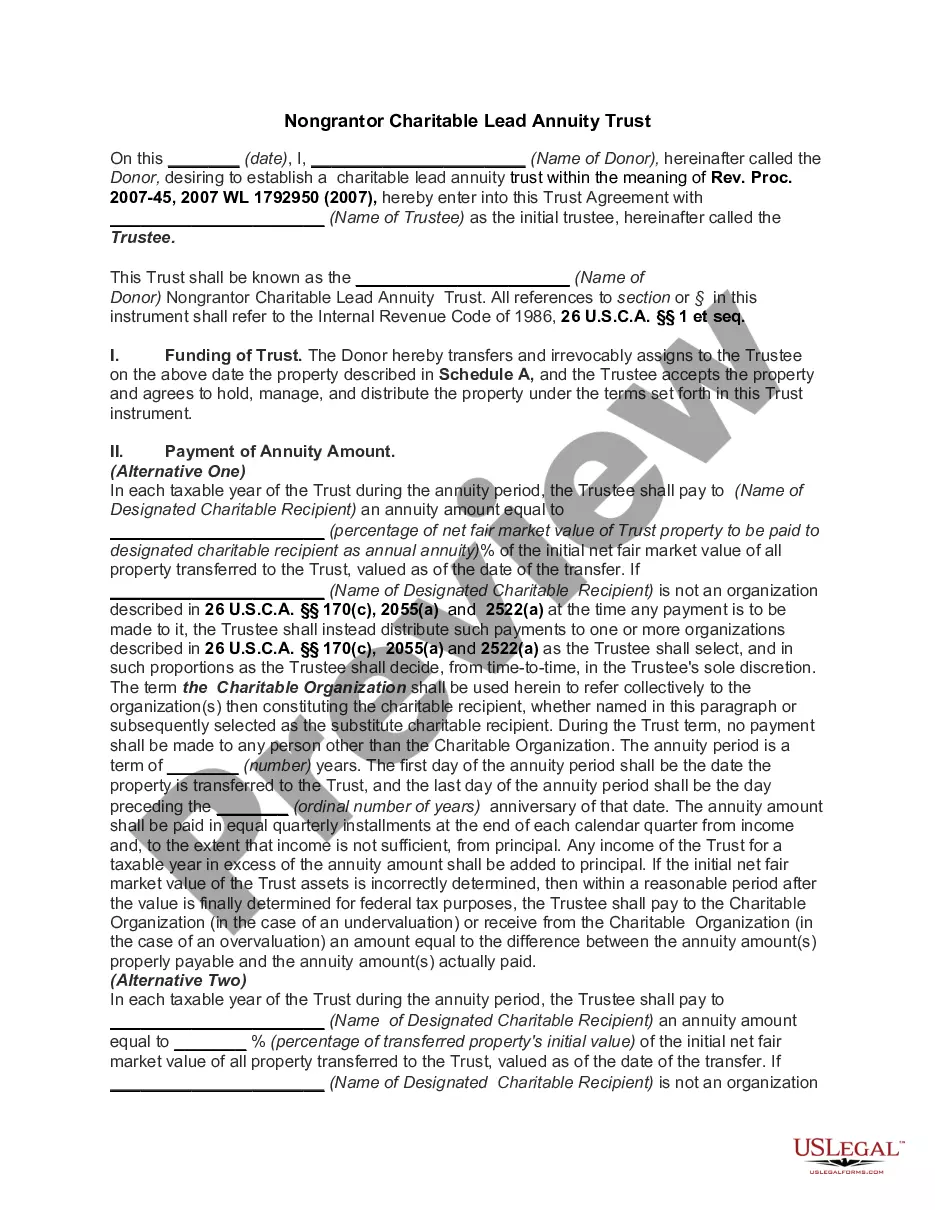

A grantor retained annuity trust, better known as a GRAT, is an irrevocable trust that pays an annuity amount to the grantor for a set period of years, after which the remainder passes to or for the benefit of children or others.

GRATs are taxed in two ways: Any income you earn from the appreciation of your assets in the trust is subject to regular income tax, and any remaining funds/assets that transfer to a beneficiary are subject to gift taxes.

If trust assets generate interest or capital gains, you must report them on your income tax return. Second, since the annuity payments are merely a transfer of principal between the same taxpayer, the annuity payments will not be taxable to you.

The grantor receives annuity payments from the GRAT. The trust is expected to produce a minimum return of at least the IRS Section 7520 interest rate. If it doesn't, the trust uses principal to cover the annuity payment and the GRAT fails, returning trust assets back to the grantor.

The grantor funds a 2-year GRAT, based on the considerations set forth below. This means that she will receive an annuity for two years, and then whatever is left in the GRAT after two years will pass to the grantor's children.

A GRAT is an irrevocable trust that allows the trust's creator known as the grantor to direct certain assets into a temporary trust and freeze its value, removing additional appreciation from the grantor's estate and giving it to heirs with minimal estate or gift tax liability.

During the term of the GRAT, the Donor will be taxed on all of the income and capital gains earned by the trust, without regard to the amount of the annuity paid to the Donor.