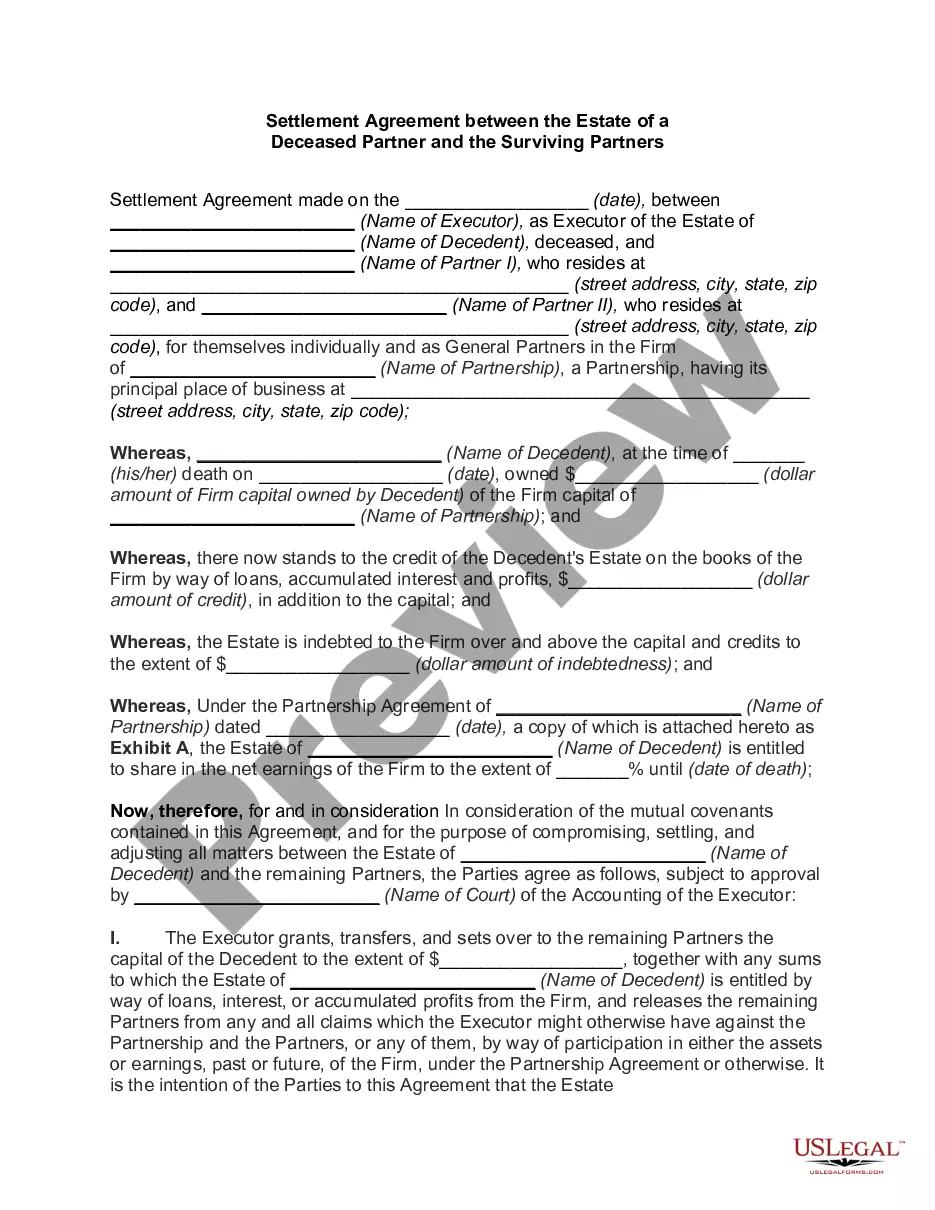

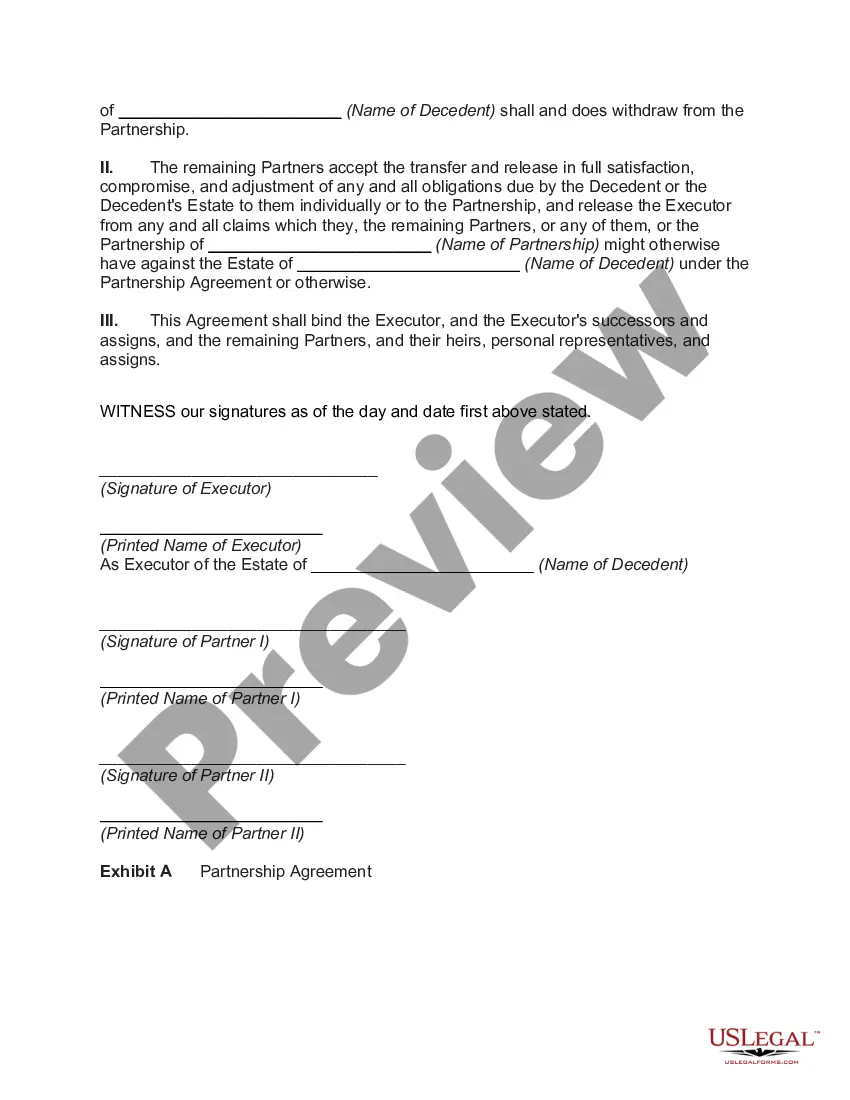

Fairfax Virginia Settlement Agreement between the Estate of a Deceased Partner and the Surviving Partners is a legally binding document that outlines the terms and conditions regarding the distribution of assets, liabilities, and ongoing business operations following the death of a partner in a business located in Fairfax, Virginia. This agreement is crucial to ensure a fair and smooth transition for all parties involved. Keywords: Fairfax Virginia, Settlement Agreement, Estate, Deceased Partner, Surviving Partners, assets, liabilities, business operations, distribution, transition. When a partner in a business located in Fairfax, Virginia passes away, it can significantly impact the operations, financial stability, and future of the company. A Fairfax Virginia Settlement Agreement between the Estate of a Deceased Partner and the Surviving Partners assists in resolving any potential conflicts or uncertainties regarding the division of assets and responsibilities. There are various types of Fairfax Virginia Settlement Agreements that can be tailored to suit the specific circumstances and needs of each situation. These may include: 1. Asset Distribution Agreement: This type of settlement agreement focuses primarily on the fair distribution of the deceased partner's assets among the surviving partners. It ensures that each surviving partner receives their rightful share based on agreed-upon ratios or predetermined arrangements. 2. Liability Allocation Agreement: When a partner passes away, the surviving partners may have concerns about assuming the deceased partner's liabilities. This agreement determines the allocation of these obligations and establishes a clear understanding of who is responsible for settling them. 3. Business Continuity Agreement: In some cases, the surviving partners may decide to continue the business operations after the death of a partner. This agreement outlines the terms and conditions for the continuation of the business, including profit sharing, decision-making authority, and roles and responsibilities of the surviving partners. 4. Dissolution and Wind-Up Agreement: If the surviving partners decide to dissolve the business following the death of a partner, this agreement helps navigate the process of winding down operations, distributing assets, settling liabilities, and terminating any contractual obligations. Regardless of the specific type of settlement agreement, it is crucial to engage legal professionals experienced in Fairfax, Virginia business law to ensure the agreement complies with relevant state laws and protects the rights and interests of all parties involved. The Fairfax Virginia Settlement Agreement between the Estate of a Deceased Partner and the Surviving Partners serves as a pivotal document that outlines the fair and equitable resolution of business matters following the death of a partner. By addressing asset distribution, liability allocation, business continuity, or dissolution and wind-up, this agreement provides clarity, minimizes potential conflicts, and facilitates a smooth transition for the business and all parties involved in Fairfax, Virginia.

Fairfax Virginia Settlement Agreement between the Estate of a Deceased Partner and the Surviving Partners

Description

How to fill out Fairfax Virginia Settlement Agreement Between The Estate Of A Deceased Partner And The Surviving Partners?

Preparing legal paperwork can be difficult. Besides, if you decide to ask a legal professional to write a commercial agreement, documents for ownership transfer, pre-marital agreement, divorce papers, or the Fairfax Settlement Agreement between the Estate of a Deceased Partner and the Surviving Partners, it may cost you a lot of money. So what is the best way to save time and money and draft legitimate forms in total compliance with your state and local laws? US Legal Forms is a great solution, whether you're searching for templates for your individual or business needs.

US Legal Forms is largest online library of state-specific legal documents, providing users with the up-to-date and professionally checked forms for any scenario collected all in one place. Consequently, if you need the current version of the Fairfax Settlement Agreement between the Estate of a Deceased Partner and the Surviving Partners, you can easily find it on our platform. Obtaining the papers takes a minimum of time. Those who already have an account should check their subscription to be valid, log in, and select the sample with the Download button. If you haven't subscribed yet, here's how you can get the Fairfax Settlement Agreement between the Estate of a Deceased Partner and the Surviving Partners:

- Glance through the page and verify there is a sample for your region.

- Check the form description and use the Preview option, if available, to ensure it's the template you need.

- Don't worry if the form doesn't satisfy your requirements - search for the right one in the header.

- Click Buy Now once you find the required sample and choose the best suitable subscription.

- Log in or sign up for an account to purchase your subscription.

- Make a transaction with a credit card or via PayPal.

- Opt for the document format for your Fairfax Settlement Agreement between the Estate of a Deceased Partner and the Surviving Partners and save it.

When done, you can print it out and complete it on paper or import the template to an online editor for a faster and more convenient fill-out. US Legal Forms allows you to use all the paperwork ever purchased multiple times - you can find your templates in the My Forms tab in your profile. Try it out now!