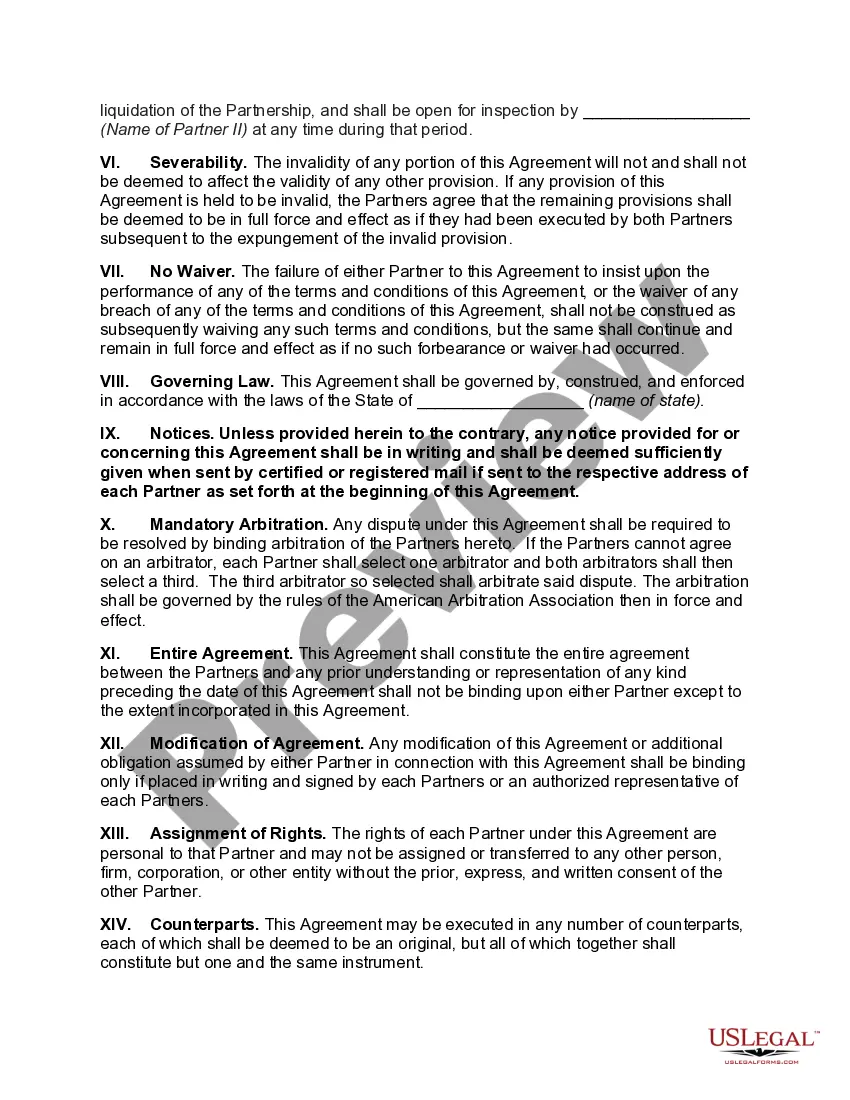

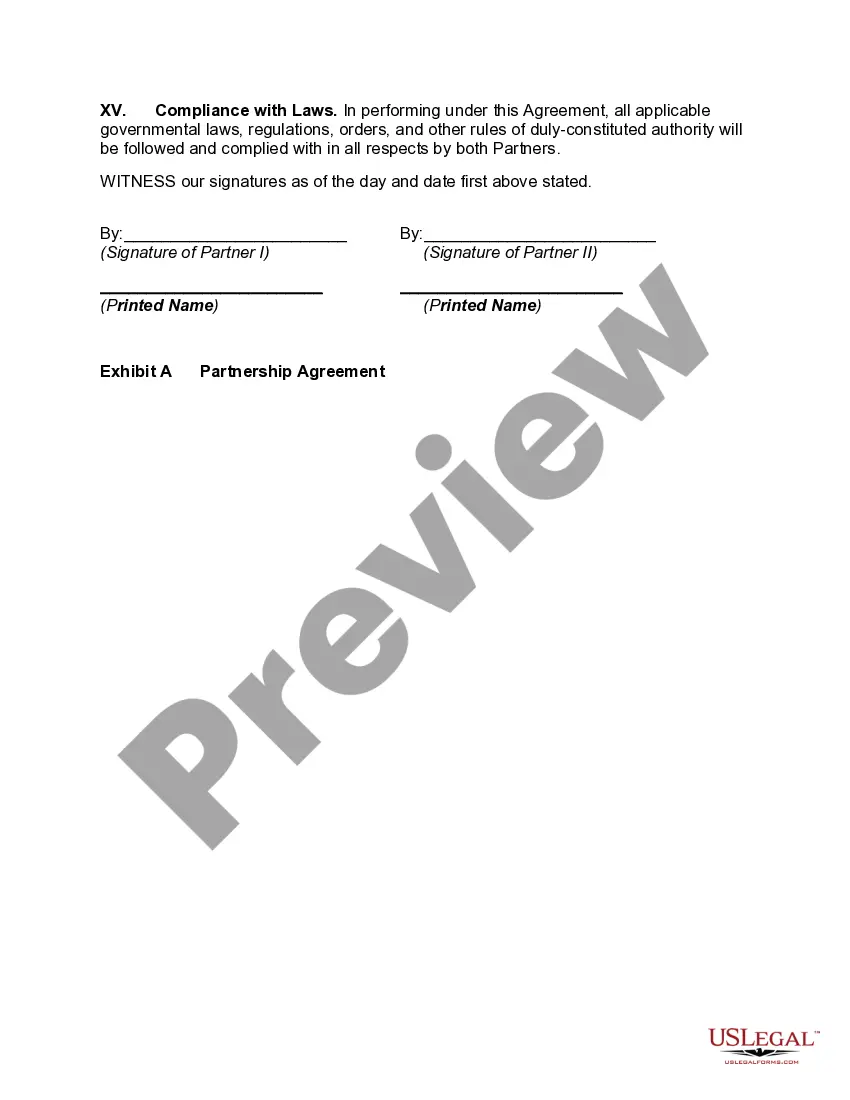

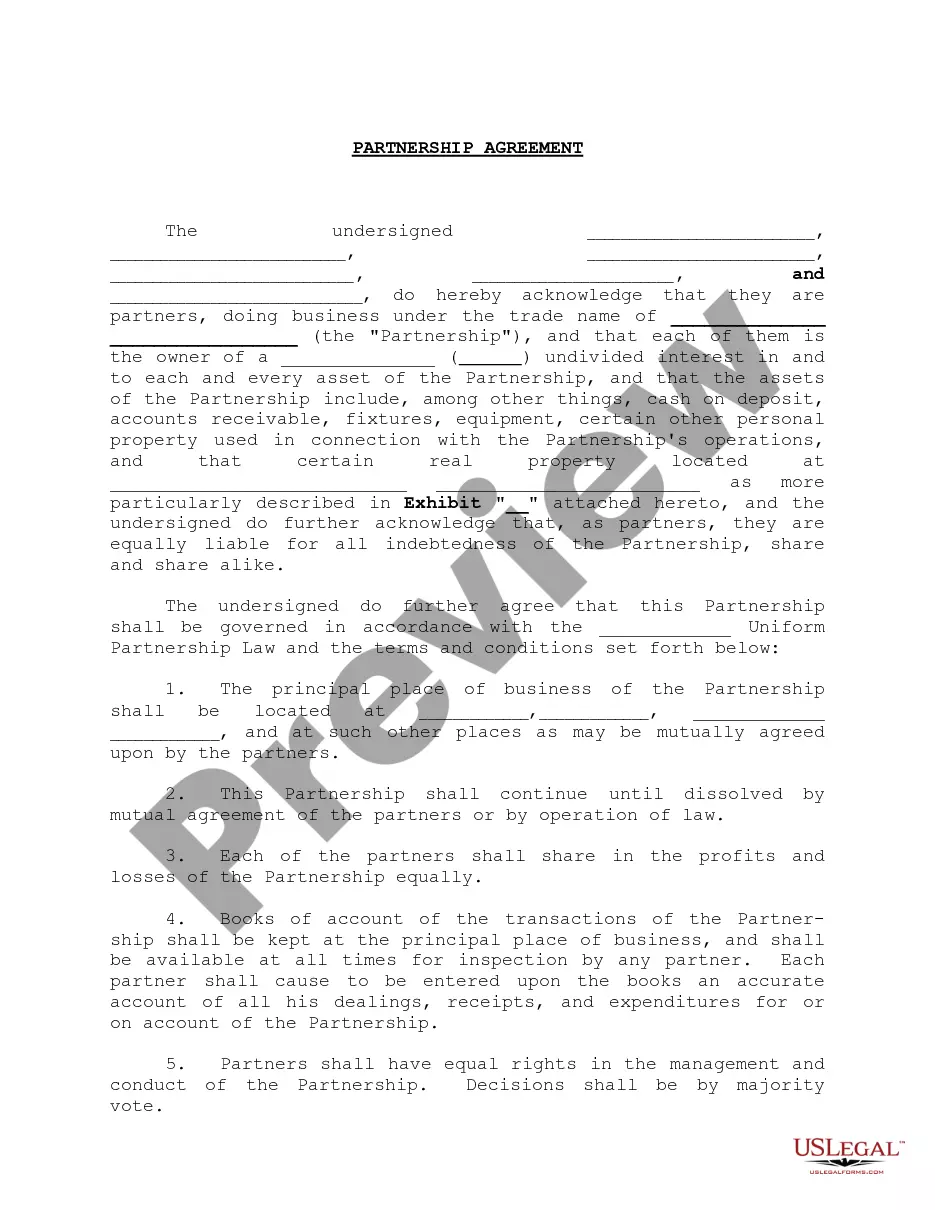

Wayne Michigan Liquidation of Partnership with Sale and Proportional Distribution of Assets

Description

How to fill out Wayne Michigan Liquidation Of Partnership With Sale And Proportional Distribution Of Assets?

Dealing with legal forms is a necessity in today's world. Nevertheless, you don't always need to look for qualified assistance to draft some of them from scratch, including Wayne Liquidation of Partnership with Sale and Proportional Distribution of Assets, with a platform like US Legal Forms.

US Legal Forms has more than 85,000 templates to select from in different types varying from living wills to real estate papers to divorce papers. All forms are organized according to their valid state, making the searching experience less frustrating. You can also find information resources and tutorials on the website to make any tasks related to paperwork execution simple.

Here's how you can locate and download Wayne Liquidation of Partnership with Sale and Proportional Distribution of Assets.

- Take a look at the document's preview and description (if provided) to get a basic information on what you’ll get after getting the form.

- Ensure that the document of your choosing is specific to your state/county/area since state laws can affect the legality of some records.

- Examine the similar document templates or start the search over to locate the correct file.

- Hit Buy now and register your account. If you already have an existing one, select to log in.

- Choose the option, then a needed payment gateway, and buy Wayne Liquidation of Partnership with Sale and Proportional Distribution of Assets.

- Choose to save the form template in any offered file format.

- Visit the My Forms tab to re-download the file.

If you're already subscribed to US Legal Forms, you can locate the needed Wayne Liquidation of Partnership with Sale and Proportional Distribution of Assets, log in to your account, and download it. Needless to say, our platform can’t take the place of a lawyer entirely. If you need to cope with an extremely difficult case, we advise using the services of a lawyer to examine your form before signing and filing it.

With more than 25 years on the market, US Legal Forms became a go-to provider for various legal forms for millions of users. Join them today and purchase your state-specific paperwork effortlessly!

Form popularity

FAQ

If the liquidated distribution is in cash, the partner is liable to pay tax on it immediately. For the liquidated distribution of fixed assets, such as property that takes time to convert into cash, the tax effect may be delayed until it is converted into cash.

Any post-distribution gain or loss by the partner from the sale of unrealized receivables and from inventory held for less than five years will give rise to ordinary income. These items are reported on Form 4797.

It is often the case that the shareholder, as well as the corporation, will recognize income on the distribution. Partnership distributions of non-cash property typically result in no tax; corporate distributions of non-cash property typically result in a double tax.

43 The U.S. corporation could use a portion of the sales proceeds to repay debt, then adopt a plan of liquidation and distribute the remaining proceeds to its nonresident alien individual shareholder as a liquidating distribution, which can be paid free of any U.S. withholding tax.

Partnership withdrawals Partners withdrawing from the partnership are not taxed to the extent the withdrawal is a return of the partner's investment. In other words, any return or withdrawal paid to the partner up to and including the partner's capital investment will be non-taxable for the partner.

Upon liquidation of a partnership, the Internal Revenue Service views the distributions as a sale of a partnership interest; as a result, gains are generally taxed as long-term capital gains to partners.

Goes out of business and the net assets of the company (after all liabilities have been paid) are distributed to shareholders, or. Sells a portion of its business for cash and the proceeds are distributed to shareholders.

For federal income tax purposes, each shareholder's receipt of the liquidating corporate distribution amount is treated as a sale of all the shareholder's stock in exchange for the distribution.

There are 2 types of distributions: a current distribution decreases the partner's capital account without terminating it, whereas a liquidating distribution pays the entire capital account to the partner, thereby eliminating the partner's equity interest in the partnership.