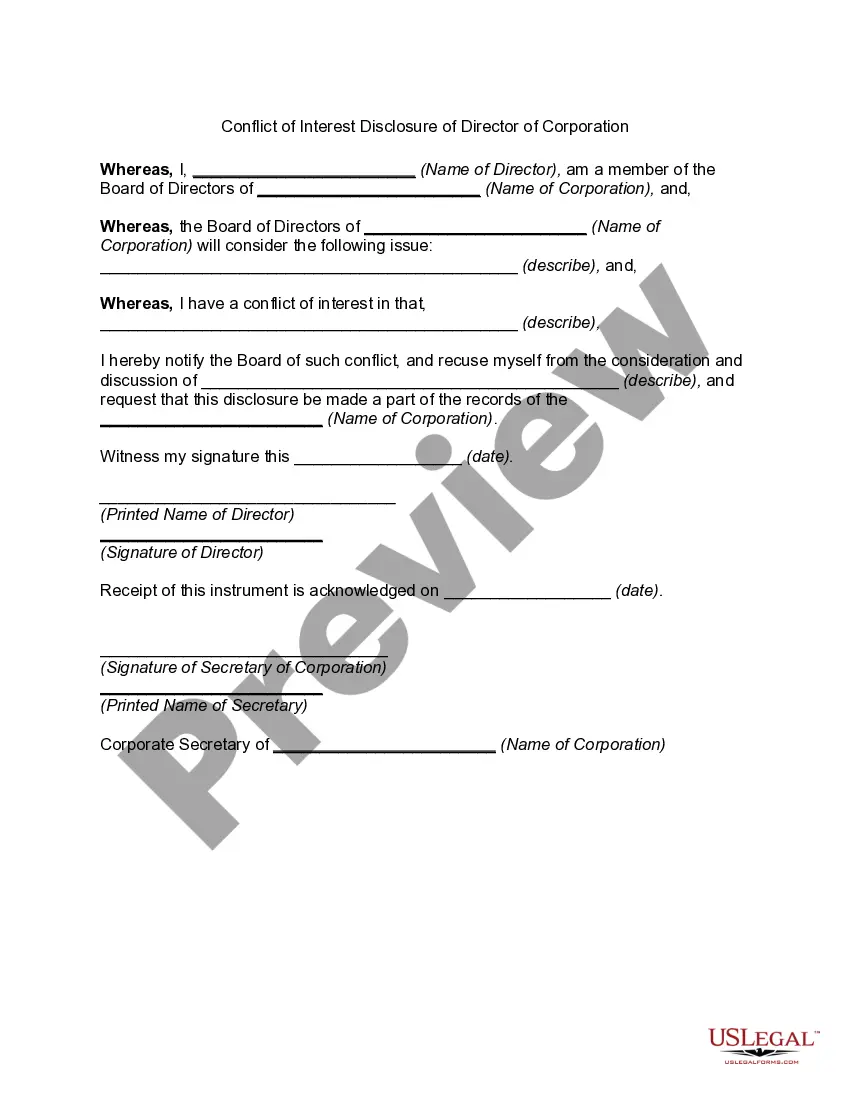

The Cook Illinois Conflict of Interest Disclosure requires directors of corporations to report any potential conflicts of interest that may arise while serving in their role. This disclosure is essential for ensuring transparency, accountability, and ethical practices within the corporation's decision-making process. By identifying and addressing conflicts of interest, the corporation can protect its reputation and maintain the trust of stakeholders. Understanding the Cook Illinois Conflict of Interest Disclosure is crucial for directors to uphold their fiduciary duties and act in the best interests of the corporation. Directors must disclose any personal, financial, or professional relationships that could potentially interfere with their ability to make unbiased decisions. This includes relationships with suppliers, competitors, clients, or any other parties that may have a vested interest in the corporation's operations or outcomes. In order to submit a comprehensive disclosure, directors must disclose the nature of the conflict, the parties involved, and the potential impact it may have on the corporation. They should also outline any actions taken to mitigate or manage the conflict in an effort to maintain transparency and address any potential ethical concerns. Different types of Cook Illinois Conflict of Interest Disclosures may include, but are not limited to: 1. Financial Conflict of Interest: This occurs when the director has a financial stake, such as ownership, investments, or partnerships, that could influence their decision-making in favor of their personal financial gain. 2. Family or Personal Relationships Conflict of Interest: Directors must disclose any family or close personal relationships that may influence their judgment or create biases in decision-making processes. 3. Professional Conflict of Interest: This includes situations where the director has a professional affiliation, consulting arrangement, or employment with a company or organization that may create a conflict between their duties as a director and their external responsibilities. 4. Indirect Conflict of Interest: Directors should also disclose any indirect conflicts of interest that may arise from their involvement with organizations or entities connected to the corporation, such as overlapping board positions or advisory roles. By maintaining open lines of communication and adhering to the Cook Illinois Conflict of Interest Disclosure guidelines, corporations can effectively address and mitigate conflicts of interest. This fosters a culture of trust, integrity, and fair decision-making, which ultimately benefits both the corporation and its stakeholders. Keywords: Cook Illinois, conflict of interest, disclosure, director, corporation, transparency, accountability, ethical practices, fiduciary duties, unbiased decisions, relationships, financial conflict of interest, family relationships, personal relationships, professional conflict of interest, indirect conflict of interest, stakeholders, decision-making process, corporations, reputation, trust, ethical concerns, mitigate, manage, judgment, biases, guidelines, integrity, fair decision-making.

Cook Illinois Conflict of Interest Disclosure of Director of Corporation

Description

How to fill out Cook Illinois Conflict Of Interest Disclosure Of Director Of Corporation?

Laws and regulations in every sphere differ from state to state. If you're not an attorney, it's easy to get lost in a variety of norms when it comes to drafting legal documents. To avoid expensive legal assistance when preparing the Cook Conflict of Interest Disclosure of Director of Corporation, you need a verified template valid for your county. That's when using the US Legal Forms platform is so beneficial.

US Legal Forms is a trusted by millions online catalog of more than 85,000 state-specific legal templates. It's an excellent solution for specialists and individuals searching for do-it-yourself templates for different life and business occasions. All the documents can be used multiple times: once you obtain a sample, it remains accessible in your profile for subsequent use. Thus, if you have an account with a valid subscription, you can simply log in and re-download the Cook Conflict of Interest Disclosure of Director of Corporation from the My Forms tab.

For new users, it's necessary to make some more steps to get the Cook Conflict of Interest Disclosure of Director of Corporation:

- Take a look at the page content to ensure you found the appropriate sample.

- Utilize the Preview option or read the form description if available.

- Search for another doc if there are inconsistencies with any of your requirements.

- Use the Buy Now button to obtain the template when you find the correct one.

- Choose one of the subscription plans and log in or sign up for an account.

- Select how you prefer to pay for your subscription (with a credit card or PayPal).

- Select the format you want to save the document in and click Download.

- Fill out and sign the template in writing after printing it or do it all electronically.

That's the simplest and most affordable way to get up-to-date templates for any legal purposes. Locate them all in clicks and keep your paperwork in order with the US Legal Forms!