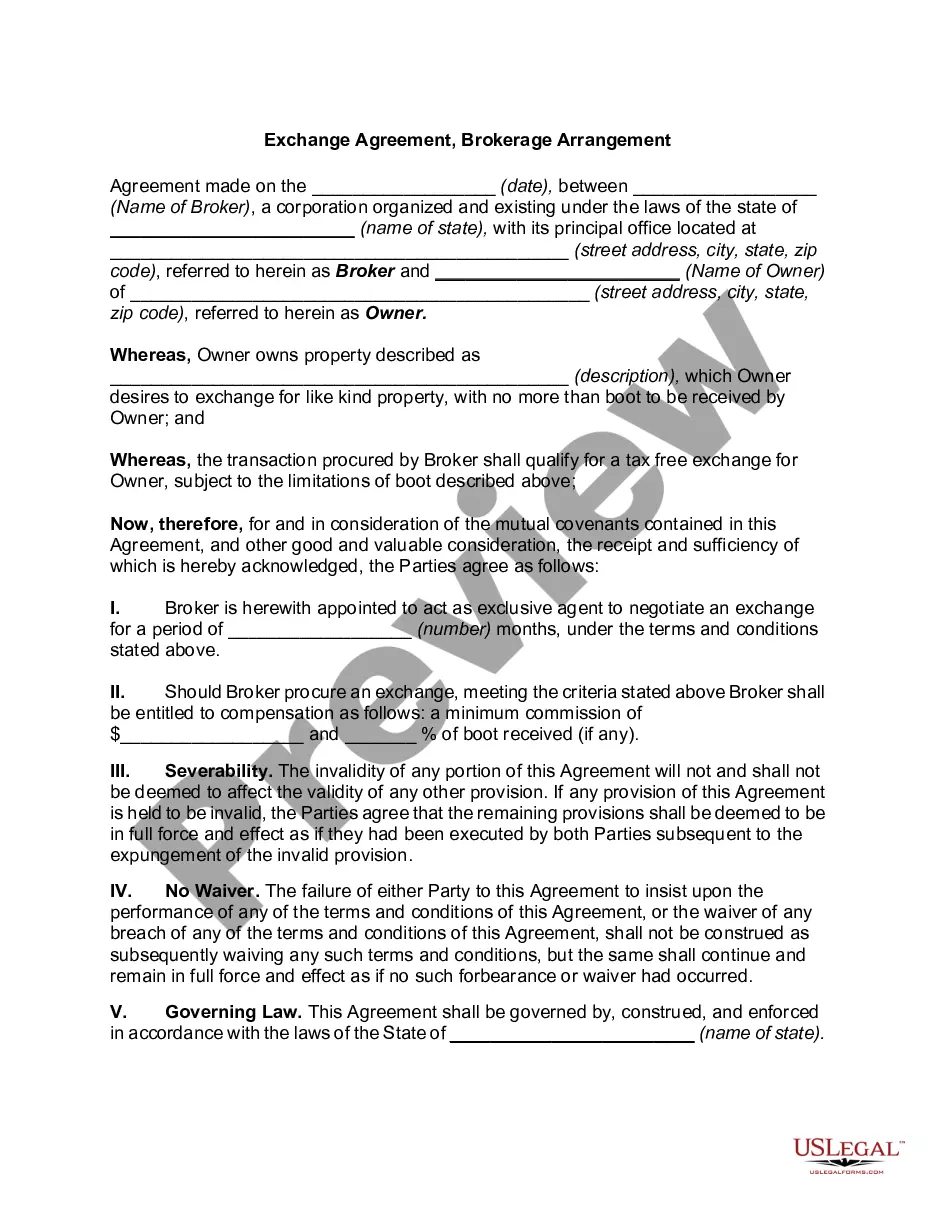

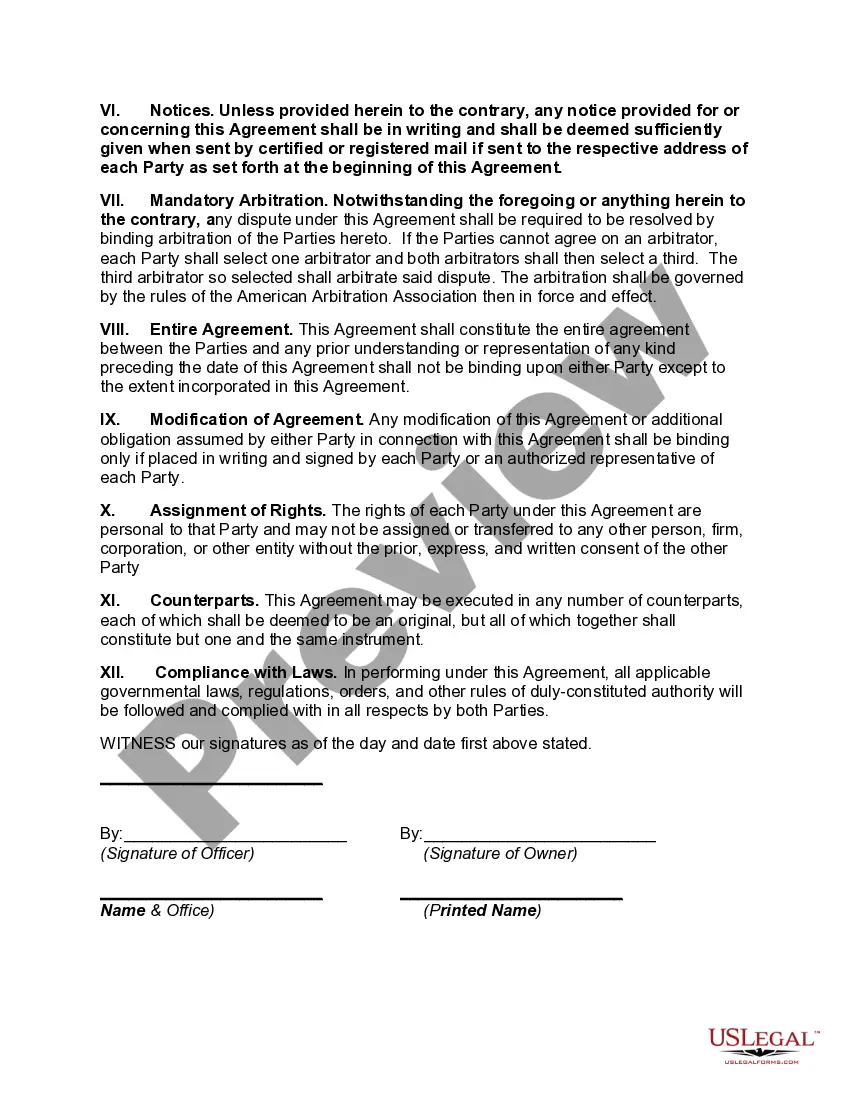

Collin Texas Exchange Agreement: The Collin Texas Exchange Agreement, also known as the 1031 Exchange Agreement, is a legal arrangement that allows property owners to exchange one investment property for another without incurring immediate tax liability on the capital gains. This agreement is governed by the Internal Revenue Code Section 1031 and has specific requirements that need to be fulfilled to qualify for tax-deferred treatment. The purpose behind the Collin Texas Exchange Agreement is to encourage real estate investments and promote economic growth. It provides property owners with the ability to leverage their investments by deferring taxes and reinvesting the proceeds into more valuable properties, thereby facilitating the growth of their real estate portfolios. Brokerage Arrangement: In the context of the Collin Texas Exchange Agreement, a brokerage arrangement refers to the involvement of a qualified intermediary or exchange facilitator who facilitates the 1031 exchange process between the parties involved. A qualified intermediary is a neutral third-party who plays a crucial role in ensuring that the exchange adheres to the rules and guidelines set forth by the IRS. Key responsibilities of a qualified intermediary include: 1. Facilitating the identification of replacement properties within certain timeframes. 2. Holding the proceeds from the sale of the relinquished property in a separate escrow or trust account. 3. Assisting in the preparation of necessary documentation, such as exchange agreements, assignments, and escrow instructions. 4. Ensuring compliance with all IRS guidelines and regulations. Different Types of Collin Texas Exchange Agreement and Brokerage Arrangement: 1. Delayed Exchange: This is the most common type of Collin Texas Exchange Agreement, wherein the disposition of the relinquished property occurs first, followed by the acquisition of the replacement property within certain timelines. The qualified intermediary holds the sale proceeds until the replacement property is acquired. 2. Simultaneous Exchange: In a simultaneous exchange, the disposition of the relinquished property and the acquisition of the replacement property happen concurrently. The qualified intermediary ensures that the timing of both transactions aligns effectively, allowing for a seamless exchange. 3. Reverse Exchange: In a reverse exchange, the acquisition of the replacement property happens before the disposition of the relinquished property. This type of exchange requires additional coordination and may involve the use of an Exchange Accommodation Titleholder (EAT) entity to hold the acquired property until the relinquished property is sold. It's important to note that engaging in Collin Texas Exchange Agreement, Brokerage Arrangement requires proper guidance from tax and legal professionals with experience in 1031 exchanges. Each exchange situation may have unique complexities, and it's crucial to comply with all IRS regulations to ensure a successful and tax-deferred exchange.

Collin Texas Exchange Agreement, Brokerage Arrangement

Description

How to fill out Collin Texas Exchange Agreement, Brokerage Arrangement?

Do you need to quickly create a legally-binding Collin Exchange Agreement, Brokerage Arrangement or maybe any other form to handle your personal or corporate matters? You can select one of the two options: contact a legal advisor to draft a valid paper for you or draft it entirely on your own. The good news is, there's another option - US Legal Forms. It will help you receive neatly written legal papers without having to pay sky-high prices for legal services.

US Legal Forms provides a rich catalog of over 85,000 state-compliant form templates, including Collin Exchange Agreement, Brokerage Arrangement and form packages. We offer templates for an array of life circumstances: from divorce paperwork to real estate document templates. We've been out there for more than 25 years and got a rock-solid reputation among our customers. Here's how you can become one of them and get the needed document without extra troubles.

- To start with, carefully verify if the Collin Exchange Agreement, Brokerage Arrangement is tailored to your state's or county's laws.

- If the form has a desciption, make sure to verify what it's suitable for.

- Start the searching process over if the template isn’t what you were hoping to find by utilizing the search bar in the header.

- Choose the subscription that is best suited for your needs and move forward to the payment.

- Choose the format you would like to get your form in and download it.

- Print it out, complete it, and sign on the dotted line.

If you've already registered an account, you can easily log in to it, locate the Collin Exchange Agreement, Brokerage Arrangement template, and download it. To re-download the form, just go to the My Forms tab.

It's stressless to buy and download legal forms if you use our catalog. In addition, the documents we provide are updated by industry experts, which gives you greater confidence when dealing with legal matters. Try US Legal Forms now and see for yourself!