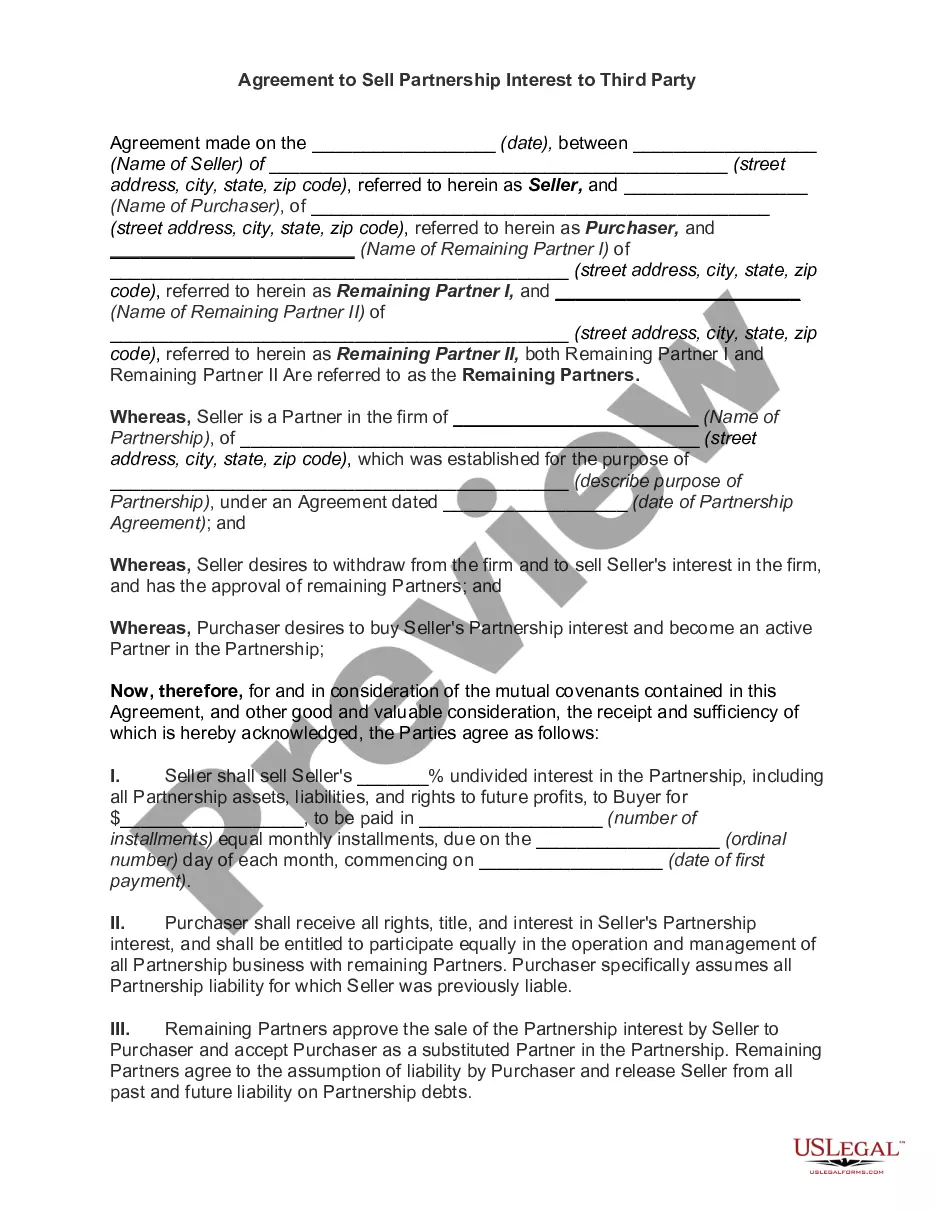

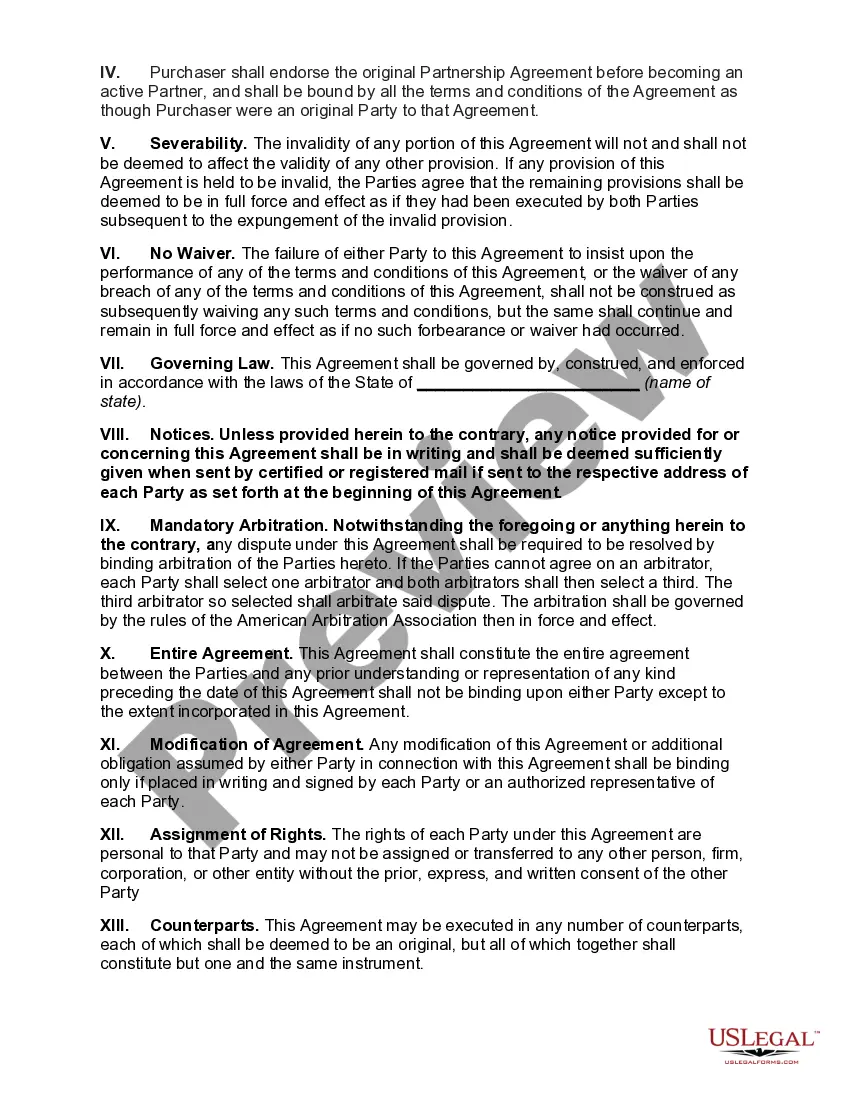

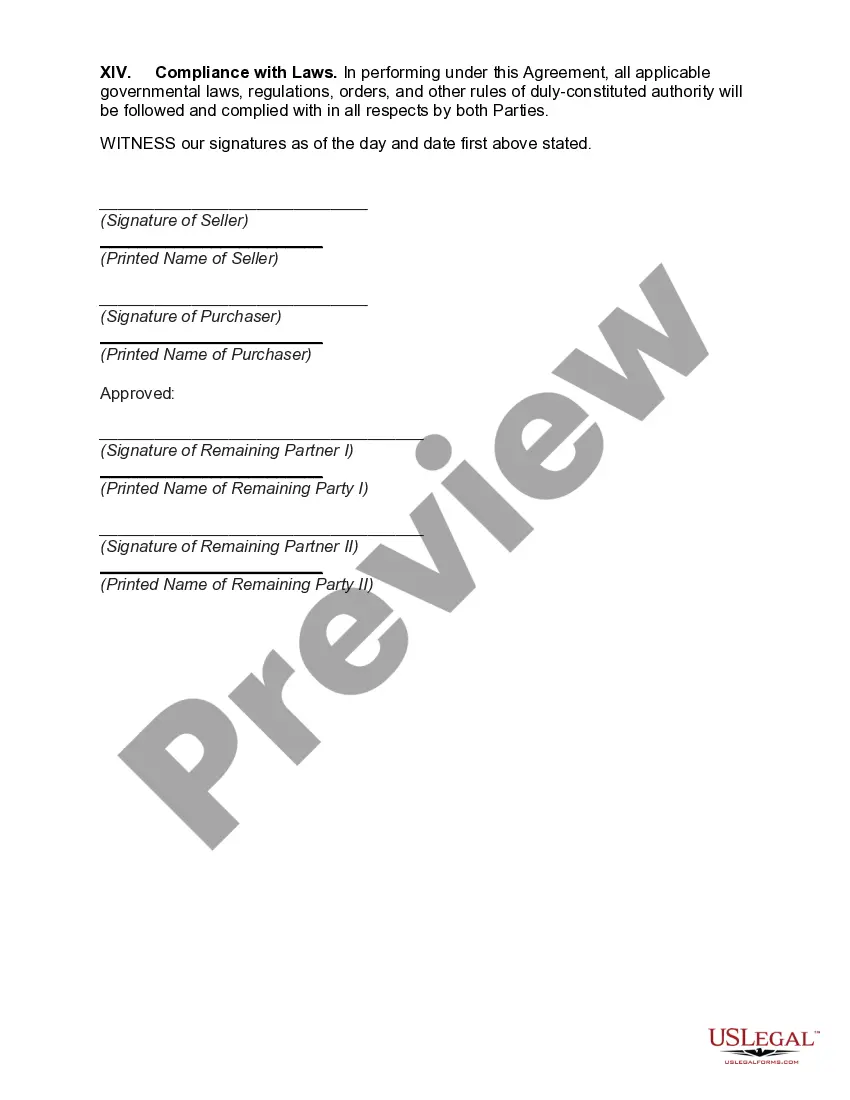

Orange California Agreement to Sell Partnership Interest to Third Party

Description

How to fill out Orange California Agreement To Sell Partnership Interest To Third Party?

How much time does it normally take you to draft a legal document? Considering that every state has its laws and regulations for every life scenario, locating a Orange Agreement to Sell Partnership Interest to Third Party meeting all regional requirements can be tiring, and ordering it from a professional attorney is often costly. Many web services offer the most popular state-specific documents for download, but using the US Legal Forms library is most advantegeous.

US Legal Forms is the most comprehensive web catalog of templates, gathered by states and areas of use. In addition to the Orange Agreement to Sell Partnership Interest to Third Party, here you can find any specific document to run your business or individual affairs, complying with your regional requirements. Experts check all samples for their validity, so you can be certain to prepare your paperwork properly.

Using the service is fairly straightforward. If you already have an account on the platform and your subscription is valid, you only need to log in, select the required sample, and download it. You can retain the document in your profile at any time later on. Otherwise, if you are new to the platform, there will be some extra steps to complete before you get your Orange Agreement to Sell Partnership Interest to Third Party:

- Examine the content of the page you’re on.

- Read the description of the sample or Preview it (if available).

- Search for another document using the corresponding option in the header.

- Click Buy Now when you’re certain in the selected document.

- Choose the subscription plan that suits you most.

- Create an account on the platform or log in to proceed to payment options.

- Make a payment via PalPal or with your credit card.

- Switch the file format if necessary.

- Click Download to save the Orange Agreement to Sell Partnership Interest to Third Party.

- Print the doc or use any preferred online editor to complete it electronically.

No matter how many times you need to use the acquired document, you can locate all the files you’ve ever saved in your profile by opening the My Forms tab. Give it a try!

Form popularity

FAQ

Transferring ownership of a partnership depends on what type of interest is being transferred. Partnerships can have two forms: general and limited....Final overview Review the partnership agreement. Obtain a valuation. Decide whether to use an interest sale agreement. Amend the partnership agreement.

When a partnership interest is sold, gain or loss is determined by the amount of the sale minus the partner's interest, often called the partner's outside basis.

2012 Review Schedule D, Form 8949 and Form 4797 to determine the amount of gain or loss the partner reported on the sale of the partnership interest. After determining a partner sold its interest in the partnership, establish other relevant facts that can impact the tax treatment of this transaction.

The sale of a partnership interest is generally treated as a sale of a capital asset, resulting in capital gain or loss for the selling partner.

Unilateral Ownership Transfer Most states have modeled their partnership laws after the Revised Uniform Partnership Act, which allows a partner to transfer his economic interest in the partnership to a third party without the consent of the other partners.

Because tax law views a partnership both as an entity and as an aggregate of partners, the sale of a partnership interest may result either in a capital gain or loss or all or a portion of the gain may be taxed as ordinary income.

Transferring Interest A new partnership will be formed between the member to whom the interest was transferred and the remaining members of the first partnership. This new partnership will be expected to continue on in the business of the first partnership.

Summary. The sale of a partnership interest is generally treated as the sale of a capital asset. As a result, the sale of a partnership interest will generally generate capital gain or loss for the difference between the amount realized on the sale and the partner's adjusted basis in the partnership interest.

A sale of a partnership interest occurs when one partner sells their ownership interest to another person or entity. The partnership is generally not involved in the transaction. However, the buyer and seller will notify the partnership of the transaction.

The sale of a partnership interest is generally treated as a sale of a capital asset, resulting in capital gain or loss for the selling partner.