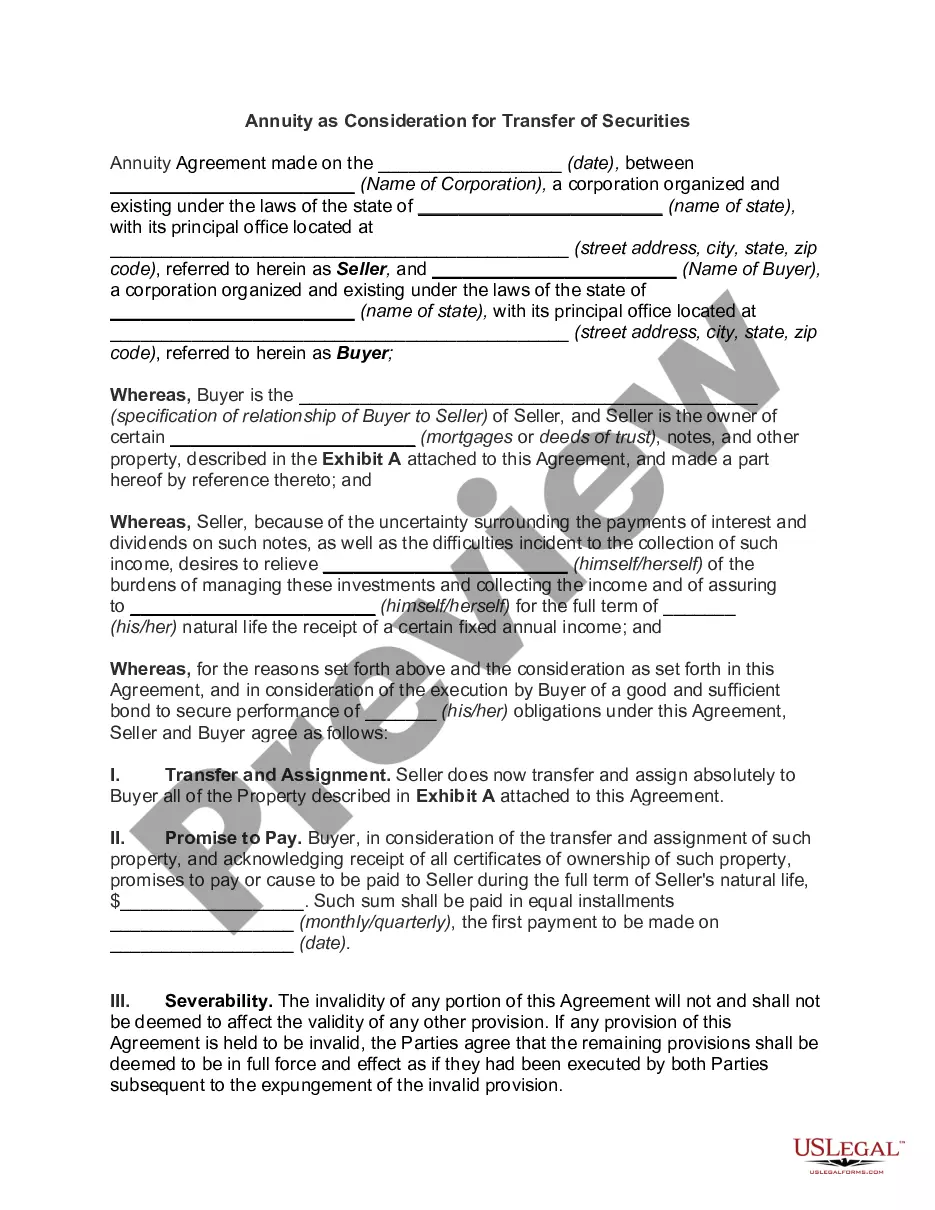

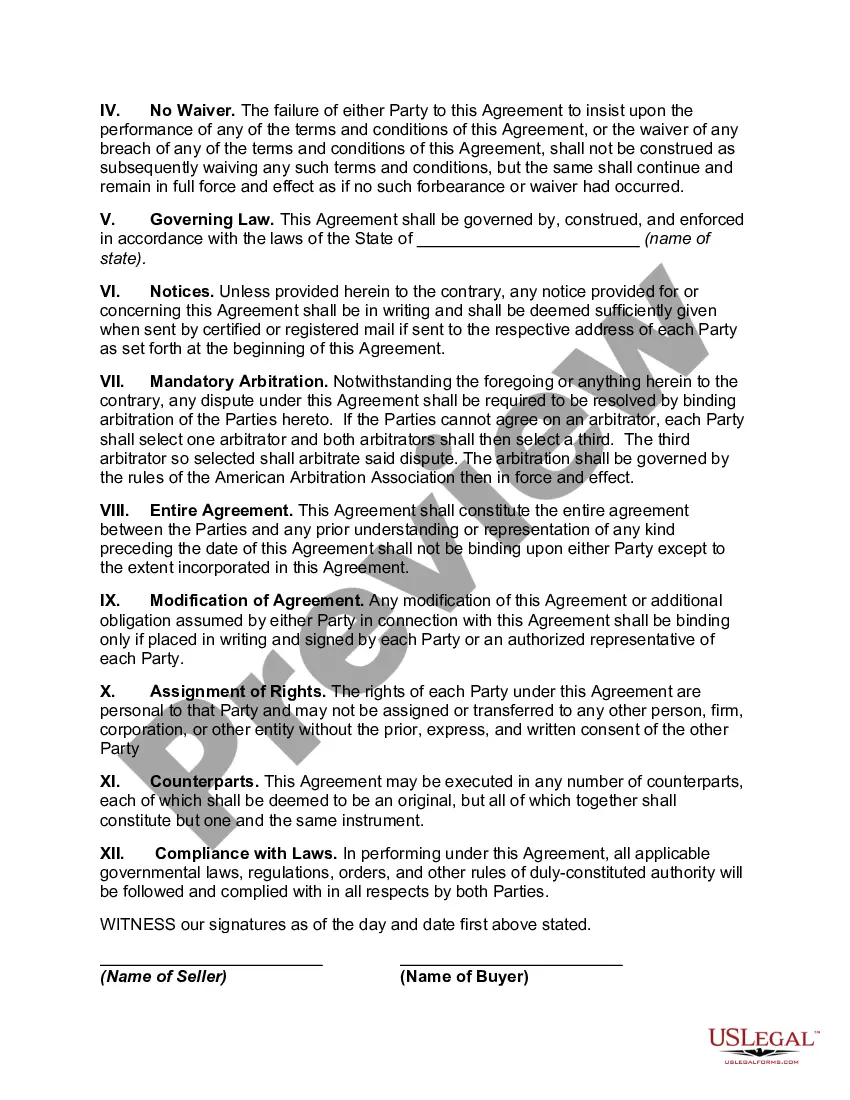

Middlesex Massachusetts Annuity as Consideration for Transfer of Securities is a financial arrangement that involves the transfer of securities in exchange for an annuity provided by Middlesex Massachusetts. An annuity is a type of financial product that pays a regular income over a specific period or for the remainder of an individual's life. It serves as a form of income stream or retirement plan. Middlesex Massachusetts offers various types of annuities as consideration for the transfer of securities, including: 1. Fixed Annuities: These annuities offer a guaranteed fixed rate of return and consistent income payments. They provide stability and security as they are not affected by market fluctuations. 2. Variable Annuities: Unlike fixed annuities, variable annuities offer the potential for higher returns as they are tied to the performance of investment portfolios. They allow individuals to invest in a range of securities, such as stocks and bonds, offering more flexibility but also exposing the investor to market risks. 3. Immediate Annuities: Immediate annuities are designed to provide an income stream that starts immediately after the initial investment. They are typically purchased by individuals nearing retirement or those needing an immediate income source. 4. Deferred Annuities: Deferred annuities involve a waiting period between the initial investment and the start of the annuity payments. During the accumulation phase, the invested funds can grow tax-deferred, potentially leading to higher returns to the future. This type of annuity is often chosen by individuals looking to supplement their retirement income. Middlesex Massachusetts Annuity as Consideration for Transfer of Securities provides investors with a reliable income stream while enabling them to diversify their investment portfolio. It offers individuals the opportunity to convert their securities into a steady income source, ensuring financial stability and peace of mind during retirement. By tailoring the annuity to meet specific financial goals and risk tolerance, Middlesex Massachusetts assists individuals in making informed decisions that align with their long-term financial objectives.

Middlesex Massachusetts Annuity as Consideration for Transfer of Securities

Description

How to fill out Middlesex Massachusetts Annuity As Consideration For Transfer Of Securities?

Laws and regulations in every sphere vary throughout the country. If you're not an attorney, it's easy to get lost in various norms when it comes to drafting legal paperwork. To avoid costly legal assistance when preparing the Middlesex Annuity as Consideration for Transfer of Securities, you need a verified template legitimate for your county. That's when using the US Legal Forms platform is so beneficial.

US Legal Forms is a trusted by millions online library of more than 85,000 state-specific legal forms. It's an excellent solution for professionals and individuals searching for do-it-yourself templates for various life and business scenarios. All the forms can be used many times: once you obtain a sample, it remains accessible in your profile for future use. Thus, when you have an account with a valid subscription, you can simply log in and re-download the Middlesex Annuity as Consideration for Transfer of Securities from the My Forms tab.

For new users, it's necessary to make a few more steps to obtain the Middlesex Annuity as Consideration for Transfer of Securities:

- Analyze the page content to ensure you found the correct sample.

- Take advantage of the Preview option or read the form description if available.

- Look for another doc if there are inconsistencies with any of your requirements.

- Use the Buy Now button to get the template once you find the correct one.

- Opt for one of the subscription plans and log in or create an account.

- Select how you prefer to pay for your subscription (with a credit card or PayPal).

- Pick the format you want to save the document in and click Download.

- Complete and sign the template in writing after printing it or do it all electronically.

That's the easiest and most economical way to get up-to-date templates for any legal reasons. Find them all in clicks and keep your paperwork in order with the US Legal Forms!

Form popularity

FAQ

Non-IRA Transfer When you want to transfer a non-IRA annuity (aka: non-qualified annuity) to another non-IRA annuity, this is a non-taxable event that is called a 1035 exchange. The number 1035 refers to the IRS Code number that explains this type of annuity to annuity transfer.

An annuity is a financial product offered by insurance companies to provide investors with a steady income stream in retirement. Investors make a lump sum payment or a series of payments, and the annuity pays a specific amount back to them in regular distributions either immediately or at some point in the future.

Most annuities allow the contract owner to change the annuitant at any time. The annuitant is the individual named under the annuity contract whose life will serve as the measuring life to determine benefits to be paid out under the contract.

EXAMPLE: LIFE INSURANCE & ANNUITIES The proceeds will generally be included in your gross estate. However, if you do not retain any incidents of ownership in the policy and the policy proceeds are not payable to your estate, then the proceeds will not be included in your gross estate.

When an annuity contract transfers from one individual to another, the transferred amount is treated as a distribution. The original owner is taxed on any tax-deferred gain and possibly subject to a 10% penalty.

As long as you do not withdraw your investment gains and keep them in the annuity, they are not taxed. A variable annuity is linked to market performance. If you do not withdraw your earnings from the investments in the annuity, they are tax-deferred until you withdraw them.

Changing the Owner The owner of a nonqualified annuity can sell the policy to a new owner and treat the sale proceeds as ordinary income. The current owner can give the annuity to a new owner and pay taxes on the excess of the surrender value above the cost basis.

The main difference between this and owning stocks outright is that the portfolio is inside an annuity. Everything else is pretty much the same same asset class, same type of returns, same investment risk. But the annuity provides additional features that are not available through common stock ownership.

Variable annuities are securities and under FINRA's jurisdiction. Annuities are often products investors consider when they plan for retirementso it pays to understand them. They also are often marketed as tax-deferred savings products.

To give the annuity away, you simply contact the insurance company and state that you want to gift the ownership of the annuity policy to someone else or a trust.