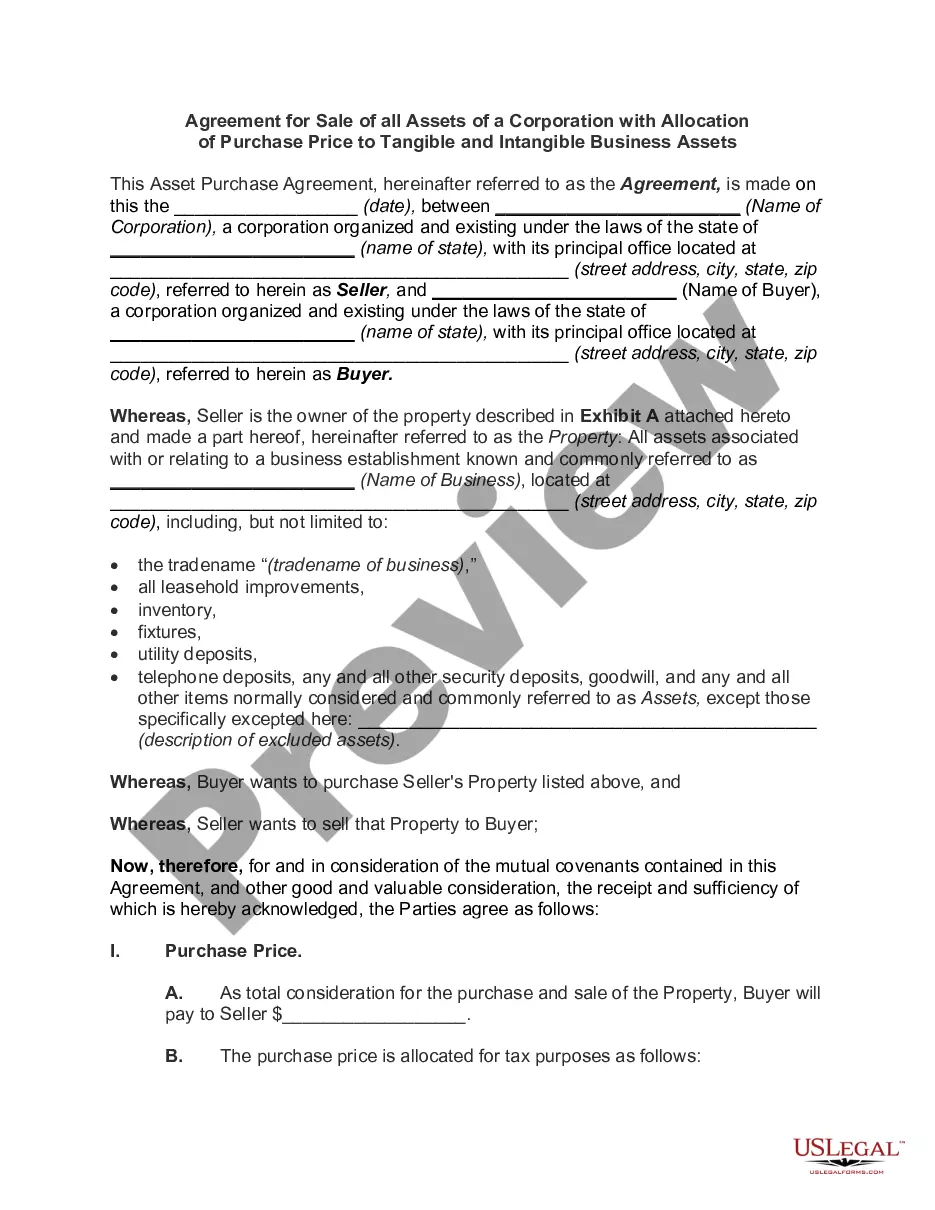

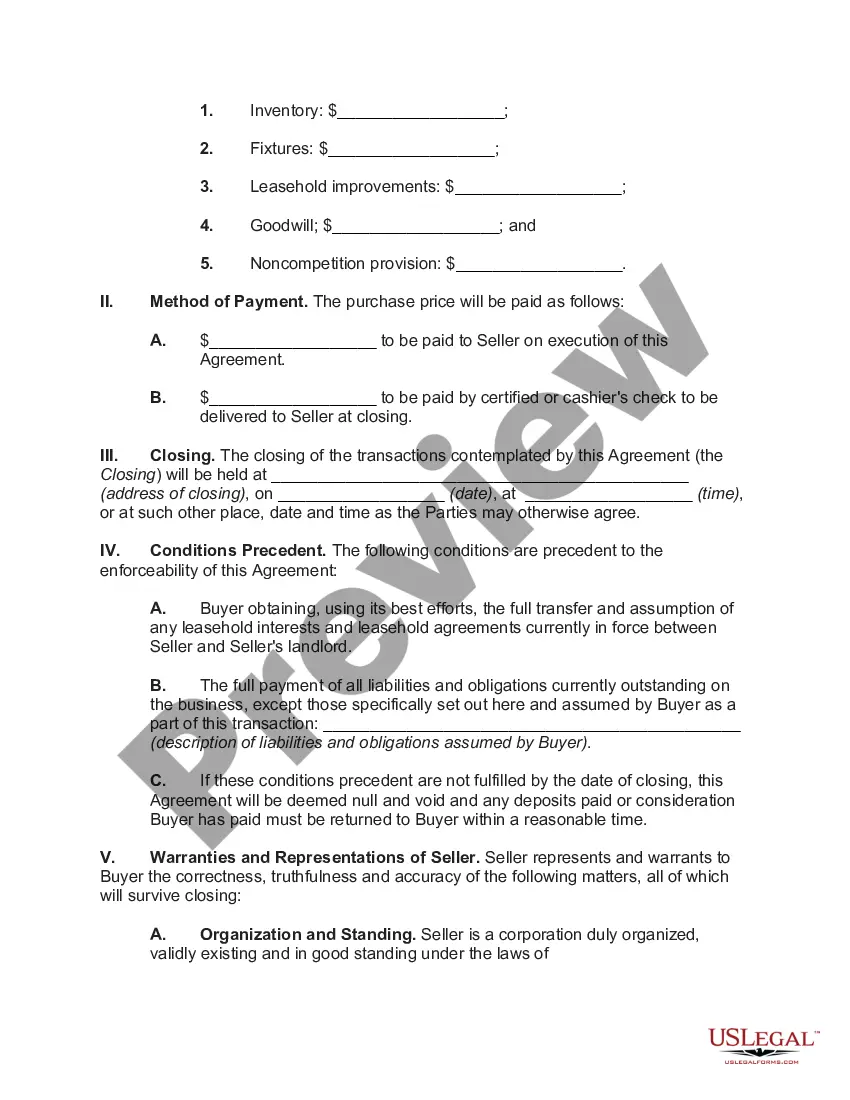

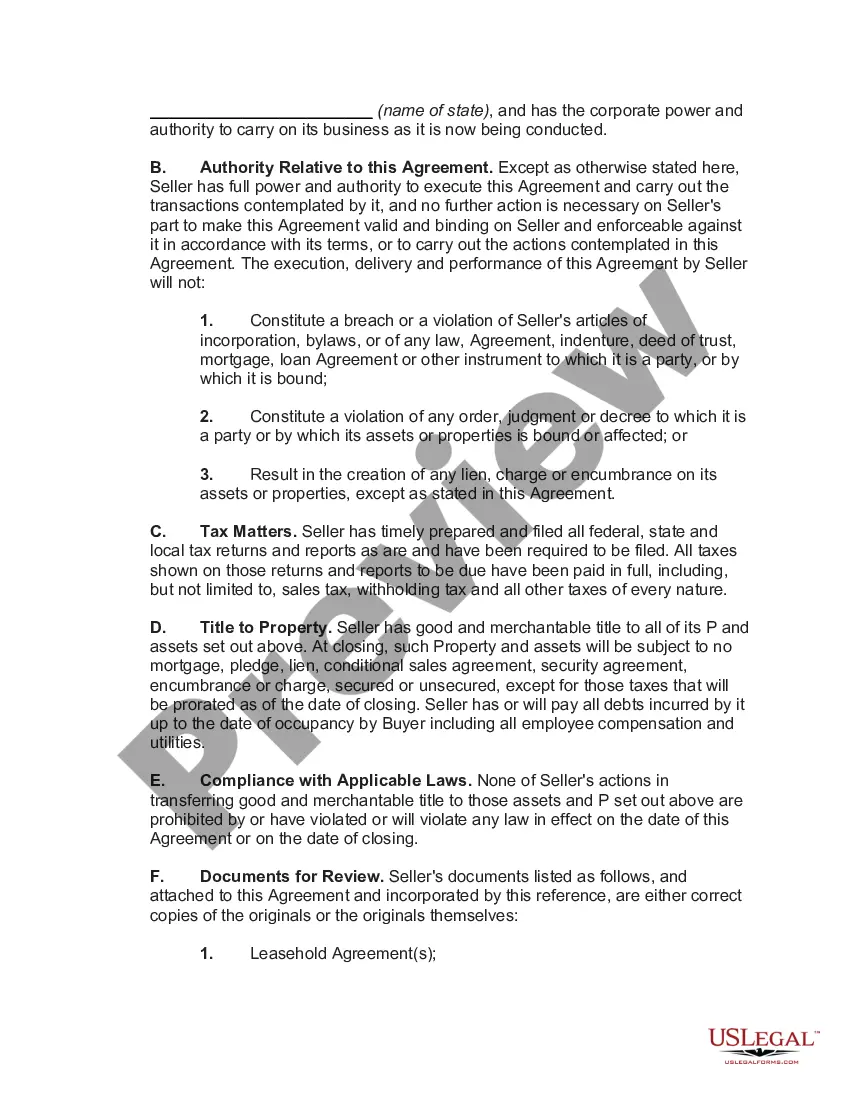

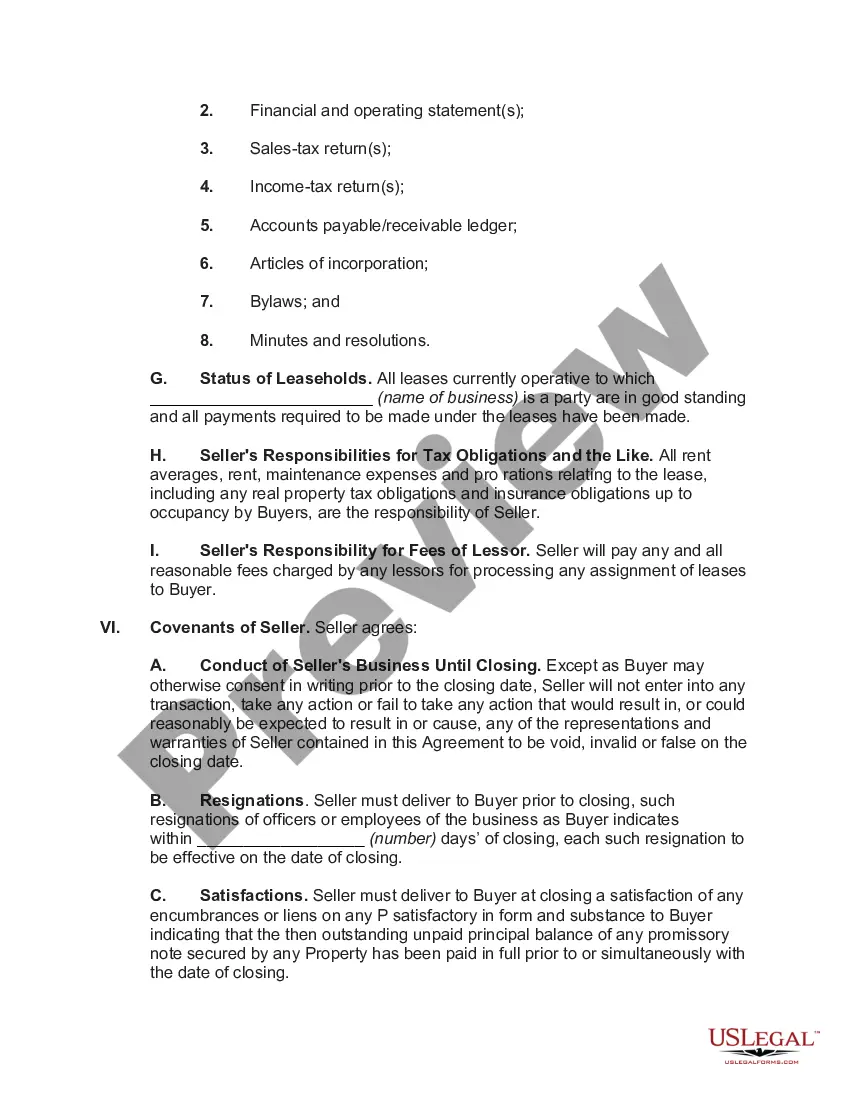

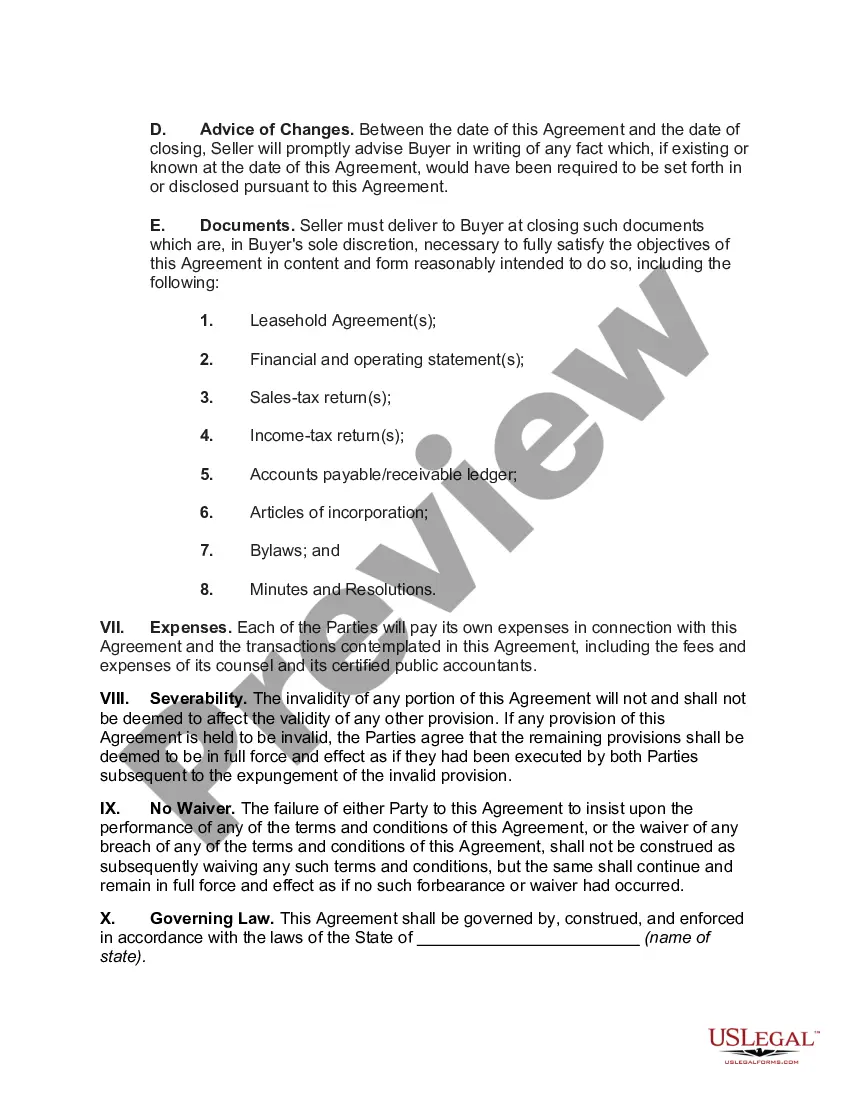

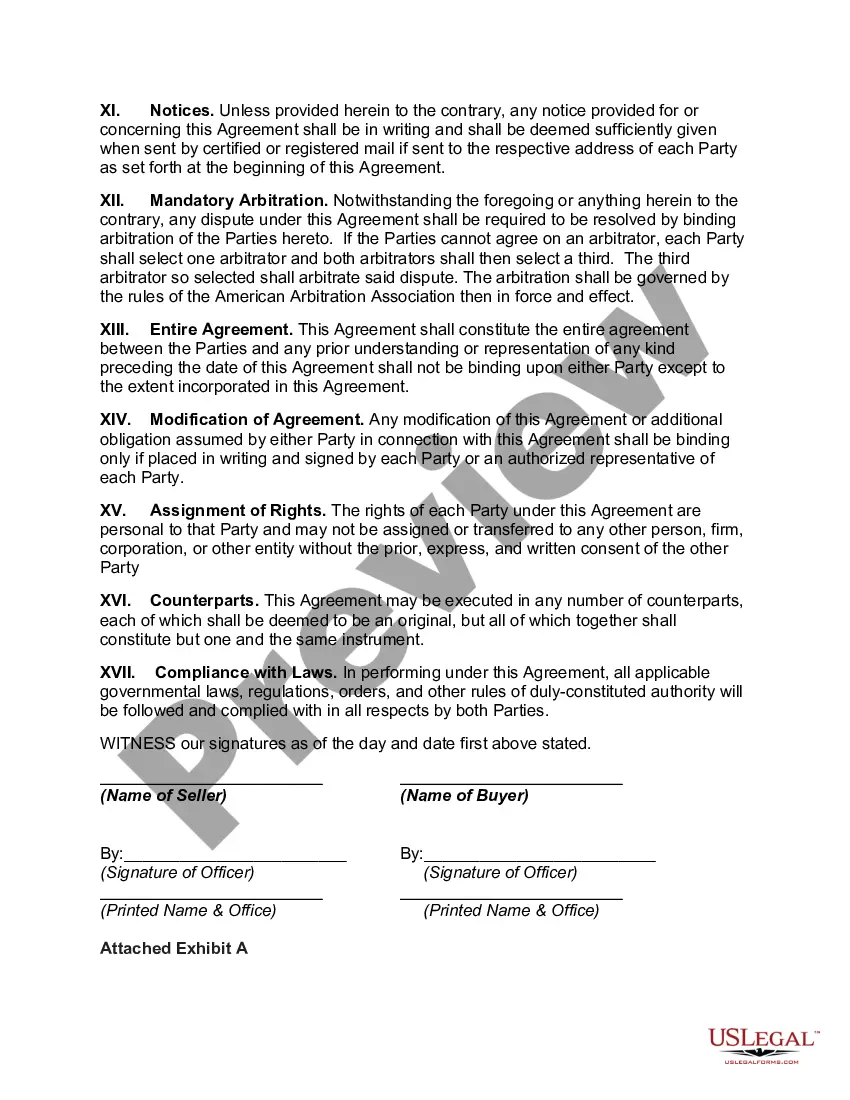

The Salt Lake Utah Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets is a legal document that outlines the terms and conditions of a sale agreement between two parties: the seller, who is a corporation, and the buyer. This agreement pertains to the sale of all assets, including both tangible and intangible business assets, of the corporation located in Salt Lake City, Utah. The agreement includes a detailed description of the assets being sold, categorizing them into two main categories: tangible and intangible assets. Tangible assets refer to physical items, such as equipment, machinery, real estate, inventory, or vehicles, while intangible assets encompass intellectual property rights, goodwill, copyrights, trademarks, or patents. The document also defines the purchase price and specifies the allocation of this price to the different categories of assets. This allocation is crucial for tax and accounting purposes and can be negotiated between the parties involved. It ensures that both tangible and intangible assets are appropriately valued and accounted for during the sale process. In addition, the agreement outlines various terms and conditions related to the sale, including representations and warranties made by both parties, payment terms, closing procedures, and any conditions or contingencies that must be met before the sale is finalized. These conditions may include regulatory approvals, consents, or any necessary third-party obligations. Depending on the specific circumstances and requirements of the corporation, there might be different types or variations of this agreement. These could include: 1. Asset Purchase Agreement with Allocation of Purchase Price: This type of agreement would be most commonly used when a buyer wants to acquire specific assets of a corporation, rather than the entire business. It would still entail the allocation of the purchase price to the different asset categories. 2. Share Purchase Agreement with Allocation of Purchase Price: In contrast to the previous type, this agreement pertains to the sale of shares of a corporation, rather than the direct assets. While the allocation of purchase price may not be as relevant, it can still be included if the buyer is interested in breaking down the value of tangible and intangible assets within the corporation. 3. Merger Agreement with Allocation of Purchase Price: This agreement would be applicable when two corporations decide to merge and consolidate their assets. The allocation of the purchase price in this case would determine the value attributed to the combined tangible and intangible assets. In conclusion, the Salt Lake Utah Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets is a comprehensive legal document that facilitates the smooth sale of a corporation's assets while appropriately allocating the purchase price. It allows for a clear understanding between the parties involved, ensures compliance with regulations, and provides a framework for a successful transaction.

Salt Lake Utah Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets

Description

How to fill out Salt Lake Utah Agreement For Sale Of All Assets Of A Corporation With Allocation Of Purchase Price To Tangible And Intangible Business Assets?

Drafting paperwork for the business or individual demands is always a big responsibility. When creating a contract, a public service request, or a power of attorney, it's important to consider all federal and state laws of the particular area. Nevertheless, small counties and even cities also have legislative provisions that you need to consider. All these aspects make it stressful and time-consuming to generate Salt Lake Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets without professional assistance.

It's possible to avoid spending money on lawyers drafting your documentation and create a legally valid Salt Lake Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets on your own, using the US Legal Forms web library. It is the greatest online catalog of state-specific legal templates that are professionally verified, so you can be certain of their validity when picking a sample for your county. Earlier subscribed users only need to log in to their accounts to download the necessary form.

If you still don't have a subscription, follow the step-by-step instruction below to obtain the Salt Lake Agreement for Sale of all Assets of a Corporation with Allocation of Purchase Price to Tangible and Intangible Business Assets:

- Examine the page you've opened and verify if it has the sample you require.

- To do so, use the form description and preview if these options are presented.

- To locate the one that meets your needs, utilize the search tab in the page header.

- Recheck that the sample complies with juridical criteria and click Buy Now.

- Choose the subscription plan, then log in or create an account with the US Legal Forms.

- Use your credit card or PayPal account to pay for your subscription.

- Download the selected file in the preferred format, print it, or fill it out electronically.

The exceptional thing about the US Legal Forms library is that all the documentation you've ever purchased never gets lost - you can access it in your profile within the My Forms tab at any time. Join the platform and easily get verified legal forms for any situation with just a couple of clicks!