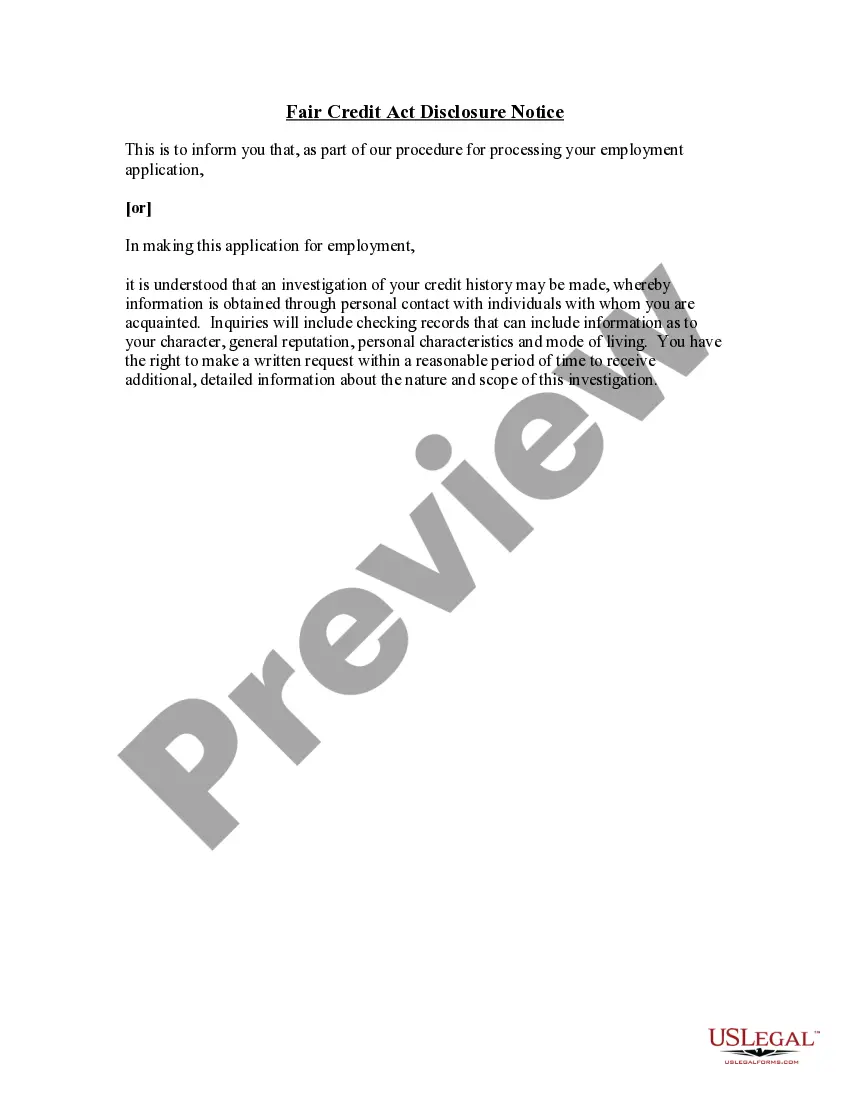

The Bronx New York Fair Credit Act Disclosure Notice is an important piece of legislation designed to protect consumers and ensure fair credit practices in the Bronx, New York. This notice provides individuals with specific rights, information, and disclosures regarding their credit and lending activities. It outlines the responsibilities of lenders, as well as the rights and protections afforded to borrowers under this act. Keywords: Bronx New York, Fair Credit Act Disclosure Notice, legislation, consumers, fair credit practices, protect, rights, information, disclosures, credit activities, lenders, borrowers, act. There are different types of Bronx New York Fair Credit Act Disclosure Notices based on specific circumstances: 1. General Disclosure Notice: This type of notice provides a broad overview of the Bronx New York Fair Credit Act and its provisions. It includes essential information about consumer rights, responsibilities of lenders, and the proper handling of credit-related matters. 2. Loan-Specific Disclosure Notice: This notice is specific to a particular loan transaction and includes pertinent details such as interest rates, repayment terms, fees, and any other loan-specific information required by the Bronx New York Fair Credit Act. It ensures that borrowers are fully informed about the terms and conditions of the loan they are entering into. 3. Dispute Resolution Disclosure Notice: This type of notice informs consumers about their rights and options when disputing credit-related issues. It outlines the steps to take if there are inaccuracies or errors in credit reports, as well as the procedures for resolving disputes with lenders or credit bureaus. 4. Credit Score Disclosure Notice: Credit scores play a vital role in loan approvals, interest rates, and overall creditworthiness. This notice provides borrowers with their credit score information and educates them on how their scores are calculated and how it impacts their borrowing opportunities. 5. Collection Practices Disclosure Notice: In cases where debt collection activities are involved, this notice informs consumers about their rights and protection against unfair or unethical debt collection practices. It outlines acceptable practices for debt collectors and provides information on reporting any unlawful activities. It is crucial for both lenders and borrowers to understand the specific details and implications of the Bronx New York Fair Credit Act Disclosure Notice applicable to their situation. By adhering to these guidelines, lenders can ensure fair credit practices, while borrowers are empowered to make informed decisions and protect their rights in credit-related matters.

Bronx New York Fair Credit Act Disclosure Notice

Description

How to fill out Bronx New York Fair Credit Act Disclosure Notice?

A document routine always goes along with any legal activity you make. Opening a company, applying or accepting a job offer, transferring ownership, and many other life situations demand you prepare official documentation that varies throughout the country. That's why having it all collected in one place is so helpful.

US Legal Forms is the biggest online collection of up-to-date federal and state-specific legal forms. On this platform, you can easily find and get a document for any individual or business objective utilized in your county, including the Bronx Fair Credit Act Disclosure Notice.

Locating forms on the platform is amazingly straightforward. If you already have a subscription to our service, log in to your account, find the sample through the search bar, and click Download to save it on your device. Afterward, the Bronx Fair Credit Act Disclosure Notice will be accessible for further use in the My Forms tab of your profile.

If you are using US Legal Forms for the first time, follow this quick guideline to obtain the Bronx Fair Credit Act Disclosure Notice:

- Ensure you have opened the right page with your localised form.

- Use the Preview mode (if available) and browse through the sample.

- Read the description (if any) to ensure the form meets your requirements.

- Search for another document using the search option in case the sample doesn't fit you.

- Click Buy Now when you find the necessary template.

- Decide on the suitable subscription plan, then log in or register for an account.

- Choose the preferred payment method (with credit card or PayPal) to continue.

- Opt for file format and download the Bronx Fair Credit Act Disclosure Notice on your device.

- Use it as needed: print it or fill it out electronically, sign it, and send where requested.

This is the easiest and most trustworthy way to obtain legal paperwork. All the samples provided by our library are professionally drafted and verified for correspondence to local laws and regulations. Prepare your paperwork and manage your legal affairs efficiently with the US Legal Forms!

Form popularity

FAQ

The Act (Title VI of the Consumer Credit Protection Act) protects information collected by consumer reporting agencies such as credit bureaus, medical information companies and tenant screening services. Information in a consumer report cannot be provided to anyone who does not have a purpose specified in the Act.

Under the Fair Credit Reporting Act, you have a right to: Access to Your Credit Report The act requires credit reporting agencies to provide you with any information in your credit file upon request once a year. You must have proper identification.

The FCRA gives you the right to be told if information in your credit file is used against you to deny your application for credit, employment or insurance. The FCRA also gives you the right to request and access all the information a consumer reporting agency has about you (this is called "file disclosure").

Disclosures to consumers. (a) Every consumer reporting agency shall, upon request and proper identification of any consumer, clearly and accurately disclose to the consumer: (1) The nature and substance of all information (except medical information) in its files on the consumer at the time of the request.

Under the FCRA, consumer reporting agencies are required to provide consumers with the information in their own file upon request, and consumer reporting agencies are not allowed to share information with third parties unless there is a permissible purpose.

The FCRA allows an employer to make a one-time disclosure and receive written permission covering any consumer report obtained in the employment application process and during the individual's employment (Haynes-James, (F.T.C. Aug.

The FCRA allows an employer to make a one-time disclosure and receive written permission covering any consumer report obtained in the employment application process and during the individual's employment (Haynes-James, (F.T.C.

The Dodd-Frank Act also amended two provisions of the FCRA to require the disclosure of a credit score and related information when a credit score is used in taking an adverse action or in risk-based pricing.

The Fair Credit Reporting Act describes the kind of data that the bureaus are allowed to collect. That includes the person's bill payment history, past loans, and current debts.

Notice to Home Loan Applicant In short, this is a disclosures that includes things like the credit score of the applicant, the range of possible scores, key factors that adversely affected the credit score, the date of the score, and the name of the person or entity that provided the score.

Interesting Questions

More info

Judiciary Committee. House of Representatives. 97th Congress. Washington, DC, July 29, 1999. The Honorable Thomas E. Cochran, Jr., Vice-Chairman, Committee on the Judiciary. Mr. Chairman: Thank you for the opportunity to discuss the Consumer Protection and Affordable Care Act of 1999. I think it is important to make the distinction in the proceedings between the act and the mandate that has been introduced to provide the funds for implementation. The act requires that states develop and administer a cost- effective alternative to the Health Insurance Portability and Accountability Act (HIPAA). As with the mandate which is an order, it states that the Secretary is also authorized to impose the requirements of the act. The first order of business is to determine whether the Act can be implemented and that is what the committee is reviewing. It is important that this be discussed and that this be the first order of business.

Disclaimer

The materials in this section are taken from public sources. We disclaim all representations or any warranties, express or implied, as to the accuracy, authenticity, reliability, accessibility, adequacy, or completeness of any data in this paragraph. Nevertheless, we make every effort to cite public sources deemed reliable and trustworthy.