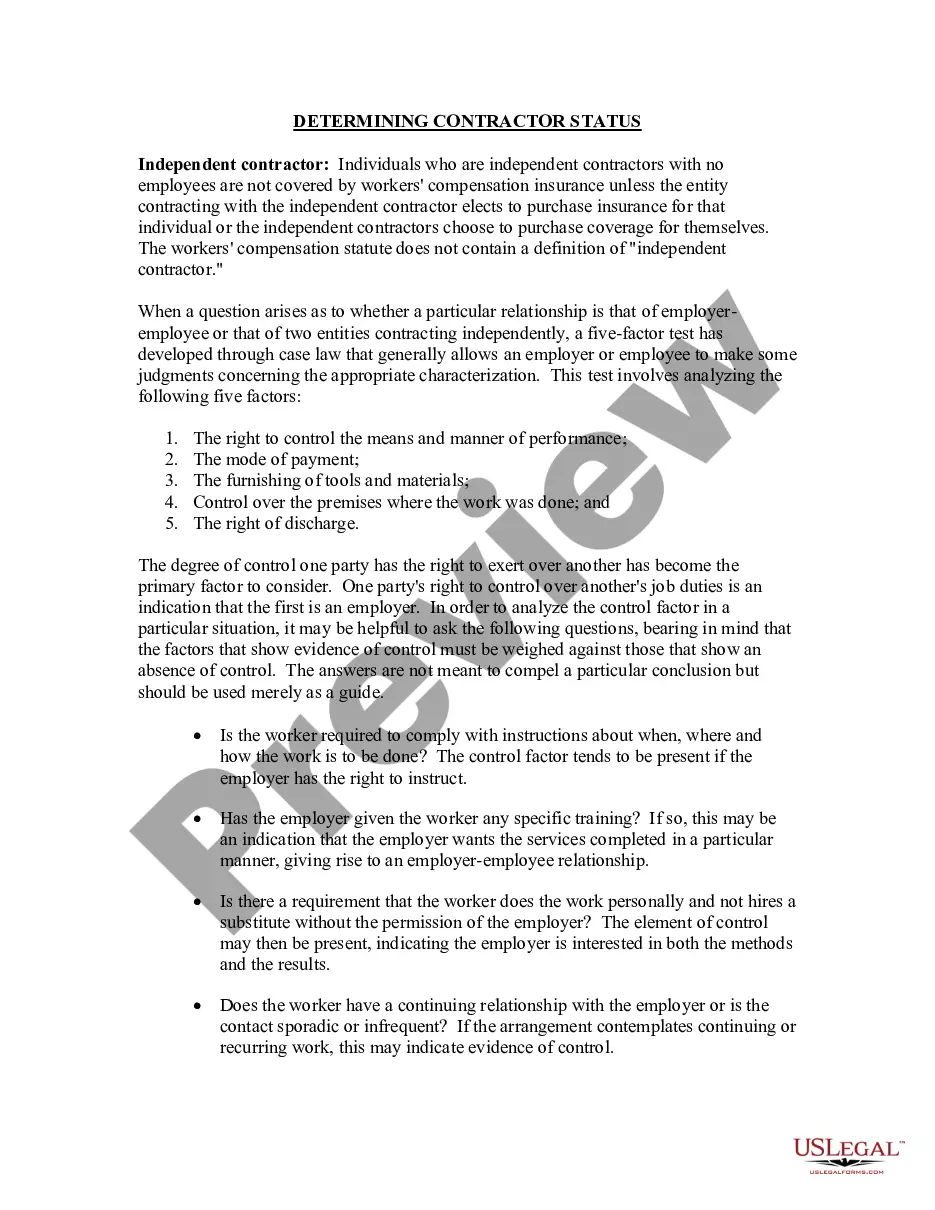

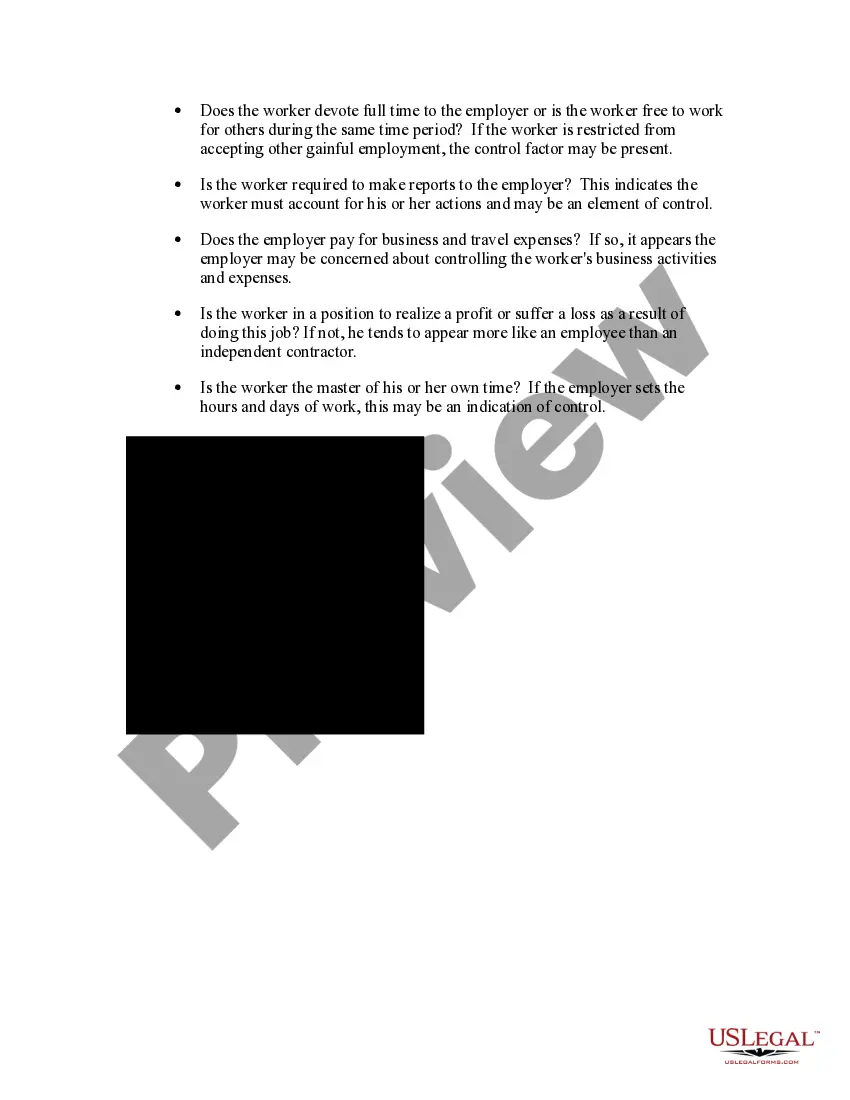

Contra Costa County, California: Determining Self-Employed Contractor Status Determining whether a worker is an employee or a self-employed contractor is crucial for both employers and workers in Contra Costa County, California. This distinction holds significant implications for taxation, workers' rights, and legal responsibilities. The Internal Revenue Service (IRS) and the Employment Development Department (EDD) provide guidelines to help determine the employment status of individuals. In Contra Costa County, California, determining the status of a self-employed contractor involves considering various factors. These factors include the level of control and independence the worker has over their work, the degree of integration into the employer's business, and the worker's opportunity for profit or loss. By examining these factors, employers can establish whether a worker is an employee or an independent contractor. To guide employers and individuals in properly classifying workers, the IRS has established three main categories: common-law employees, statutory employees, and independent contractors. 1. Common-Law Employees: Common-law employees are individuals who perform services for an employer under the employer's direction and control. The employer provides tools, training, and sets specific work hours. These employees have their taxes withheld by their employer, receive employee benefits, and may be subject to various labor laws. 2. Statutory Employees: Statutory employees are a specific type of worker who may be treated as both an employee and an independent contractor under certain circumstances. They usually fall into four categories: drivers, agent-drivers, life insurance salespeople, and home workers. Statutory employees receive a Form W-2 from their employer on which their wages, taxes, and other withholding are reported. 3. Independent Contractors: Independent contractors are self-employed individuals who generally have a significant degree of control over their work and operate as separate businesses. They are responsible for paying their own taxes, are not eligible for employee benefits, and have the flexibility to work for multiple clients. Independent contractors receive Form 1099 from their clients, which reports their earnings at the end of each tax year. It's essential for individuals and employers in Contra Costa County, California, to properly determine the worker's employment status to avoid potential misclassification issues. Misclassifying an employee as a contractor or vice versa can lead to legal and financial consequences. Both parties should familiarize themselves with the guidelines set out by the IRS and consult legal professionals if needed to ensure compliance with employment laws and regulations. Remember, accurately determining the employment status of workers in Contra Costa County, California, is fundamental to establish fair working relationships, protect workers' rights, and comply with tax regulations.

Contra Costa California Determining Self-Employed Contractor Status

Description

How to fill out Contra Costa California Determining Self-Employed Contractor Status?

How much time does it usually take you to draw up a legal document? Given that every state has its laws and regulations for every life scenario, locating a Contra Costa Determining Self-Employed Contractor Status meeting all local requirements can be tiring, and ordering it from a professional lawyer is often costly. Many online services offer the most popular state-specific templates for download, but using the US Legal Forms library is most advantegeous.

US Legal Forms is the most comprehensive online collection of templates, gathered by states and areas of use. Apart from the Contra Costa Determining Self-Employed Contractor Status, here you can get any specific form to run your business or individual affairs, complying with your county requirements. Experts verify all samples for their actuality, so you can be certain to prepare your documentation correctly.

Using the service is remarkably easy. If you already have an account on the platform and your subscription is valid, you only need to log in, choose the required form, and download it. You can pick the file in your profile at any moment later on. Otherwise, if you are new to the website, there will be some extra actions to complete before you get your Contra Costa Determining Self-Employed Contractor Status:

- Examine the content of the page you’re on.

- Read the description of the template or Preview it (if available).

- Look for another form utilizing the corresponding option in the header.

- Click Buy Now once you’re certain in the chosen file.

- Select the subscription plan that suits you most.

- Create an account on the platform or log in to proceed to payment options.

- Make a payment via PalPal or with your credit card.

- Change the file format if necessary.

- Click Download to save the Contra Costa Determining Self-Employed Contractor Status.

- Print the doc or use any preferred online editor to complete it electronically.

No matter how many times you need to use the purchased template, you can find all the files you’ve ever downloaded in your profile by opening the My Forms tab. Give it a try!