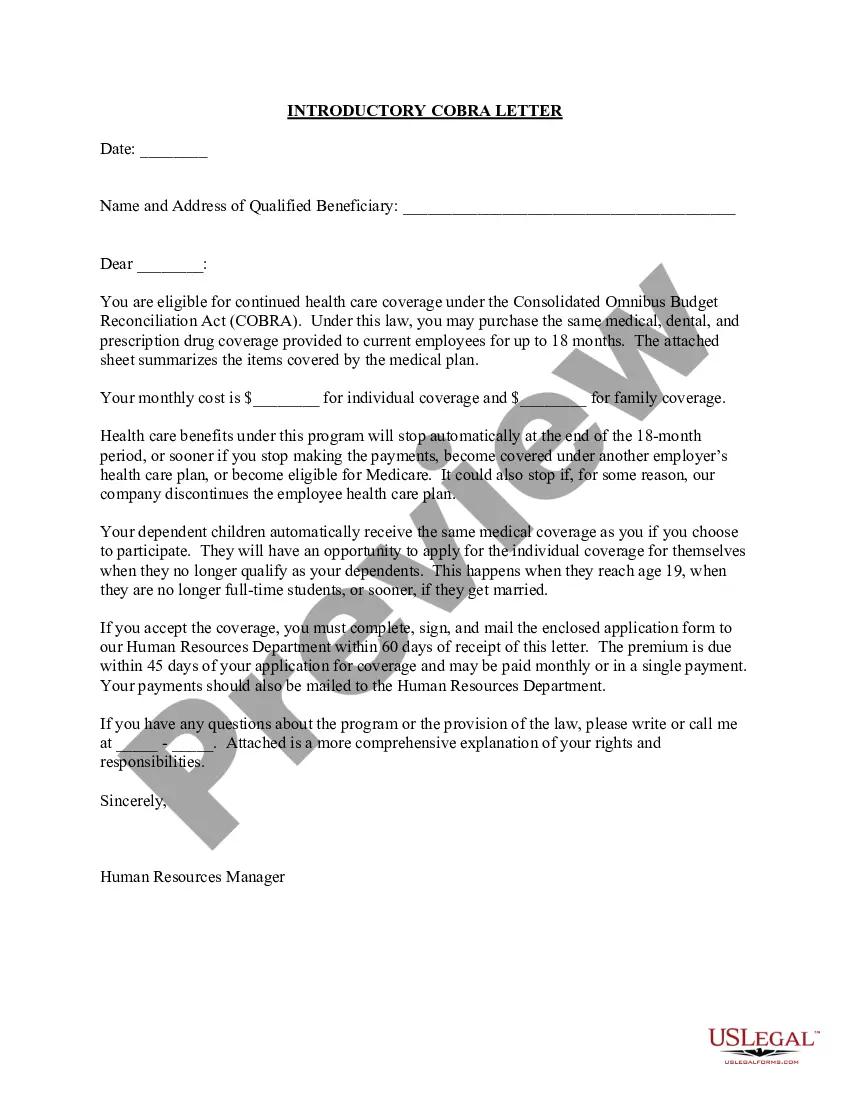

King Washington Introductory COBRA Letter is an official correspondence provided by the King Washington organization to inform eligible employees about their right to continue their health insurance coverage under the Consolidated Omnibus Budget Reconciliation Act (COBRA). This letter serves as a vital communication tool to educate recipients about their rights and responsibilities and provide essential details relating to the COBRA continuation coverage option. In general, the King Washington Introductory COBRA Letter includes crucial information such as the eligibility criteria for COBRA coverage, the duration of coverage, premium cost details, and the necessary timeframes individuals need to adhere to for enrollment. It outlines the significance of maintaining health insurance coverage during transitional periods, such as when employees experience job loss, reduced work hours, or other qualifying events. This letter emphasizes the importance of promptly reviewing and understanding the information provided to avoid any gaps in health insurance coverage. It highlights the potential benefits of COBRA continuation coverage, such as access to the same healthcare providers and coverage levels as before the qualifying event. Furthermore, it explains the critical consequences of failing to elect or maintain COBRA coverage. Different types of King Washington Introductory COBRA Letters may exist, depending on the specific qualifying event triggering the need for COBRA coverage. These events can include termination of employment, reduction in work hours, divorce or legal separation, death of the covered employee, and loss of dependent status. Each type of letter will include the relevant details and instructions specific to the qualifying event it addresses. In summary, the King Washington Introductory COBRA Letter is a comprehensive communication that informs eligible individuals about their rights and options for continuing health insurance coverage under COBRA. It offers critical information, such as eligibility requirements, duration of coverage, premium costs, and enrollment timeframes. It aims to ensure individuals maintain essential healthcare coverage during transitional periods, preventing potential gaps in insurance protection.

King Washington Introductory COBRA Letter

Description

How to fill out King Washington Introductory COBRA Letter?

Preparing legal paperwork can be cumbersome. In addition, if you decide to ask an attorney to write a commercial agreement, papers for ownership transfer, pre-marital agreement, divorce paperwork, or the King Introductory COBRA Letter, it may cost you a lot of money. So what is the best way to save time and money and create legitimate forms in total compliance with your state and local laws and regulations? US Legal Forms is a great solution, whether you're searching for templates for your personal or business needs.

US Legal Forms is largest online collection of state-specific legal documents, providing users with the up-to-date and professionally verified forms for any use case collected all in one place. Therefore, if you need the current version of the King Introductory COBRA Letter, you can easily find it on our platform. Obtaining the papers requires a minimum of time. Those who already have an account should check their subscription to be valid, log in, and pick the sample using the Download button. If you haven't subscribed yet, here's how you can get the King Introductory COBRA Letter:

- Glance through the page and verify there is a sample for your region.

- Check the form description and use the Preview option, if available, to ensure it's the sample you need.

- Don't worry if the form doesn't satisfy your requirements - search for the correct one in the header.

- Click Buy Now when you find the needed sample and choose the best suitable subscription.

- Log in or sign up for an account to purchase your subscription.

- Make a transaction with a credit card or through PayPal.

- Opt for the file format for your King Introductory COBRA Letter and save it.

When finished, you can print it out and complete it on paper or upload the samples to an online editor for a faster and more practical fill-out. US Legal Forms enables you to use all the documents ever obtained many times - you can find your templates in the My Forms tab in your profile. Give it a try now!