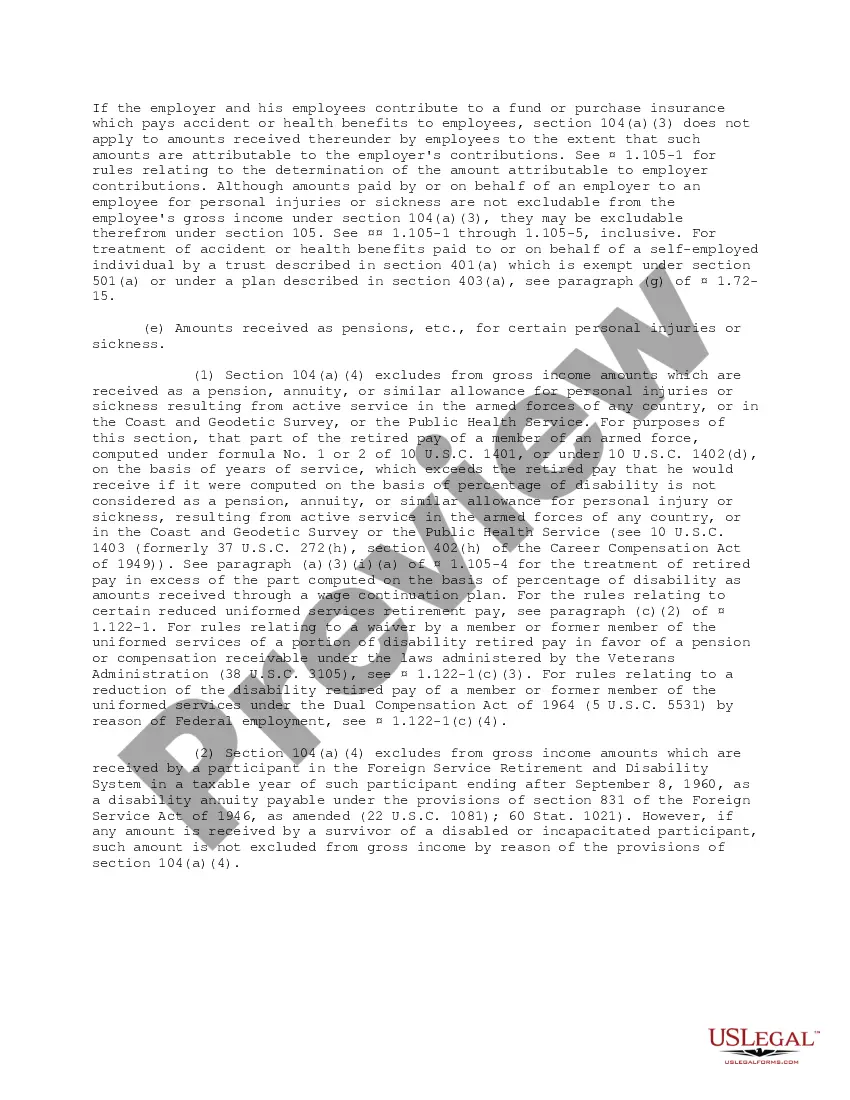

Statutory Guidelines [Appendix A(2) Tres. Reg 104-1] regarding compensation for injuries or sickness under workmen's compensation acts, damages, accident or health insurance, etc. as stated in the guidelines.

Cook Illinois Compensation for Injuries or Sickness Treasury Regulation 104.1, also known as Treasury Regulation Section 104.1, is a comprehensive set of guidelines and provisions established by the U.S. Department of the Treasury. These regulations outline the tax treatment of compensation received by individuals as a result of injuries or sickness. The primary purpose of Cook Illinois Compensation for Injuries or Sickness Treasury Regulation 104.1 is to provide clarity on the tax implications of such compensations. It influences how individuals report and file their taxes while receiving payments for injuries or illnesses. These regulations aim to ensure fair and consistent treatment in terms of taxation across various types of compensations. There are different types of Cook Illinois Compensation for Injuries or Sickness Treasury Regulation 104.1, which include: 1. Medical Expense Reimbursements: This category covers reimbursements received by individuals to cover medical expenses resulting from injuries or sickness. It outlines the tax treatment of these reimbursements and specifies what qualifies as eligible medical expenses. 2. Disability Benefits: Cook Illinois Compensation for Injuries or Sickness Treasury Regulation 104.1 also addresses disability benefits received due to injuries or sickness. It outlines the tax treatment of long-term and short-term disability benefits, including how to determine taxable and non-taxable portions of such payments. 3. Personal Injury Settlements: This category pertains to compensatory awards or settlements received through legal actions for personal injuries. It outlines how these settlements should be reported and taxed, taking into account various factors like medical expenses, attorney fees, and other related costs. 4. Workers' Compensation: Cook Illinois Compensation for Injuries or Sickness Treasury Regulation 104.1 also covers workers' compensation benefits. It provides guidelines on the taxation of payments made to workers who suffer workplace injuries or illnesses, ensuring consistency in tax treatment across jurisdictions. 5. Sickness and Accident Insurance Benefits: This component explains the tax treatment of insurance benefits received by individuals as a result of injuries or sickness. It clarifies which portions of these benefits are taxable and which are not, helping individuals accurately report such income. Overall, Cook Illinois Compensation for Injuries or Sickness Treasury Regulation 104.1 plays a crucial role in providing individuals with clarity and guidance regarding the tax treatment of compensation received for injuries or sickness. It ensures that individuals comply with the necessary regulations while accurately reporting these payments, ultimately promoting fairness and consistency in the taxation system.