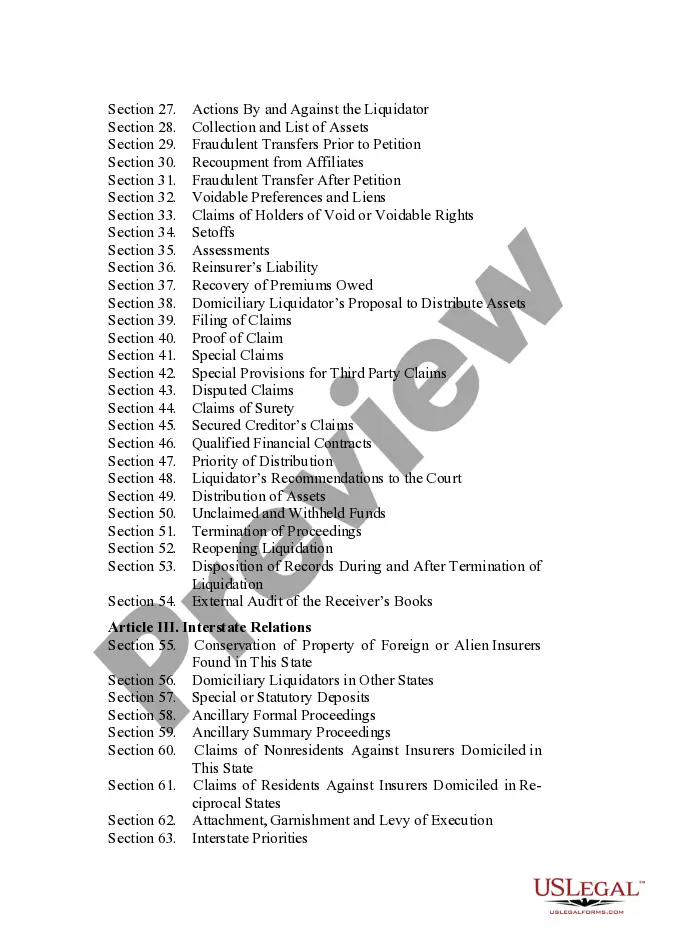

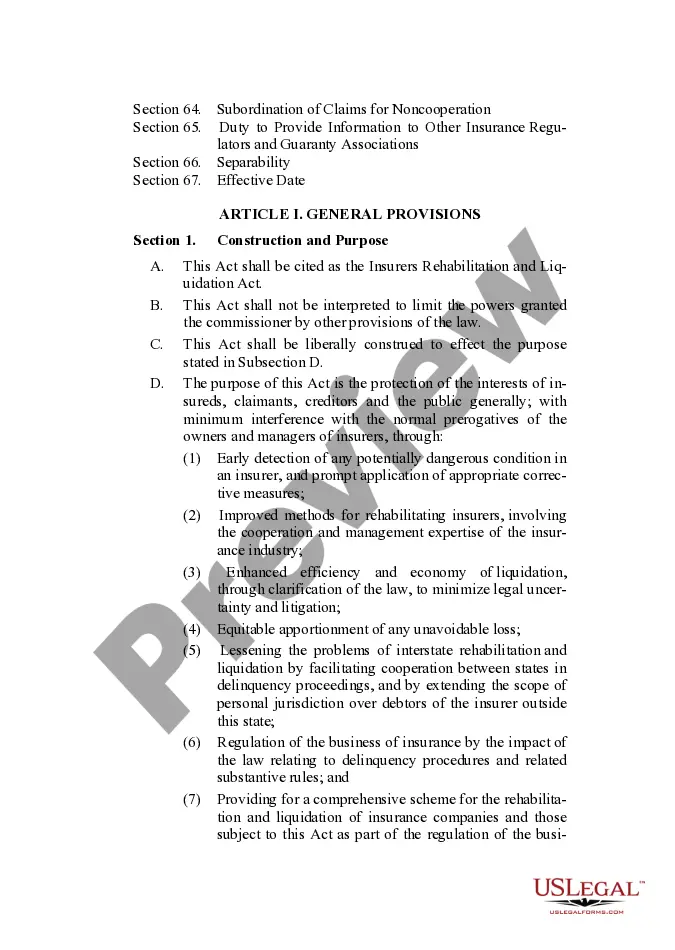

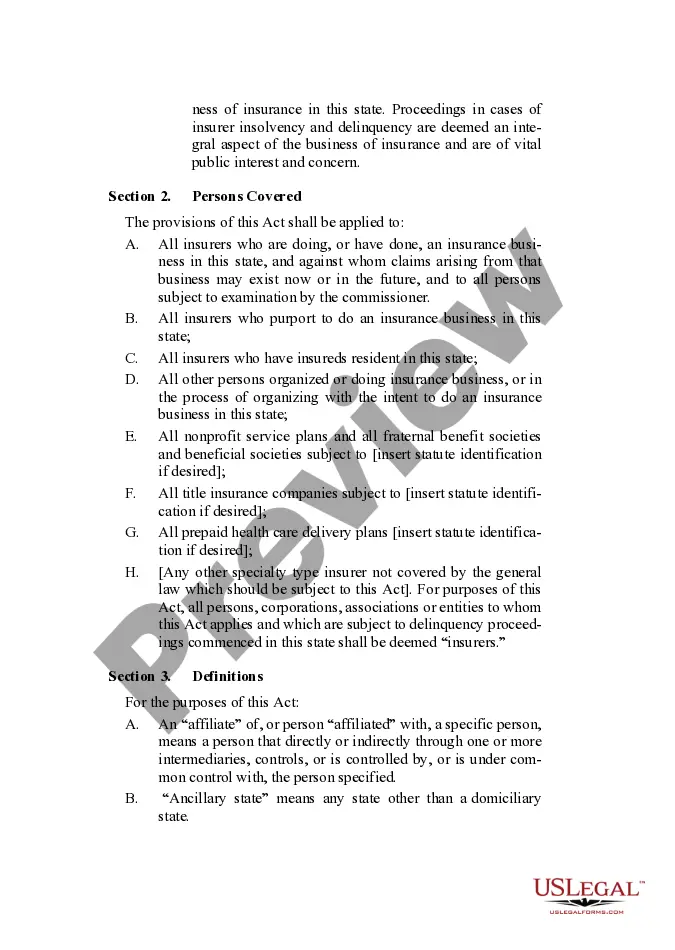

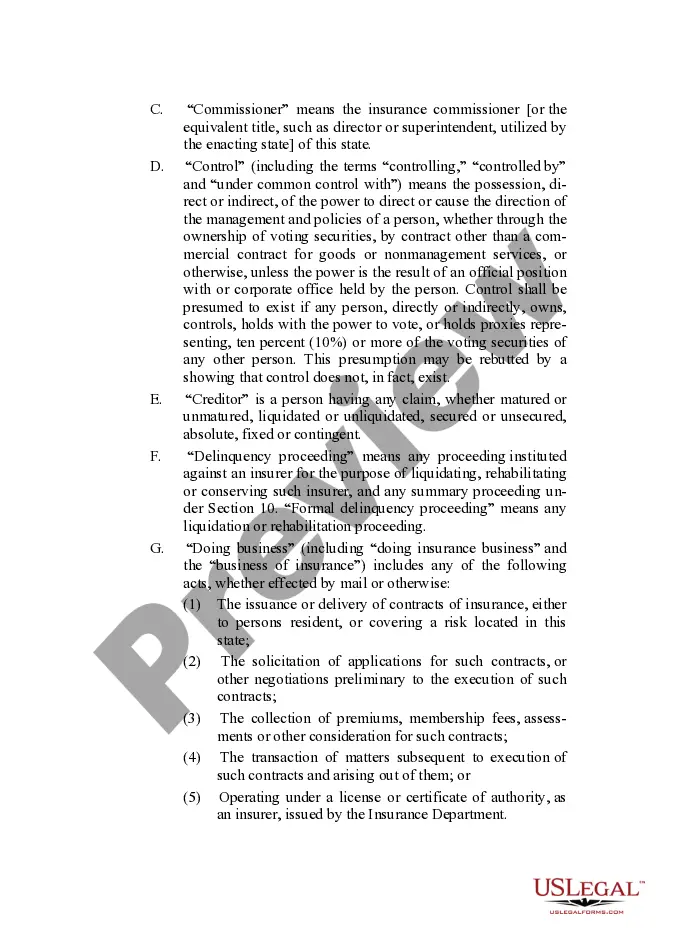

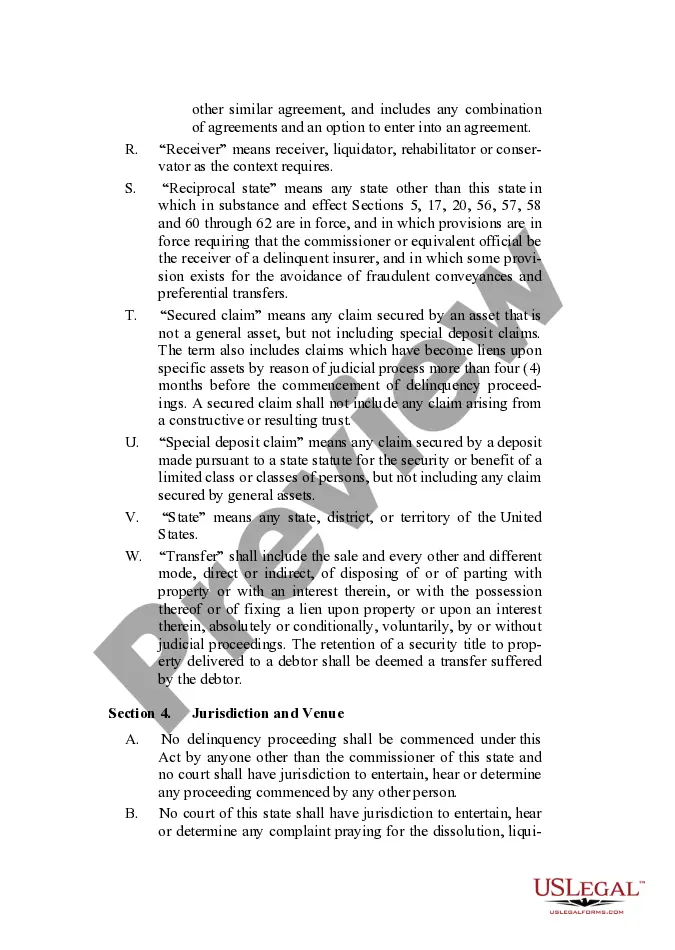

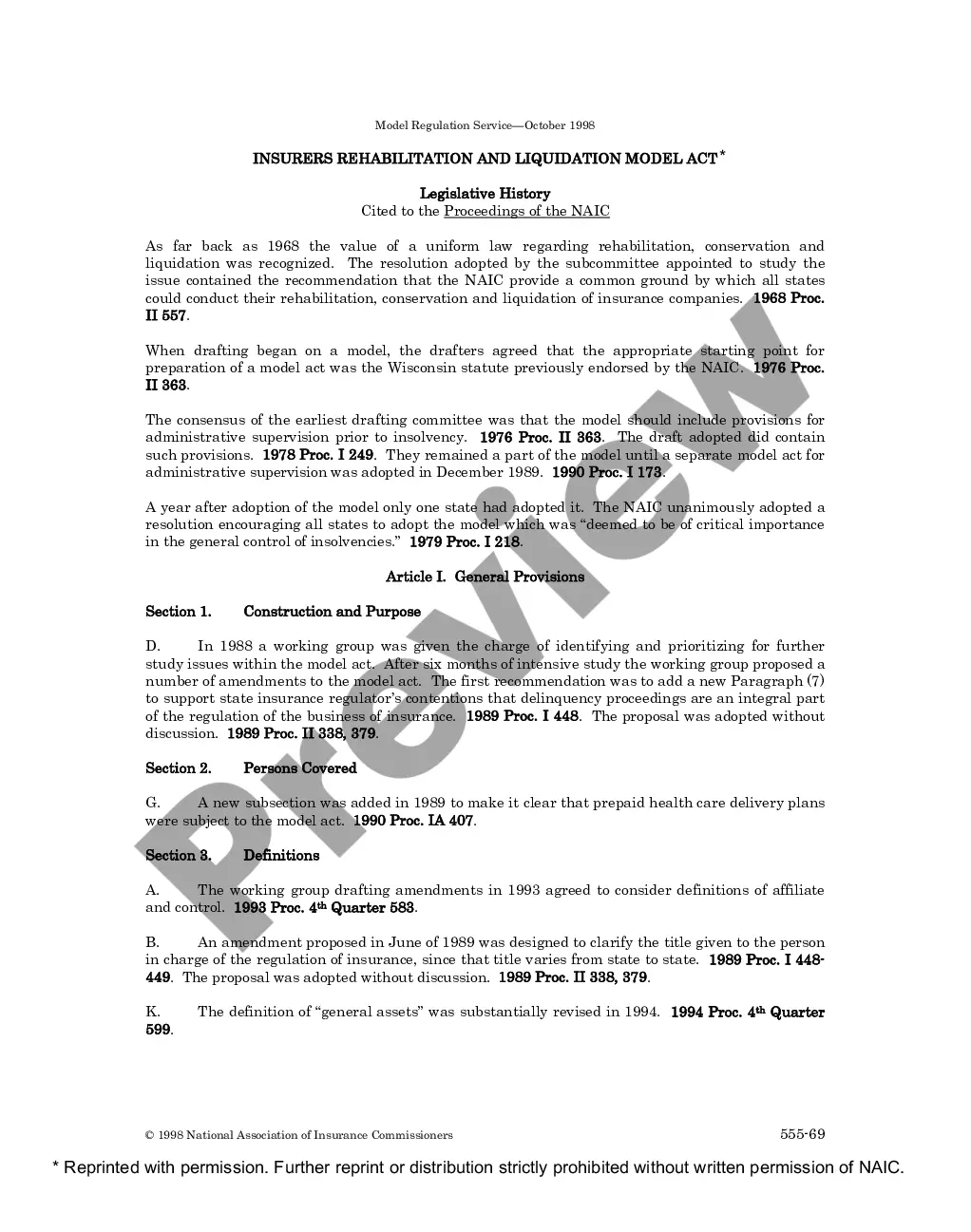

Full text and statutory guidelines for the Insurers Rehabilitation and Liquidation Model Act.

The Riverside California Insurers Rehabilitation and Liquidation Model Act is a crucial piece of legislation designed to manage the rehabilitation and liquidation processes of insurers operating in Riverside, California. This act outlines the guidelines and procedures for the efficient resolution of troubled insurers to protect policyholders, creditors, and the insurance industry as a whole. One of the primary objectives of this act is to ensure the timely and orderly rehabilitation or liquidation of insurers that are unable to meet their financial obligations. The act provides a framework for the California Department of Insurance (CDI) to intervene when an insurer faces significant financial instability or insolvency. Under this act, there are different types of rehabilitation and liquidation methods that can be employed based on the specific circumstances and severity of the insurer's financial distress. These methods include: 1. Rehabilitation: Rehabilitation aims to restore the insurer's financial viability and ensure the continuation of its operations. The CDI, as the designated rehabilitation, assumes control over the insurer's assets, liabilities, and management. The rehabilitation employs various strategies, such as restructuring debt, renegotiating contracts, and implementing cost-cutting measures, to stabilize the insurer's financial position. 2. Conservation: Conservation refers to an alternative form of rehabilitation, focusing on the conservation and preservation of the insurer's assets. The CDI acts as the conservator and takes control of the insurer's assets and operations to prevent further deterioration, while exploring restructuring options. Conservation is typically used when there is an immediate threat to policyholders' interests or the insurer's continued solvency. 3. Liquidation: Liquidation is the last resort when the insurer's financial situation is irreparable or rehabilitation is not feasible. The liquidation process involves the sale of the insurer's assets to pay off its outstanding debts, including policyholder claims. The CDI, as the liquidator, manages the orderly distribution of assets and the resolution of outstanding obligations. The Riverside California Insurers Rehabilitation and Liquidation Model Act incorporates a range of important provisions and safeguards to ensure fair treatment for policyholders, creditors, and other stakeholders in the rehabilitation and liquidation processes. It encompasses criteria for determining insolvency, procedures for notification, claim processing, supervision, and the distribution of assets. In summary, the Riverside California Insurers Rehabilitation and Liquidation Model Act is a comprehensive framework that guides the rehabilitation and liquidation of troubled insurers in Riverside, California. Its various methods, including rehabilitation, conservation, and liquidation, are implemented to protect the interests of policyholders, creditors, and the stability of the insurance market.The Riverside California Insurers Rehabilitation and Liquidation Model Act is a crucial piece of legislation designed to manage the rehabilitation and liquidation processes of insurers operating in Riverside, California. This act outlines the guidelines and procedures for the efficient resolution of troubled insurers to protect policyholders, creditors, and the insurance industry as a whole. One of the primary objectives of this act is to ensure the timely and orderly rehabilitation or liquidation of insurers that are unable to meet their financial obligations. The act provides a framework for the California Department of Insurance (CDI) to intervene when an insurer faces significant financial instability or insolvency. Under this act, there are different types of rehabilitation and liquidation methods that can be employed based on the specific circumstances and severity of the insurer's financial distress. These methods include: 1. Rehabilitation: Rehabilitation aims to restore the insurer's financial viability and ensure the continuation of its operations. The CDI, as the designated rehabilitation, assumes control over the insurer's assets, liabilities, and management. The rehabilitation employs various strategies, such as restructuring debt, renegotiating contracts, and implementing cost-cutting measures, to stabilize the insurer's financial position. 2. Conservation: Conservation refers to an alternative form of rehabilitation, focusing on the conservation and preservation of the insurer's assets. The CDI acts as the conservator and takes control of the insurer's assets and operations to prevent further deterioration, while exploring restructuring options. Conservation is typically used when there is an immediate threat to policyholders' interests or the insurer's continued solvency. 3. Liquidation: Liquidation is the last resort when the insurer's financial situation is irreparable or rehabilitation is not feasible. The liquidation process involves the sale of the insurer's assets to pay off its outstanding debts, including policyholder claims. The CDI, as the liquidator, manages the orderly distribution of assets and the resolution of outstanding obligations. The Riverside California Insurers Rehabilitation and Liquidation Model Act incorporates a range of important provisions and safeguards to ensure fair treatment for policyholders, creditors, and other stakeholders in the rehabilitation and liquidation processes. It encompasses criteria for determining insolvency, procedures for notification, claim processing, supervision, and the distribution of assets. In summary, the Riverside California Insurers Rehabilitation and Liquidation Model Act is a comprehensive framework that guides the rehabilitation and liquidation of troubled insurers in Riverside, California. Its various methods, including rehabilitation, conservation, and liquidation, are implemented to protect the interests of policyholders, creditors, and the stability of the insurance market.