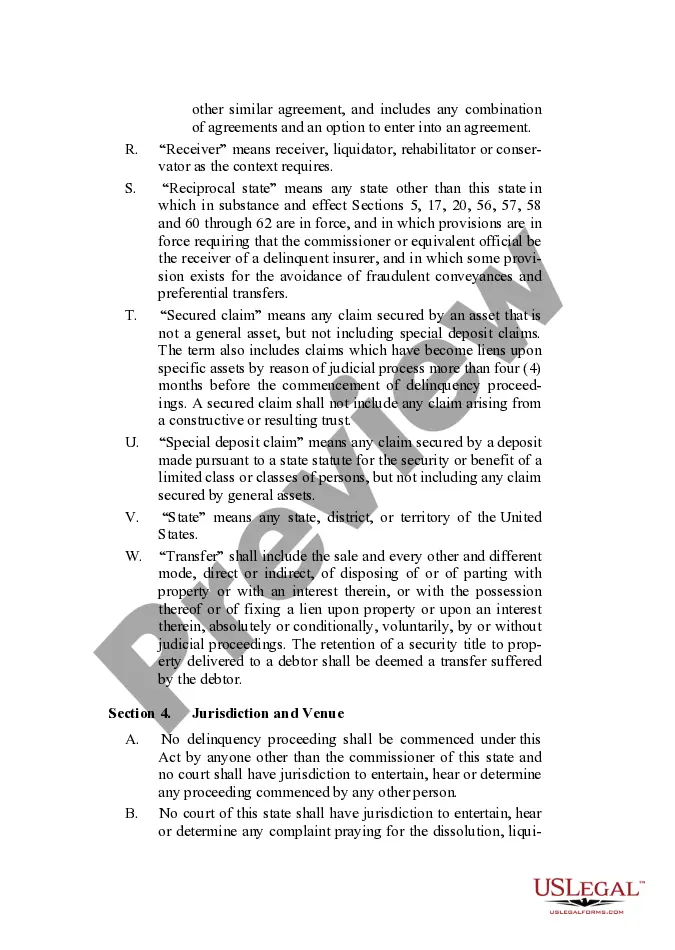

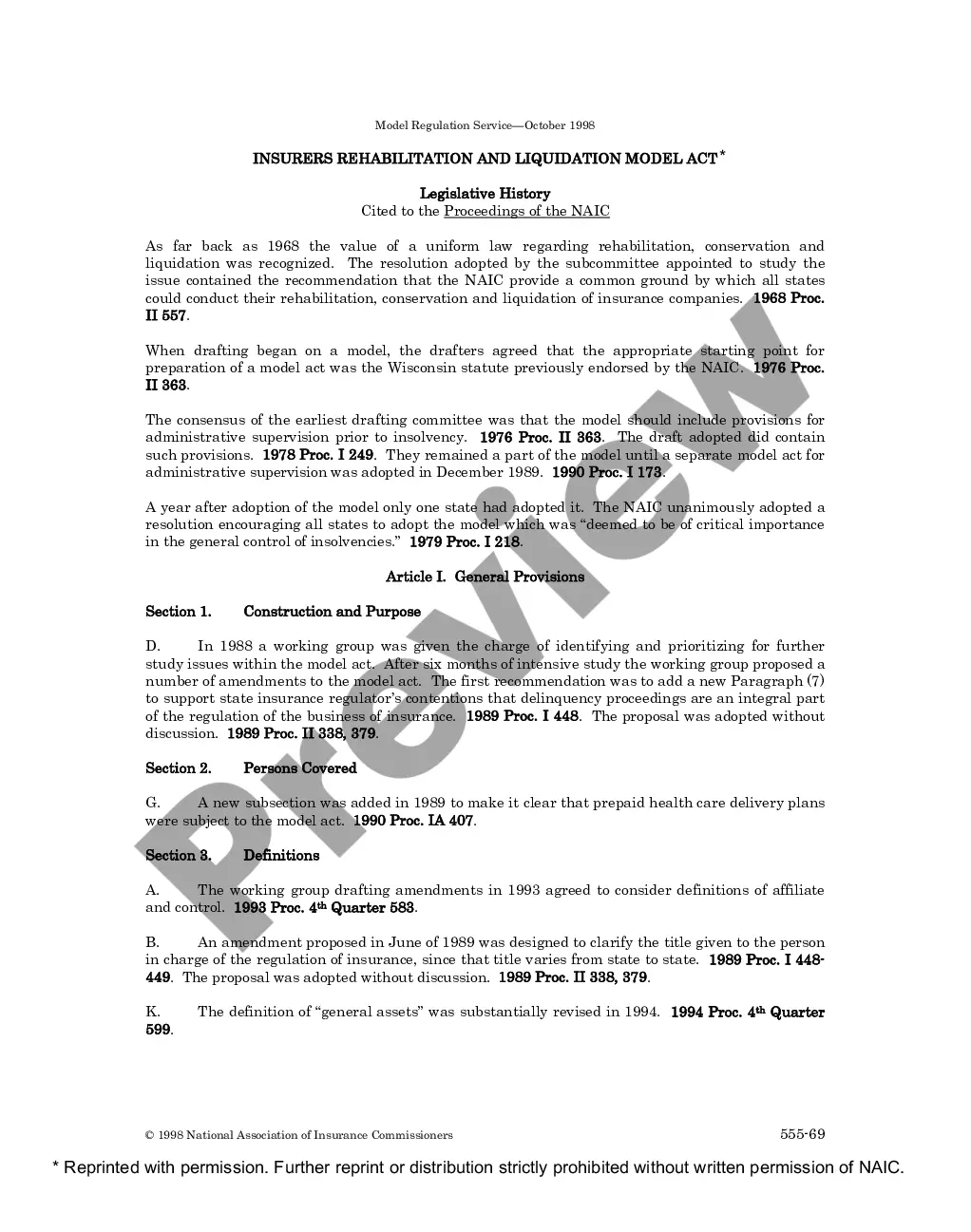

Full text and statutory guidelines for the Insurers Rehabilitation and Liquidation Model Act.

The Wake North Carolina Insurers Rehabilitation and Liquidation Model Act is a comprehensive framework established by the state of North Carolina to manage the rehabilitation and liquidation process for insurers. This act outlines the legal procedures and guidelines to be followed when an insurance company encounters financial distress, ensuring effective addressing of the situation while protecting the interests of policyholders and creditors. Key features of the Wake North Carolina Insurers Rehabilitation and Liquidation Model Act include financial oversight, asset evaluation, claims handling, and supervision of troubled insurers. Under this model, appointed state officials or an insurance commissioner take charge of the troubled insurance company's affairs, including its assets, liabilities, and policies. The act differentiates between rehabilitation and liquidation, offering discrete processes based on the company's financial viability. Rehabilitation aims to revive the company's financial health by restructuring its operations, reducing expenses, and negotiating with creditors. On the other hand, liquidation occurs when rehabilitation is deemed impossible, requiring the orderly closure of the insurance company's operations. The model act ensures that beneficiaries of insurance policies, along with creditors, are prioritized and protected during this process. It establishes a claims' resolution mechanism, allowing affected policyholders to submit claims and receive their entitled benefits. The act also includes provisions for monitoring the rehabilitation or liquidation progress and handling complaints or disputes that may arise during the process. The Wake North Carolina Insurers Rehabilitation and Liquidation Model Act may involve variations tailored to specific types of insurance companies. For instance, there might be separate provisions for life insurance, health insurance, property and casualty insurance, and other specialized insurance sectors. These variations account for the unique characteristics and regulatory requirements associated with each type of insurer, ensuring the act remains relevant and effective across the entire insurance industry. Overall, the Wake North Carolina Insurers Rehabilitation and Liquidation Model Act serves as a comprehensive legal framework that safeguards the interests of policyholders, creditors, and the insurance industry as a whole. Its meticulous guidelines and procedures provide a structured approach for managing distressed insurers while aiming to achieve the best possible outcomes for all stakeholders involved.