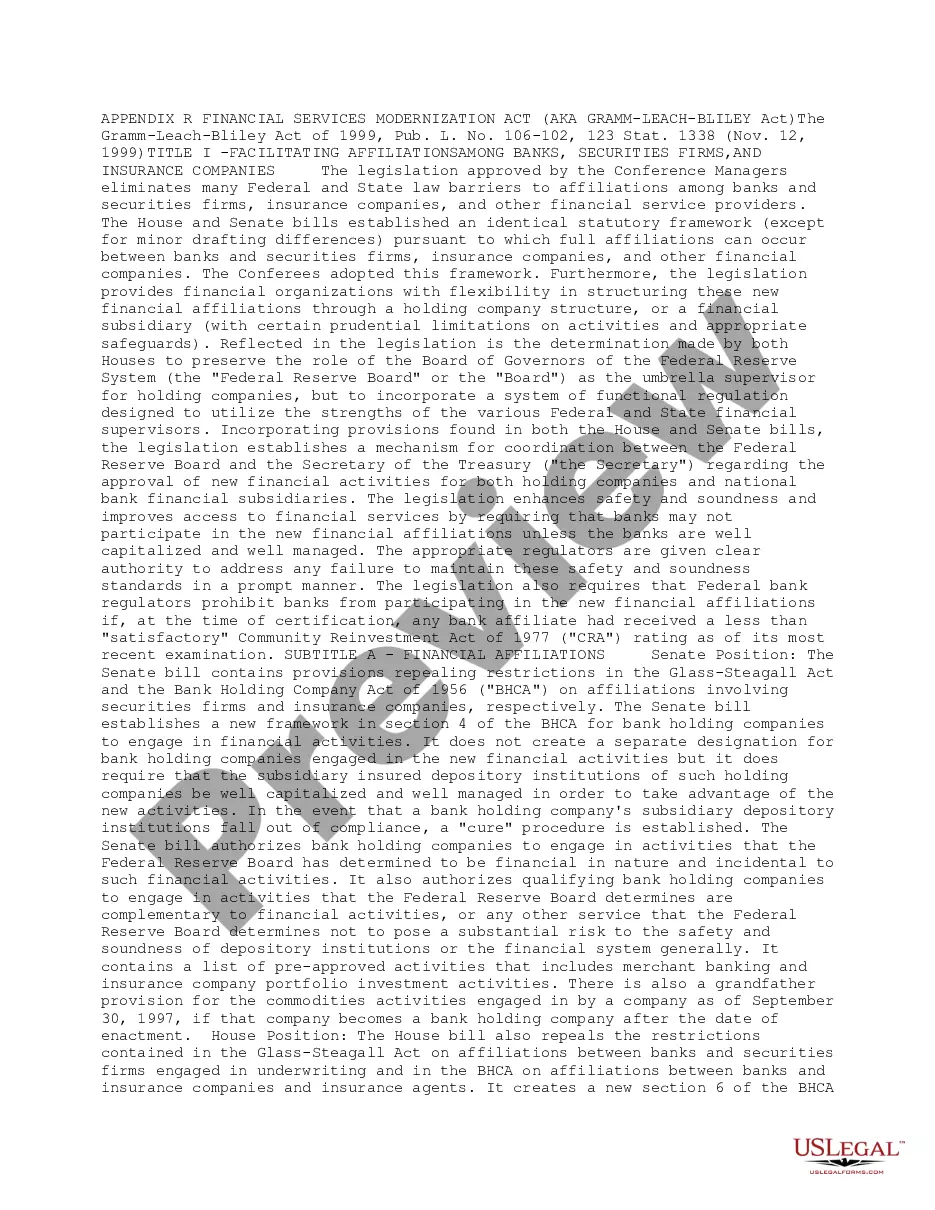

Full text and statutory guidelines for the Financial Services Modernization Act (Gramm-Leach-Bliley Act)

The Chicago Illinois Financial Services Modernization Act, also known as the Gramm-Leach-Bliley Act, is a significant piece of legislation enacted in 1999 that aimed to modernize and regulate the financial services industry. This act has shaped the landscape of financial services by removing many barriers that previously separated commercial banks, investment banks, and insurance companies. The Gramm-Leach-Bliley Act (ALBA) plays a crucial role in promoting competition, consumer protection, and information privacy within the financial sector. This act recognizes the evolving needs of the market and strives to create a more efficient and secure financial system. One of the key aspects of ALBA is the elimination of the Glass-Steagall Act's restrictions. The Glass-Steagall Act, enacted during the Great Depression, separated commercial and investment banking activities, aiming to prevent conflicts of interest. Under the ALBA, banks are allowed to provide a wider range of financial services, including insurance and securities activities, as long as they adhere to certain regulatory measures. The ALBA fosters competition by allowing financial institutions to diversify their services, attracting customers with a comprehensive range of offerings. This results in improved access to financial products and services for consumers. However, this act also seeks to protect consumers by setting regulations and standards that financial institutions must follow. Data privacy is a significant concern in the modern era, and the ALBA addresses this issue by setting guidelines for the protection of consumers' non-public personal information (NPI). Financial institutions are obligated to inform customers about their privacy policies and provide opt-out options for the sharing of NPI with non-affiliated third parties. This helps to ensure that consumers have control over their personal information and are aware of how it is being utilized. In addition to the main provisions mentioned above, there may not be different types of the Chicago Illinois Financial Services Modernization Act (Gramm-Leach-Bliley Act). However, it is important to note that the act may be subject to periodic amendments and updates to adapt to the changing dynamics of the financial industry. Overall, the Chicago Illinois Financial Services Modernization Act (Gramm-Leach-Bliley Act) is a comprehensive legislation that promotes competition, consumer protection, and data privacy within the financial services industry. By breaking down barriers and encouraging innovation, this act has had a lasting impact on the way financial services are provided and regulated in the United States.The Chicago Illinois Financial Services Modernization Act, also known as the Gramm-Leach-Bliley Act, is a significant piece of legislation enacted in 1999 that aimed to modernize and regulate the financial services industry. This act has shaped the landscape of financial services by removing many barriers that previously separated commercial banks, investment banks, and insurance companies. The Gramm-Leach-Bliley Act (ALBA) plays a crucial role in promoting competition, consumer protection, and information privacy within the financial sector. This act recognizes the evolving needs of the market and strives to create a more efficient and secure financial system. One of the key aspects of ALBA is the elimination of the Glass-Steagall Act's restrictions. The Glass-Steagall Act, enacted during the Great Depression, separated commercial and investment banking activities, aiming to prevent conflicts of interest. Under the ALBA, banks are allowed to provide a wider range of financial services, including insurance and securities activities, as long as they adhere to certain regulatory measures. The ALBA fosters competition by allowing financial institutions to diversify their services, attracting customers with a comprehensive range of offerings. This results in improved access to financial products and services for consumers. However, this act also seeks to protect consumers by setting regulations and standards that financial institutions must follow. Data privacy is a significant concern in the modern era, and the ALBA addresses this issue by setting guidelines for the protection of consumers' non-public personal information (NPI). Financial institutions are obligated to inform customers about their privacy policies and provide opt-out options for the sharing of NPI with non-affiliated third parties. This helps to ensure that consumers have control over their personal information and are aware of how it is being utilized. In addition to the main provisions mentioned above, there may not be different types of the Chicago Illinois Financial Services Modernization Act (Gramm-Leach-Bliley Act). However, it is important to note that the act may be subject to periodic amendments and updates to adapt to the changing dynamics of the financial industry. Overall, the Chicago Illinois Financial Services Modernization Act (Gramm-Leach-Bliley Act) is a comprehensive legislation that promotes competition, consumer protection, and data privacy within the financial services industry. By breaking down barriers and encouraging innovation, this act has had a lasting impact on the way financial services are provided and regulated in the United States.