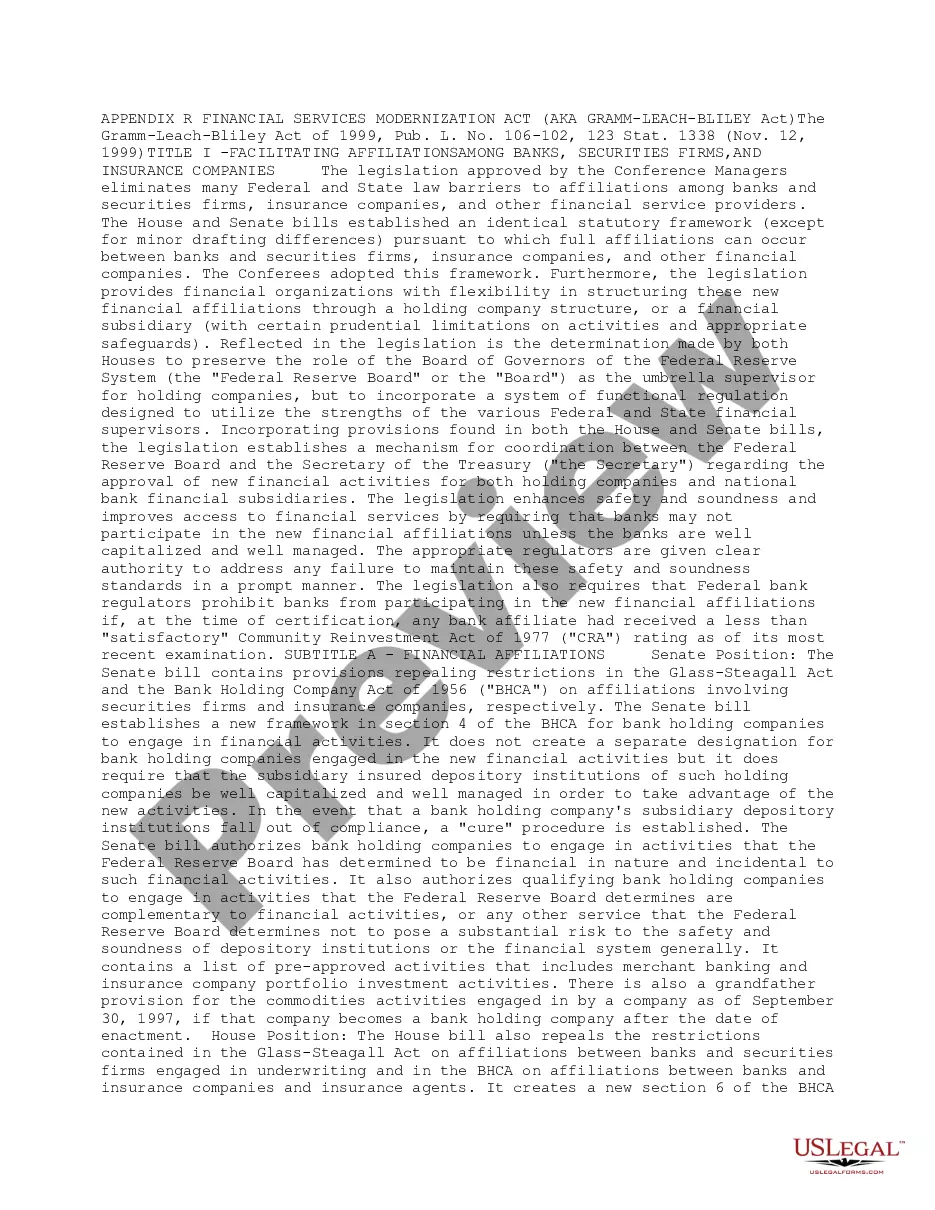

Full text and statutory guidelines for the Financial Services Modernization Act (Gramm-Leach-Bliley Act)

The King Washington Financial Services Modernization Act, also known as the Gramm-Leach-Bliley Act (ALBA), is a significant piece of legislation that was enacted in the United States to address the rapidly evolving financial services industry. This act aimed to remove barriers between different types of financial institutions, such as banks, insurance companies, and investment firms, allowing them to engage in a broader range of financial activities while protecting consumer privacy. The Gramm-Leach-Bliley Act encompasses various provisions and regulations, each serving specific purposes to promote competition, consumer protection, and privacy in the financial services sector. Some key elements and keywords associated with this act include: 1. Financial Institutions: ALBA allows different types of financial institutions, including commercial banks, investment companies, insurance companies, and securities firms to enter into new business activities, collaborate, and form affiliate relationships. 2. Financial Services Modernization: The act aimed to modernize the financial industry by removing certain restrictions on the activities of financial institutions, facilitating mergers and acquisitions, and promoting technological advancements in financial services. 3. Consumer Privacy: One critical component of ALBA is the requirement for financial institutions to protect consumers' personal information. It introduced regulations for the collection, disclosure, and storing of consumers' non-public personal information, ensuring the privacy and security of customer data. 4. Financial Privacy Rule: This rule under ALBA mandates financial institutions to provide an annual notice to customers regarding the institution's privacy policies and practices. Additionally, it allows consumers to opt-out of sharing their personal information with non-affiliated third parties. 5. Safeguards Rule: The Safeguards Rule under ALBA imposes requirements on financial institutions to develop and implement comprehensive information security programs. These programs must include measures to protect customer information from unauthorized access, data breaches, and other security threats. 6. Pretexting: The ALBA includes provisions aimed at preventing pretexting, which is the act of using false pretenses to obtain a person's personal financial information. These provisions impose penalties on individuals or companies engaged in such deceptive practices. It is important to note that the King Washington Financial Services Modernization Act is often referred to as the Gramm-Leach-Bliley Act due its co-sponsorship by three U.S. lawmakers: Senator Phil Grammy, Representative Jim Leach, and Representative Thomas J. Bailey Jr. The act has had a significant impact on the financial services industry, promoting competition and innovation while ensuring consumer protection and privacy. Understanding the various provisions and regulations of ALBA is crucial for financial institutions and individuals alike to navigate the ever-changing landscape of the modern financial services sector.