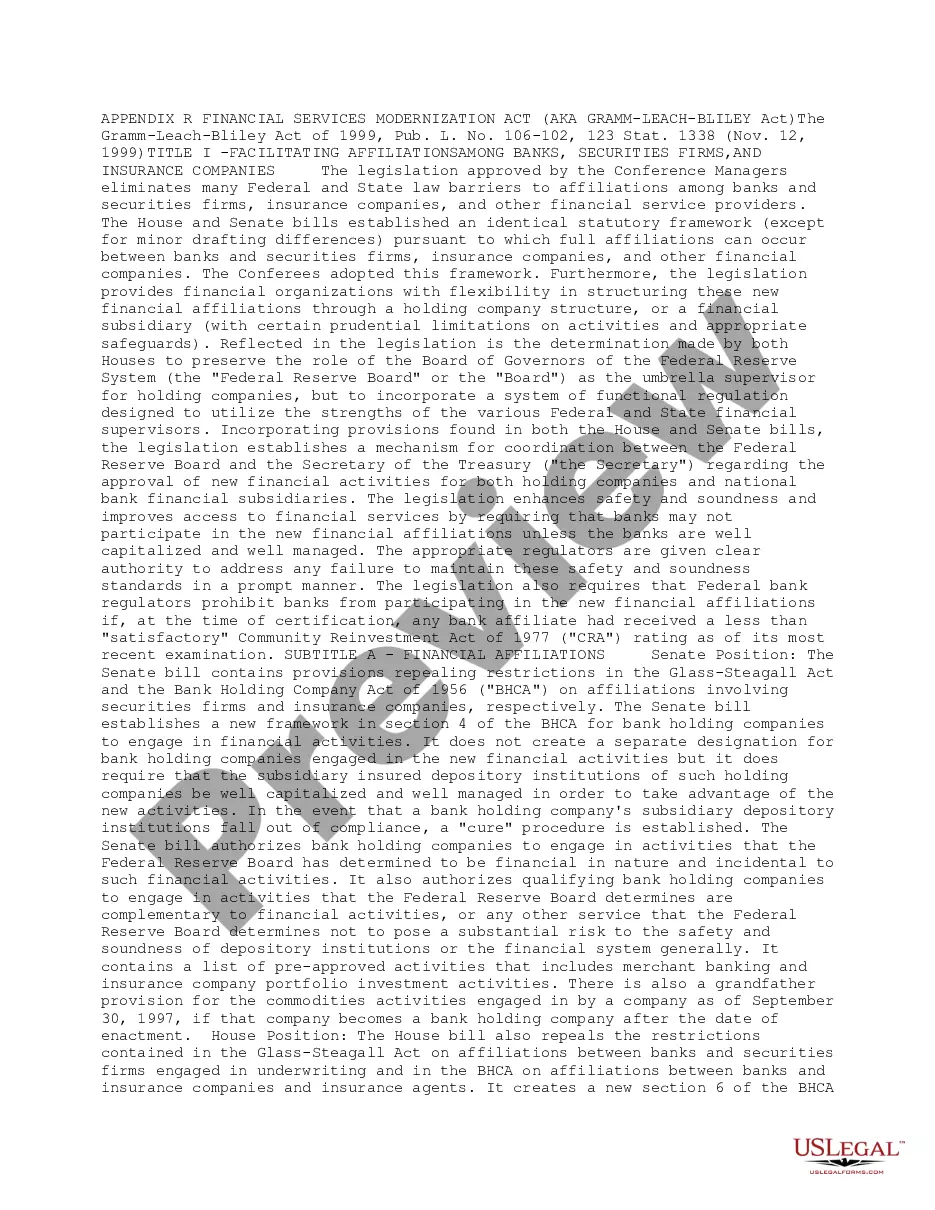

Full text and statutory guidelines for the Financial Services Modernization Act (Gramm-Leach-Bliley Act)

The Wayne Michigan Financial Services Modernization Act, also known as the Gramm-Leach-Bliley Act (ALBA), is a significant piece of legislation that revolutionized the financial industry in the United States. Enacted by Congress in 1999, this act aimed to modernize and update the regulatory framework for financial services, enhance competition, and provide consumers with greater protection. The ALBA encompasses several critical provisions that target different aspects of the financial services sector. Here are the key components within the Act: 1. Privacy Requirements: The ALBA mandates financial institutions to establish privacy policies and implement procedures to protect their customers' non-public personal information. Covered institutions are required to provide customers with privacy notices, disclosing the types of information collected, how it is shared, and the right of the customer to opt-out of certain data-sharing practices. 2. Financial Privacy: This section of the ALBA demands that financial institutions provide customers the opportunity to opt-out of sharing their personal financial information with non-affiliated third parties. It also sets guidelines for data security and requires institutions to implement safeguards to protect customer information from unauthorized access or use. 3. Consumer Protections: The Act tasks federal banking agencies with ensuring that financial institutions conduct their financial operations fairly and transparently. It promotes competition by removing barriers between banks and other financial entities, allowing for diversification of services offered by financial institutions. 4. Insurance Activities: The ALBA permits banks and financial institutions to engage in insurance activities under certain conditions. It establishes a regulatory framework for these activities, including licensing requirements and regulatory oversight. 5. Securities Activities: Under the Act, banks were allowed to supplement their traditional banking services with securities activities. This provision led to a blurring of the lines between banking and investment services, enabling institutions to cater to a broader range of customer needs. 6. Wayne Michigan-specific Amendments: While the ALBA sets regulations at a federal level, Wayne Michigan has introduced its own amendments to refine the application of the Act within the state. These amendments may include additional consumer protections or specific criteria for financial institutions operating in Wayne Michigan. The Wayne Michigan Financial Services Modernization Act, or Gramm-Leach-Bliley Act, stands as a landmark regulation that transformed the financial services landscape. By striking a balance between providing customers with privacy and enhancing competition, it continues to shape the way financial institutions operate today. Compliance with the ALBA and its Wayne Michigan-specific amendments are crucial for financial institutions to uphold transparency, safeguard customer information, and ensure fair practices in the provision of financial services.The Wayne Michigan Financial Services Modernization Act, also known as the Gramm-Leach-Bliley Act (ALBA), is a significant piece of legislation that revolutionized the financial industry in the United States. Enacted by Congress in 1999, this act aimed to modernize and update the regulatory framework for financial services, enhance competition, and provide consumers with greater protection. The ALBA encompasses several critical provisions that target different aspects of the financial services sector. Here are the key components within the Act: 1. Privacy Requirements: The ALBA mandates financial institutions to establish privacy policies and implement procedures to protect their customers' non-public personal information. Covered institutions are required to provide customers with privacy notices, disclosing the types of information collected, how it is shared, and the right of the customer to opt-out of certain data-sharing practices. 2. Financial Privacy: This section of the ALBA demands that financial institutions provide customers the opportunity to opt-out of sharing their personal financial information with non-affiliated third parties. It also sets guidelines for data security and requires institutions to implement safeguards to protect customer information from unauthorized access or use. 3. Consumer Protections: The Act tasks federal banking agencies with ensuring that financial institutions conduct their financial operations fairly and transparently. It promotes competition by removing barriers between banks and other financial entities, allowing for diversification of services offered by financial institutions. 4. Insurance Activities: The ALBA permits banks and financial institutions to engage in insurance activities under certain conditions. It establishes a regulatory framework for these activities, including licensing requirements and regulatory oversight. 5. Securities Activities: Under the Act, banks were allowed to supplement their traditional banking services with securities activities. This provision led to a blurring of the lines between banking and investment services, enabling institutions to cater to a broader range of customer needs. 6. Wayne Michigan-specific Amendments: While the ALBA sets regulations at a federal level, Wayne Michigan has introduced its own amendments to refine the application of the Act within the state. These amendments may include additional consumer protections or specific criteria for financial institutions operating in Wayne Michigan. The Wayne Michigan Financial Services Modernization Act, or Gramm-Leach-Bliley Act, stands as a landmark regulation that transformed the financial services landscape. By striking a balance between providing customers with privacy and enhancing competition, it continues to shape the way financial institutions operate today. Compliance with the ALBA and its Wayne Michigan-specific amendments are crucial for financial institutions to uphold transparency, safeguard customer information, and ensure fair practices in the provision of financial services.