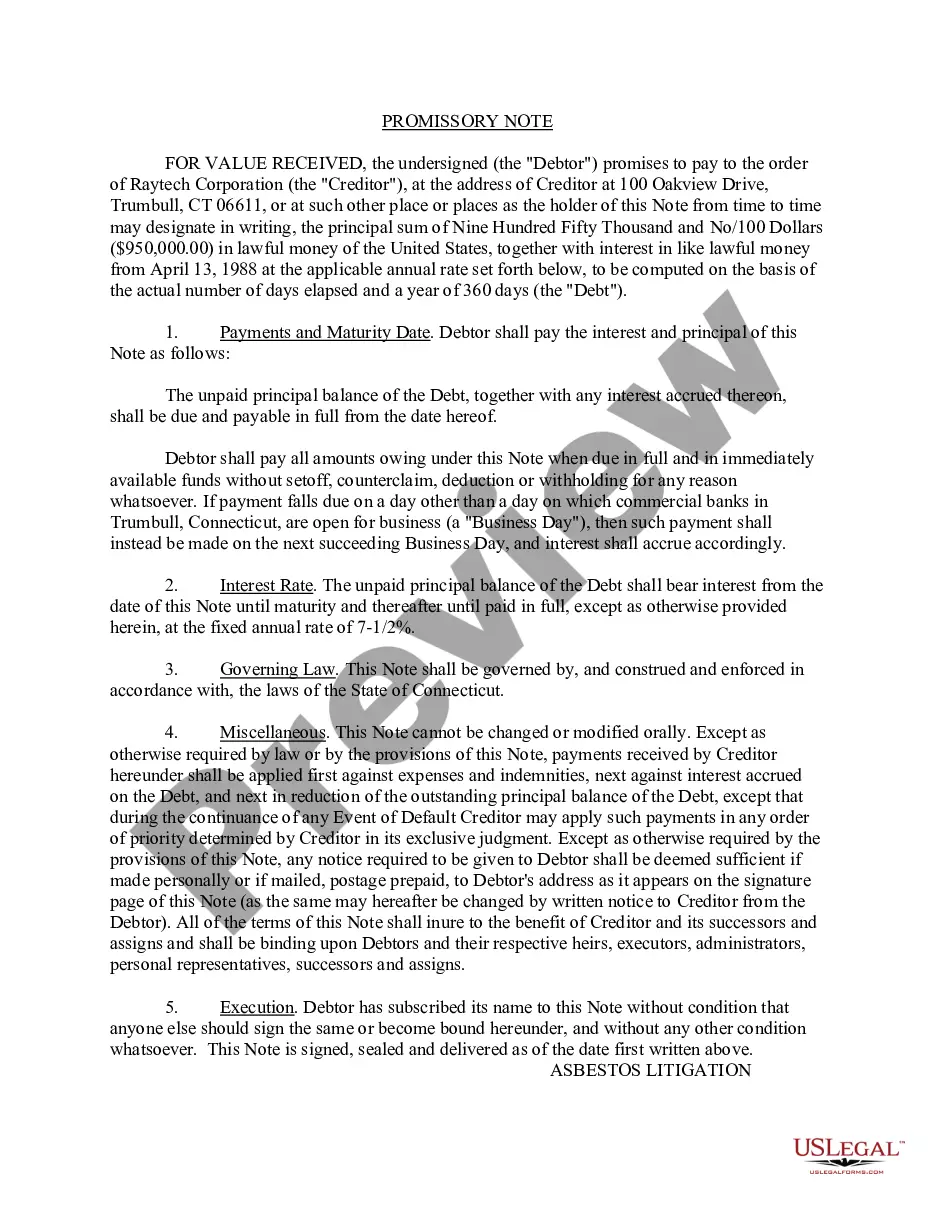

A Nassau New York Promissory Note is a legally binding document that outlines the terms and conditions of a loan agreement between two parties. It serves as an acknowledgment of a debt owed by a borrower to a lender. The document contains important information such as the loan amount, interest rate, repayment terms, and the consequences of defaulting on the loan. Nassau New York offers different types of Promissory Notes, each designed to cater to specific needs and circumstances. Some common types of Promissory Notes in Nassau New York include: 1. Unsecured Promissory Note: This type of Promissory Note does not require any collateral from the borrower. It is based solely on the borrower's promise to repay the loan. 2. Secured Promissory Note: This type of Promissory Note is secured by collateral provided by the borrower. In case of default, the lender has the right to seize and sell the collateral to recover the outstanding loan amount. 3. Adjustable-Rate Promissory Note: This type of Promissory Note has an interest rate that can fluctuate based on market conditions. The interest rate may change periodically, resulting in varying monthly payments for the borrower. 4. Fixed-Rate Promissory Note: This type of Promissory Note has a fixed interest rate for the entire loan term. The borrower pays the same amount each month, making it easier to budget and plan for repayment. 5. Demand Promissory Note: This type of Promissory Note allows the lender to demand repayment of the loan at any time within a specified period. The borrower must repay the loan in full upon receiving the lender's demand. 6. Installment Promissory Note: This type of Promissory Note divides the loan repayment into equal installments over a specified period. Each installment includes both principal and interest, allowing the borrower to repay the loan gradually. When drafting a Nassau New York Promissory Note, it is crucial to consult with an attorney to ensure compliance with local laws and regulations. The Promissory Note should clearly define the obligations and rights of both parties and provide a legal recourse in the event of default or dispute. It is advisable to include all relevant terms and conditions to protect the interests of both the lender and the borrower.

Nassau New York Promissory Note

Description

How to fill out Nassau New York Promissory Note?

Laws and regulations in every sphere differ around the country. If you're not a lawyer, it's easy to get lost in various norms when it comes to drafting legal documents. To avoid pricey legal assistance when preparing the Nassau Promissory Note, you need a verified template legitimate for your county. That's when using the US Legal Forms platform is so helpful.

US Legal Forms is a trusted by millions web catalog of more than 85,000 state-specific legal templates. It's a great solution for specialists and individuals looking for do-it-yourself templates for various life and business situations. All the forms can be used multiple times: once you pick a sample, it remains available in your profile for subsequent use. Thus, if you have an account with a valid subscription, you can simply log in and re-download the Nassau Promissory Note from the My Forms tab.

For new users, it's necessary to make a few more steps to get the Nassau Promissory Note:

- Examine the page content to make sure you found the right sample.

- Use the Preview option or read the form description if available.

- Search for another doc if there are inconsistencies with any of your criteria.

- Click on the Buy Now button to obtain the document when you find the proper one.

- Opt for one of the subscription plans and log in or sign up for an account.

- Decide how you prefer to pay for your subscription (with a credit card or PayPal).

- Pick the format you want to save the document in and click Download.

- Fill out and sign the document in writing after printing it or do it all electronically.

That's the simplest and most economical way to get up-to-date templates for any legal purposes. Locate them all in clicks and keep your documentation in order with the US Legal Forms!