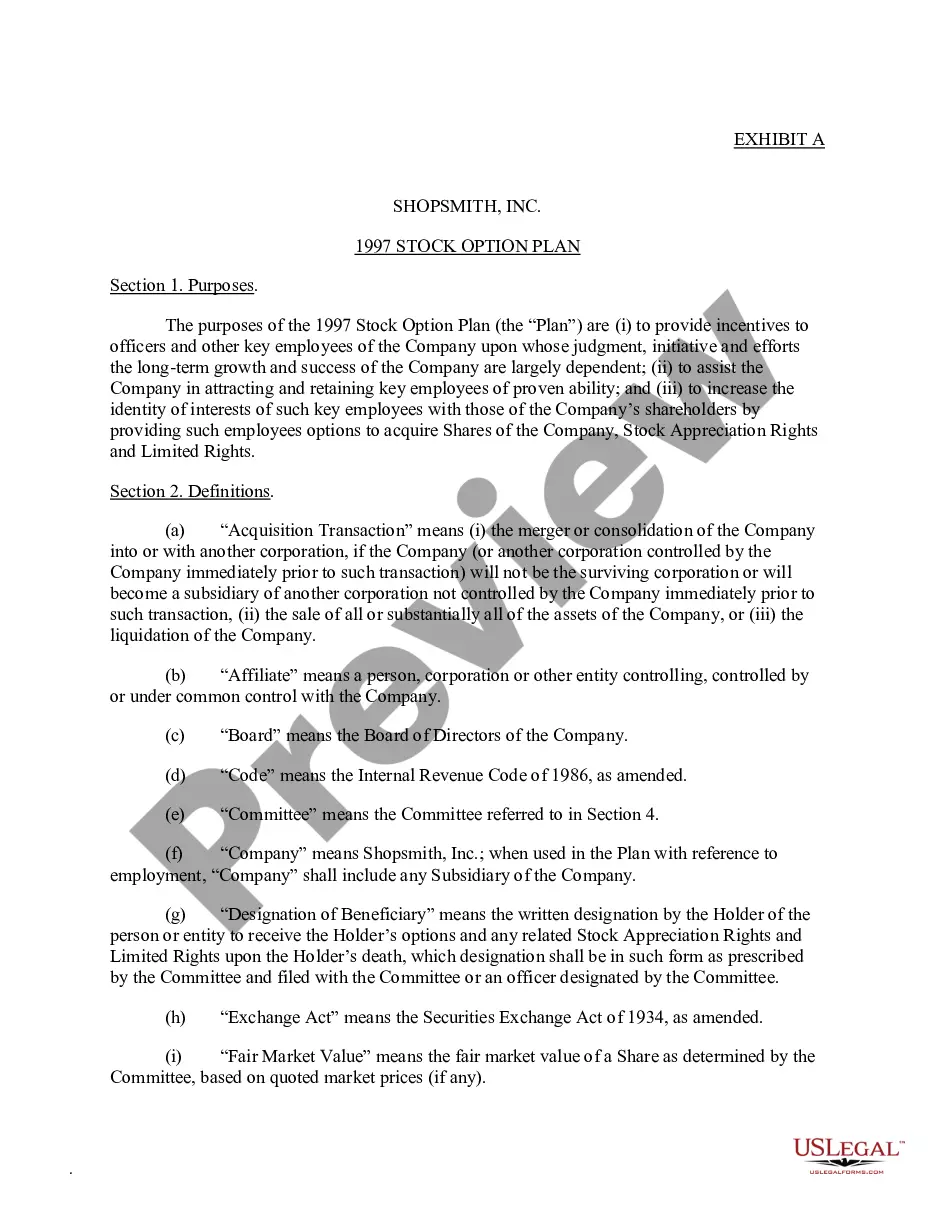

18-219B 18-219B . . . Stock Option Plan which provides for grant of Incentive Stock Options, (b) Non-qualified Stock Options, and (c) Exchange Options under which employees of the corporation or any of its subsidiaries can exchange (i) all of their options for shares of a subsidiary that were granted under that subsidiary's stock option plan and are outstanding as of the date of adoption of this Plan and all their awards under that subsidiary's Restricted Stock Plan for restricted shares of that subsidiary's stock that are outstanding as of the date of adoption of this Plan and receive therefor non-qualified options for shares under this Plan, (ii) all of their restricted shares of a subsidiary that were issued under the subsidiary's Performance Restricted Stock Plan and receive therefor non-qualified options for shares under this Plan, and (iii) all of their stock appreciation rights with respect to shares of a subsidiary that were granted under that subsidiary's Stock Appreciation Rights Plan and receive therefor non-qualified options for shares under this Plan

Franklin Ohio Stock Option Plan Stock Option Plan which provides for grant of Incentive Stock Options, Nonqualified Stock Options, and Exchange Options

Category:

State:

Multi-State

County:

Franklin

Control #:

US-CC-18-219B

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Stock Option Plan Stock Option Plan Which Provides For Grant Of Incentive Stock Options, Nonqualified Stock Options, And Exchange Options?

Drafting documents, such as the Franklin Stock Option Plan which allows for the issuance of Incentive Stock Options, Nonqualified Stock Options, and Exchange Options, to handle your legal issues is a daunting and time-intensive endeavor.

Numerous situations necessitate the involvement of a lawyer, which consequently renders this task rather costly.

Nonetheless, you can take control of your legal matters and manage them independently.

The onboarding experience for new clients is equally straightforward! Here’s what you need to do before acquiring the Franklin Stock Option Plan that allows for the issuance of Incentive Stock Options, Nonqualified Stock Options, and Exchange Options.

- US Legal Forms is here to assist you.

- Our platform offers over 85,000 legal documents designed for different scenarios and life events.

- We guarantee that every form adheres to the laws of each state, alleviating your concerns about possible legal compliance issues.

- If you are already acquainted with our offerings and hold a subscription with US Legal Forms, you understand how seamless it is to obtain the Franklin Stock Option Plan that provides for the issuance of Incentive Stock Options, Nonqualified Stock Options, and Exchange Options.

- Feel free to Log In to your account, retrieve the template, and customize it to fit your preferences.

- Have you misplaced your document? No need to panic. You can access it in the My documents section of your account - available on both desktop and mobile devices.

Form popularity

FAQ

An incentive stock option (ISO) is a corporate benefit that gives an employee the right to buy shares of company stock at a discounted price with the added benefit of possible tax breaks on the profit.

Incentive stock options, or ISOs, are options that are entitled to potentially favorable federal tax treatment. Stock options that are not ISOs are usually referred to as nonqualified stock options or NQOs. The acronym NSO is also used. These do not qualify for special tax treatment.

Key Takeaways. Non-qualified stock options require payment of income tax of the grant price minus the price of the exercised option. NSOs might be provided as an alternative form of compensation. Prices are often similar to the market value of the shares.

What Is a Non-Qualified Stock Option (NSO)? A non-qualified stock option (NSO) is a type of employee stock option wherein you pay ordinary income tax on the difference between the grant price and the price at which you exercise the option.

Non-qualified stock options are stock options that do not receive favorable tax treatment when exercised but do provide additional flexibility for the issuing company. Gains from non-qualified stock options are taxed as normal income.

Qualified stock options, also known as incentive stock options, can only be granted to employees. Non-qualified stock options can be granted to employees, directors, contractors and others. This gives you greater flexibility to recognize the contributions of non-employees.

Only income taxes apply to RSUs, meaning the capital gains tax is not a factor. On the other hand, two types of stock options exist. These are non-qualified stock options (NSOs) and incentive stock options (ISOs). For NSOs, you are taxed on the difference between the market price and the grant price.

A nonqualified stock option, also known as an NSO, is a form of employee compensation offered by employers wherein the option holder pays ordinary income tax on the profit made when they exercise the shares.

However, there is another type of stock option, known as an incentive stock option, which is usually only offered to key employees and top-tier management. These options are also commonly known as statutory or qualified options, and they can receive preferential tax treatment in many cases.

Profits made from exercising qualified stock options (QSO) are taxed at the capital gains tax rate (typically 15%), which is lower than the rate at which ordinary income is taxed. Gains from non-qualified stock options (NQSO) are considered ordinary income and are therefore not eligible for the tax break.