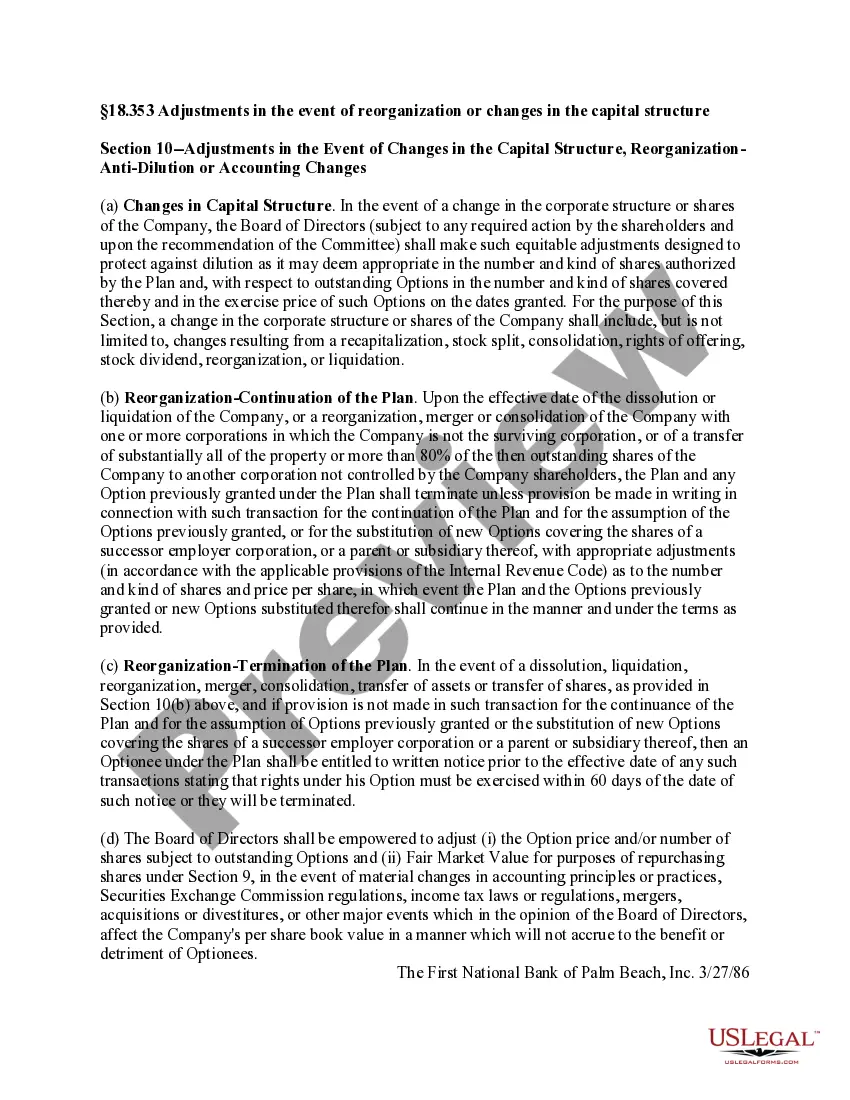

When it comes to reorganization or changes in the capital structure, Franklin Ohio Adjustments play a vital role in ensuring smooth transitions and effective financial management. Franklin Ohio Adjustments are specific accounting changes made by a company in response to reorganization or alterations in its capital structure. These adjustments help maintain accurate financial records and reflect the impact of such changes. There are different types of Franklin Ohio Adjustments that can be implemented in the event of a reorganization or changes in the capital structure. Some key types include: 1. Debt Restructuring Adjustments: This type of adjustment is made when a company undergoes debt restructuring, such as negotiating new loan terms, converting debt into equity, or issuing new debt instruments. The accounting procedures are adjusted to reflect the new debt arrangements accurately, ensuring correct disclosure of liabilities and interest expenses. 2. Equity Issuance Adjustments: When a company decides to issue new equity, such as common stock or preferred stock, to raise capital or change its ownership structure, equity issuance adjustments come into play. These adjustments affect the company's balance sheet by reflecting changes in shareholders' equity, including the addition of new shares and corresponding changes in common stock, additional paid-in capital, and retained earnings. 3. Merger and Acquisition Adjustments: In the case of mergers, acquisitions, or other business combinations, Franklin Ohio Adjustments help account for the changes in assets, liabilities, and equity resulting from the transaction. These adjustments ensure that the company's financial statements accurately reflect the impact of the combination, including the fair valuation of acquired assets and liabilities and the recognition of goodwill or bargain purchase gain. 4. Divestiture Adjustments: When a company divests a subsidiary, business segment, or any other asset, divestiture adjustments are necessary to reflect the removal of the associated assets and liabilities from the financial statements. These adjustments often involve accounting for discontinued operations, impairment of assets, and the recognition of any retained interest in the divested entity. 5. Capital Structure Adjustment: In situations where a company undergoes a significant change in its capital structure, such as debt-to-equity swaps, recapitalization, or reissuance of shares, capital structure adjustments are made. These adjustments aim to align the financial records with the new capital structure and accurately portray the changes in debt-to-equity ratios and related financial metrics. Overall, Franklin Ohio Adjustments in the event of reorganization or changes in the capital structure are essential for maintaining transparency and accuracy in financial reporting. By implementing these adjustments, companies can uphold their fiduciary responsibilities by providing relevant information to stakeholders, investors, and regulatory bodies.

Franklin Ohio Adjustments in the event of reorganization or changes in the capital structure

Description

How to fill out Franklin Ohio Adjustments In The Event Of Reorganization Or Changes In The Capital Structure?

Laws and regulations in every sphere vary throughout the country. If you're not a lawyer, it's easy to get lost in a variety of norms when it comes to drafting legal paperwork. To avoid high priced legal assistance when preparing the Franklin Adjustments in the event of reorganization or changes in the capital structure, you need a verified template legitimate for your region. That's when using the US Legal Forms platform is so advantageous.

US Legal Forms is a trusted by millions web collection of more than 85,000 state-specific legal templates. It's a perfect solution for professionals and individuals searching for do-it-yourself templates for various life and business occasions. All the forms can be used many times: once you purchase a sample, it remains available in your profile for subsequent use. Therefore, when you have an account with a valid subscription, you can simply log in and re-download the Franklin Adjustments in the event of reorganization or changes in the capital structure from the My Forms tab.

For new users, it's necessary to make a couple of more steps to get the Franklin Adjustments in the event of reorganization or changes in the capital structure:

- Take a look at the page content to ensure you found the right sample.

- Use the Preview option or read the form description if available.

- Search for another doc if there are inconsistencies with any of your criteria.

- Utilize the Buy Now button to get the document when you find the proper one.

- Opt for one of the subscription plans and log in or create an account.

- Decide how you prefer to pay for your subscription (with a credit card or PayPal).

- Pick the format you want to save the document in and click Download.

- Complete and sign the document on paper after printing it or do it all electronically.

That's the easiest and most economical way to get up-to-date templates for any legal reasons. Find them all in clicks and keep your documentation in order with the US Legal Forms!