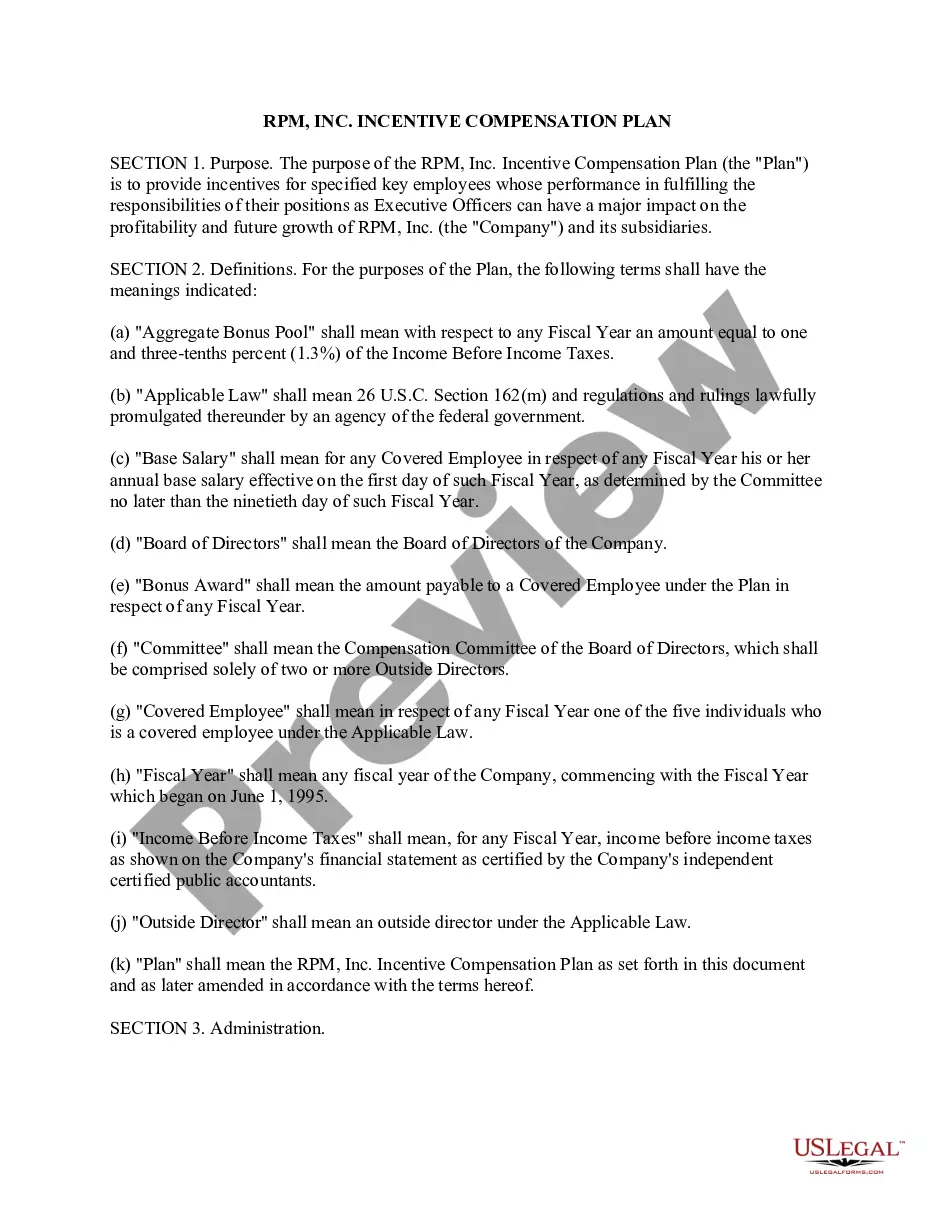

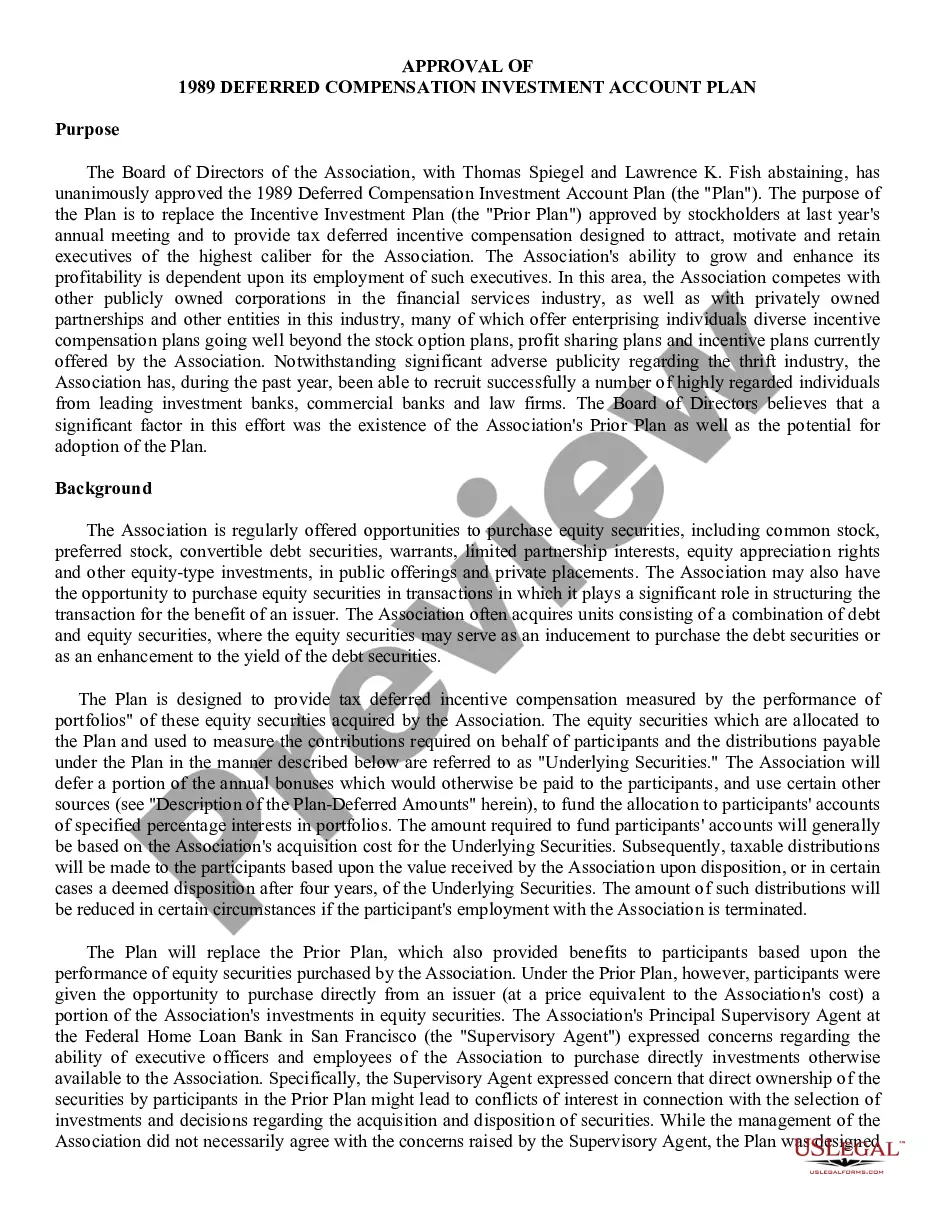

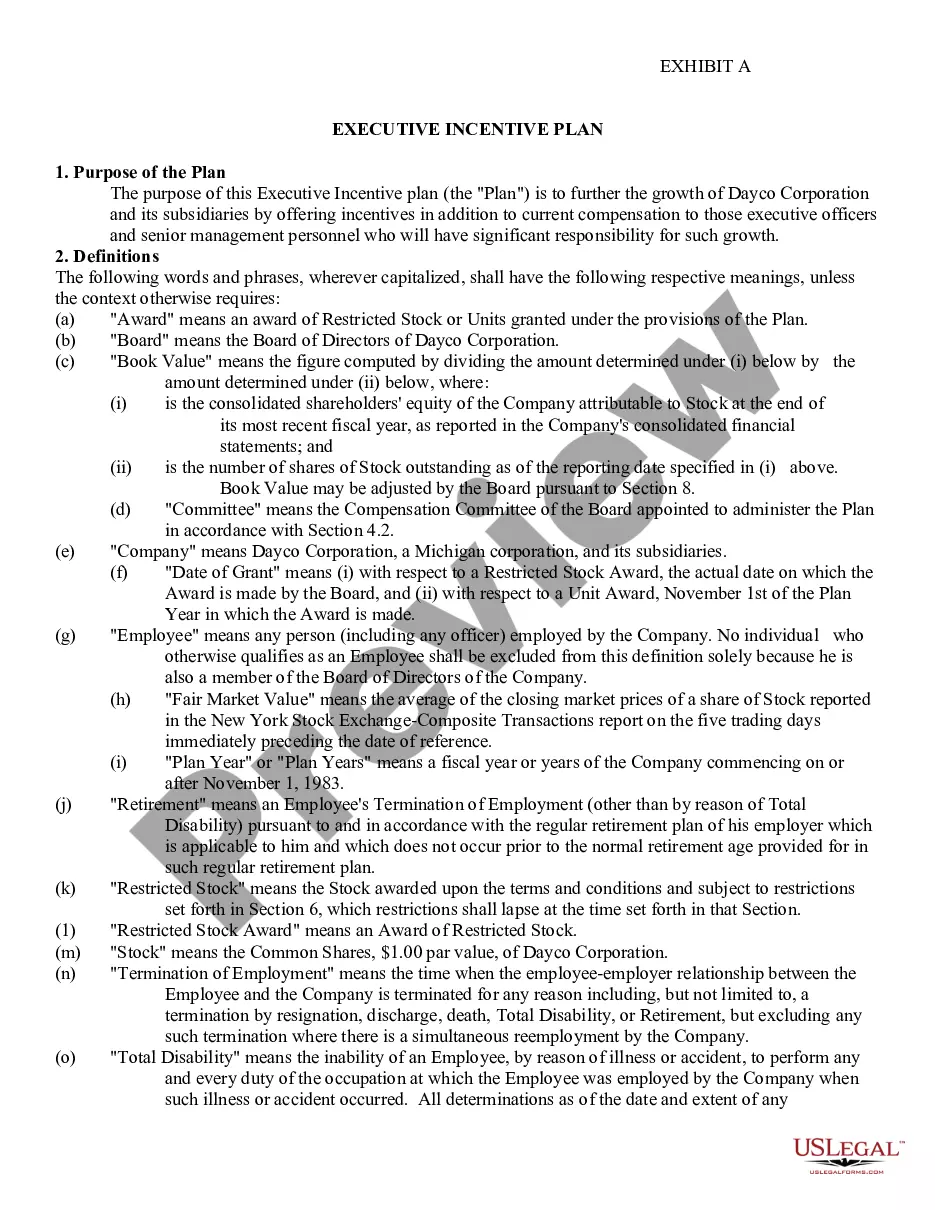

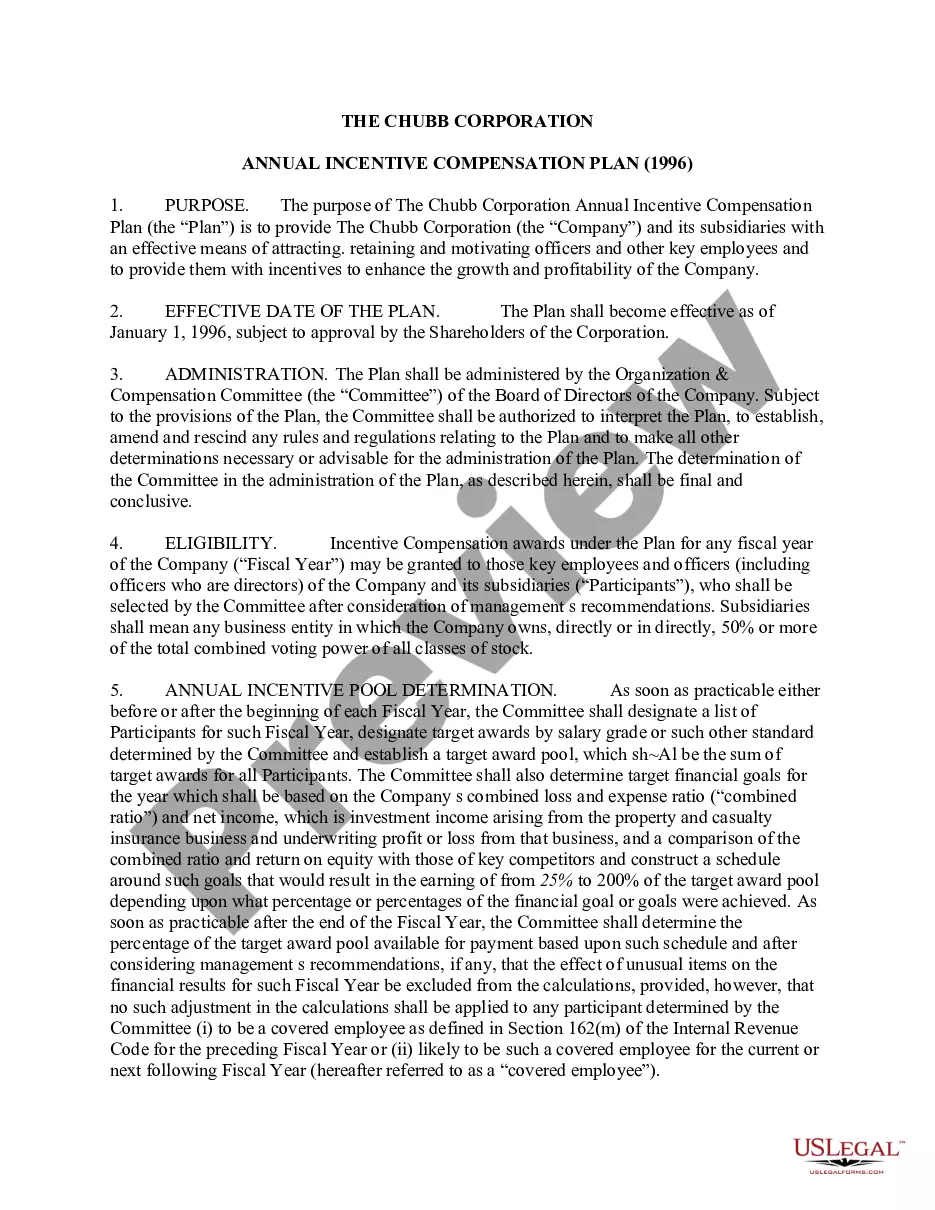

20-146 20-146 . . . Deferred Compensation Investment Account Plan under which Board of Directors of Savings and Loan Association allocates a portion of annual bonuses which would otherwise be paid to selected officers and employees to a separate account. The deferred compensation in such account is deemed, for purposes of Plan only, to represent specified percentages of Association's investments in certain portfolios of equity securities, and it is increased or decreased to same extent as performance of such securities

Alameda California Deferred Compensation Investment Account Plan

State:

Multi-State

County:

Alameda

Control #:

US-CC-20-146

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Deferred Compensation Investment Account Plan?

Whether you plan to establish your business, engage in a transaction, request your ID renewal, or address family-related legal matters, you must prepare specific documentation in accordance with your local laws and regulations.

Finding the appropriate papers may require considerable time and effort unless you utilize the US Legal Forms library.

The platform offers users over 85,000 professionally drafted and validated legal templates for any personal or business circumstance. All documents are categorized by state and area of use, making it quick and easy to select a copy like the Alameda Deferred Compensation Investment Account Plan.

Forms available in our library are reusable. With an active subscription, you can access all of your previously purchased documents at any time from the My documents section of your profile. Stop squandering time on a never-ending search for current official documents. Join the US Legal Forms platform and organize your paperwork using the most comprehensive online form library!

- Ensure the sample meets your specific needs and complies with state law regulations.

- Review the form description and examine the Preview if available on the page.

- Use the search bar provided for your state above to find another template.

- Click Buy Now to acquire the file once you identify the accurate one.

- Choose the subscription plan that best fits your requirements to continue.

- Log in to your account and pay the service using a credit card or PayPal.

- Download the Alameda Deferred Compensation Investment Account Plan in your desired file format.

- Print the copy or complete it and sign it digitally via an online editor to save time.

Form popularity

FAQ

A deferred compensation plan withholds a portion of an employee's pay until a specified date, usually retirement. The lump sum owed to an employee in this type of plan is paid out on that date. Examples of deferred compensation plans include pensions, 401(k) retirement plans, and employee stock options.

But because these plans are not qualified retirement plans, the money you have in a deferred compensation plan is generally not protected from the company's creditors. So if your employer gets into financial difficulty, or goes bankrupt, your savings may be seized to pay the company's liabilities.

One easy way to increase your retirement savings is to contribute a percentage of your income to your Deferred Compensation Plan (DCP) account. Consider saving between 7% and 10% of your salary.

You can leave the money in the account, withdraw in full or withdraw it in payments. If you are not a spouse, you can withdraw the funds. For more specific information about withdrawal options, contact the DRS record keeper.

A deferred comp plan is most beneficial when you're able to reduce both your present and future tax rates by deferring your income. Unfortunately, it's challenging to project future tax rates. This takes analysis, projections, and assumptions.

Unlike a 401k with contributions housed in a trust and protected from the employer's (and the employee's) creditors, a deferred compensation plan (generally) offers no such protections. Instead, the employee only has a claim under the plan for the deferred compensation.

A deferred compensation plan allows a portion of an employee's compensation to be paid at a later date, usually to reduce income taxes. Because taxes on this income are deferred until it is paid out, these plans can be attractive to high earners.

Unlike a 401(k) or traditional IRA, there are no contribution limits for a deferred compensation plan. The 401(k) plan contribution limits for 2021 are $19,500, or $26,000 if you are 50 or older. Traditional IRAs have a maximum contribution of $6,000 in 2021, or $7,000 if you are at least 50 years old.

You may keep your contributions in the Plan and continue to build savings for retirement. However, you may withdraw your contributions if you: Have a Plan account balance of less than $5,000, exclusive of any assets you may have in a rollover account, AND. Have not contributed to the Plan in the last two years, AND.

Executive deferred compensation plans are an excellent way to attract and keep high-income executives since they can't roll over their contributions and keep them when they retire. If you are an executive, learn about these plans before you invest, including the pros and cons.