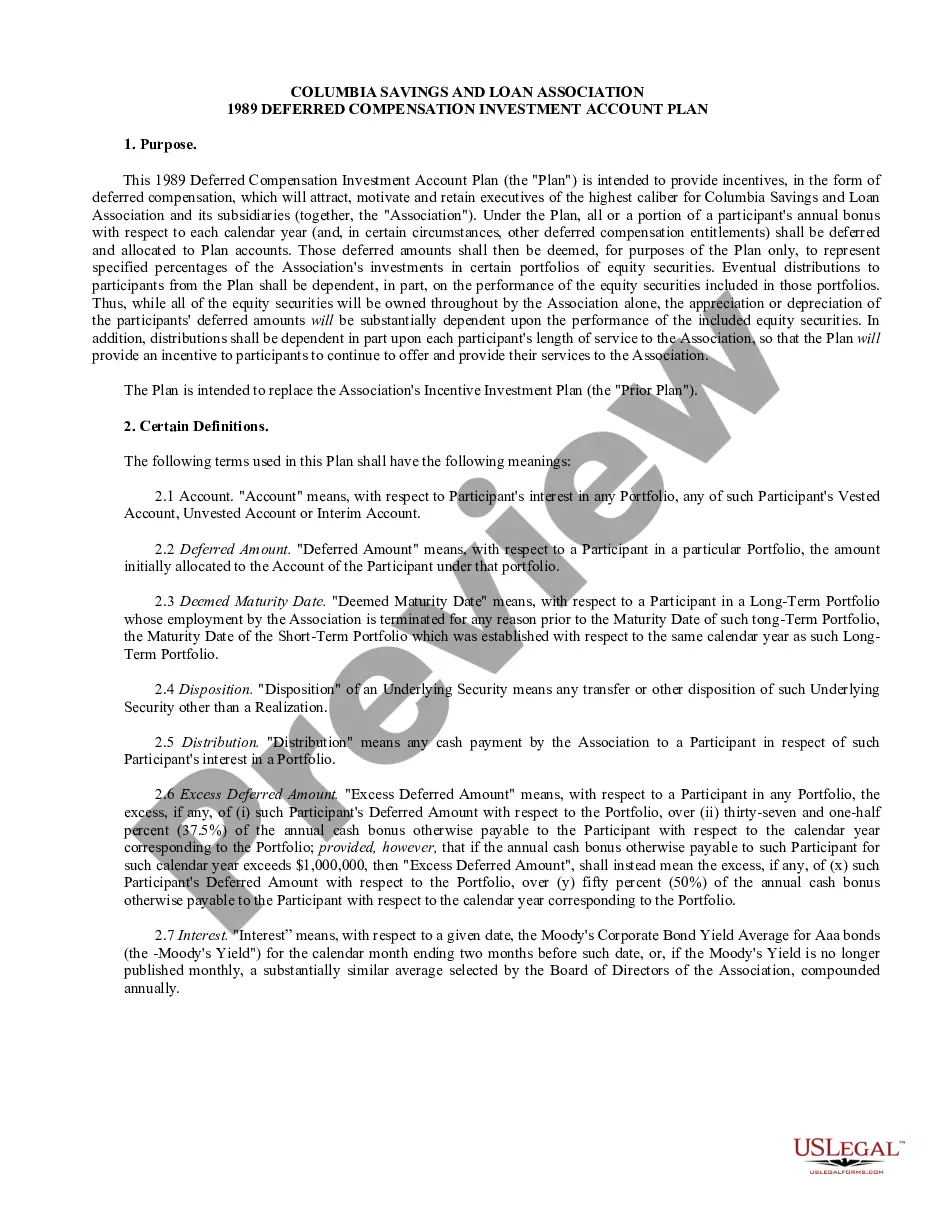

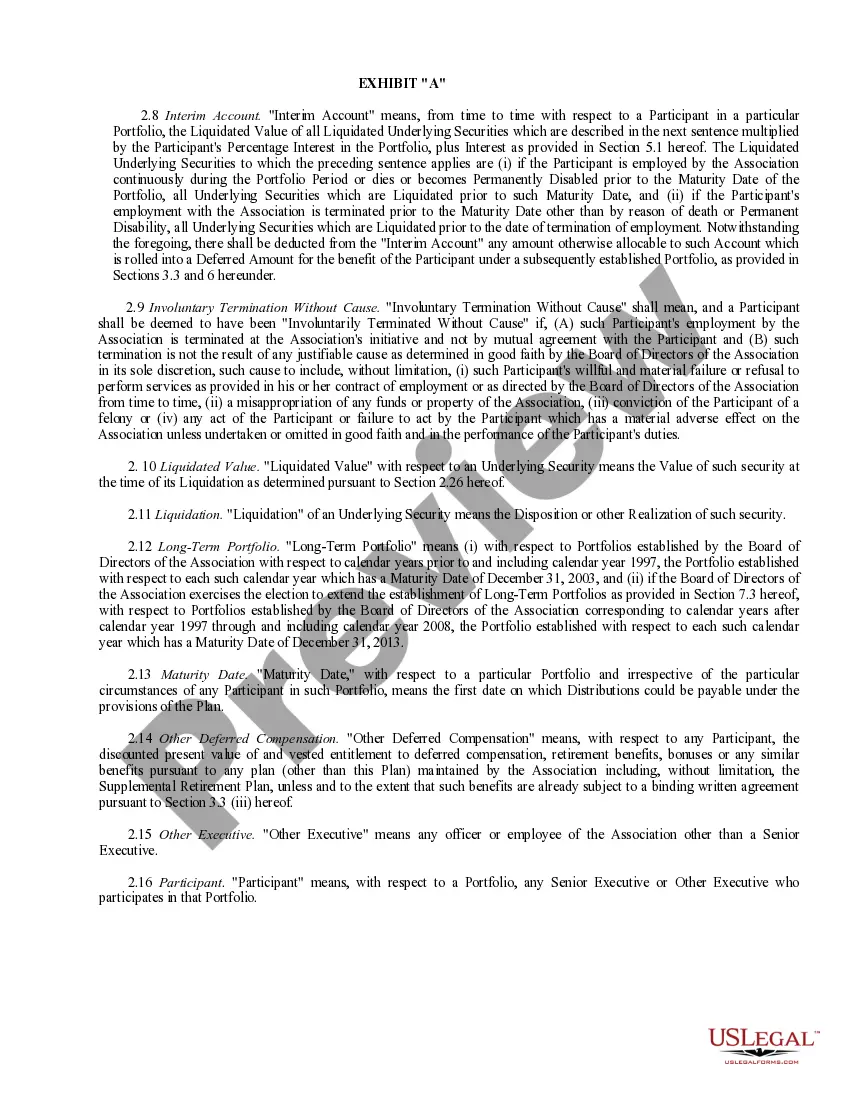

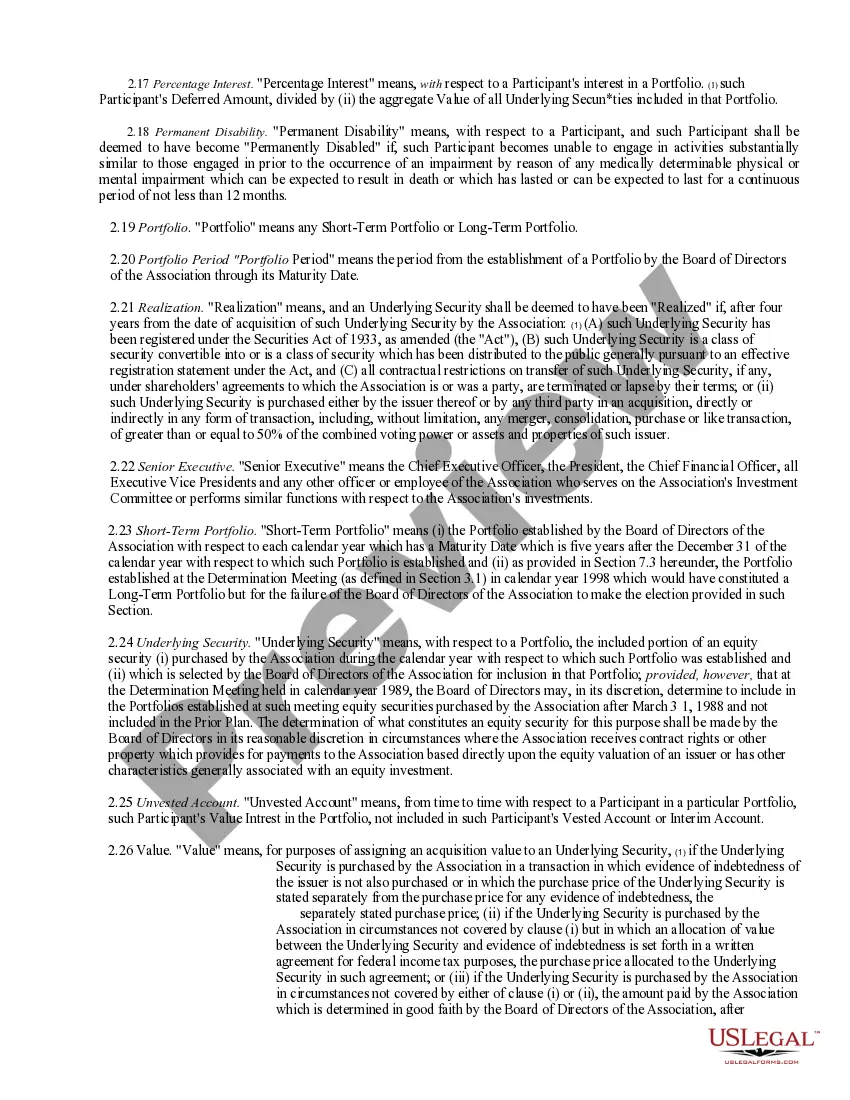

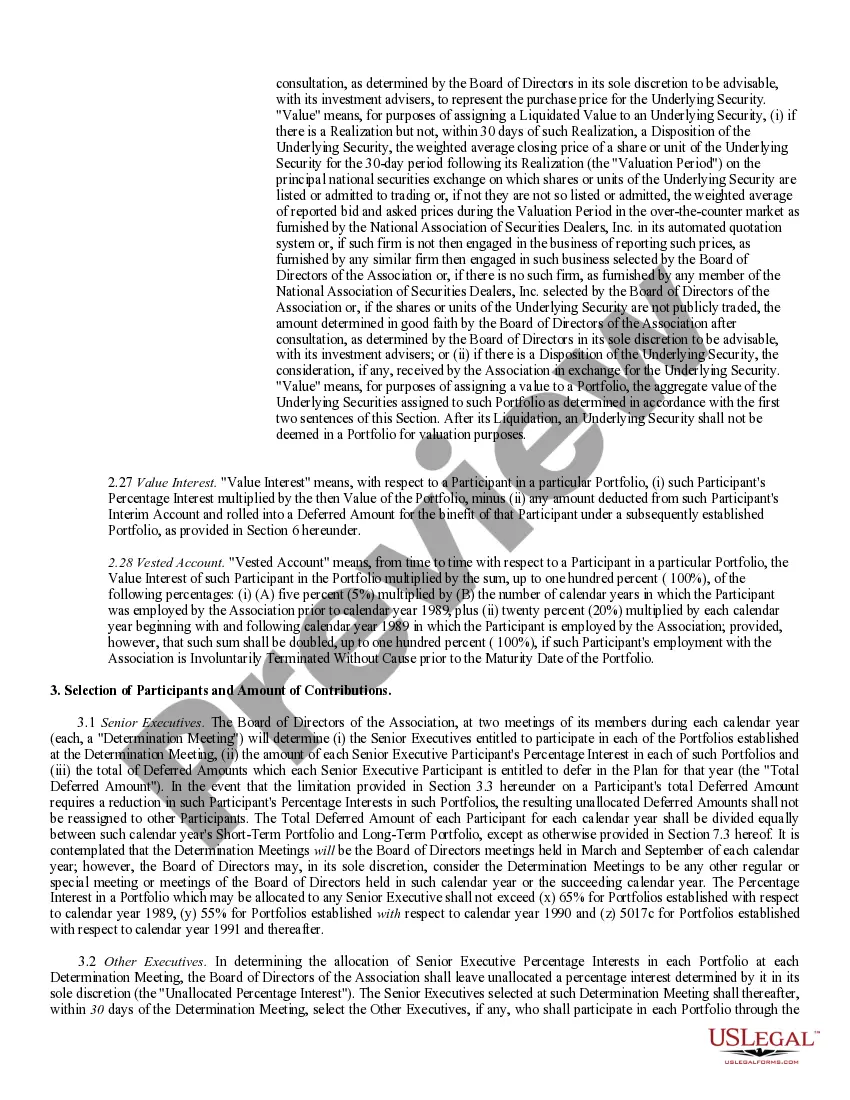

The Mecklenburg North Carolina Deferred Compensation Investment Account Plan is a retirement savings program offered to employees of Mecklenburg County, North Carolina. This voluntary plan allows employees to set aside a portion of their pre-tax income for investment, which helps them build a nest egg for their retirement years. The Mecklenburg North Carolina Deferred Compensation Investment Account Plan offers several advantages to participants. Firstly, it allows employees to defer income tax on the portion of their salary that they contribute to the plan. This means that the money contributed is not taxed until it is withdrawn at retirement. Secondly, participants can choose from a wide array of investment options to grow their savings, including mutual funds, stocks, bonds, and more. This flexibility enables employees to tailor their investment strategy according to their risk tolerance and financial goals. One of the different types of Mecklenburg North Carolina Deferred Compensation Investment Account Plan is the 457(b) plan. This plan is specifically designed for employees of government and nonprofit organizations, offering them additional tax benefits and higher contribution limits compared to traditional employer-sponsored retirement plans. The 457(b) plan allows employees to contribute a certain percentage of their income, up to a maximum limit determined by the Internal Revenue Service (IRS). Participants can allocate their contributions among various investment options provided by the plan. Another type of Mecklenburg North Carolina Deferred Compensation Investment Account Plan is the Roth 457(b) plan. This plan is similar to the traditional 457(b) plan in terms of contribution limits and investment options, but it differs in terms of taxation. With the Roth 457(b) plan, employees contribute after-tax income into their retirement account. Although these contributions are not tax-deductible, the earnings and withdrawals in retirement are tax-free, providing potential tax advantages during retirement. Participants in the Mecklenburg North Carolina Deferred Compensation Investment Account Plan have access to various resources and support systems. These may include online tools and calculators to help plan contributions, personalized investment advice, and educational materials to improve financial literacy. Additionally, participants can monitor their account balance, investment performance, and make changes to their investment strategy online. In conclusion, the Mecklenburg North Carolina Deferred Compensation Investment Account Plan is a retirement savings program offered to employees of Mecklenburg County, providing them with tax advantages and investment options to build a secure financial future. The plan includes different types such as the traditional 457(b) plan and the Roth 457(b) plan, offering flexibility and catering to different financial needs and goals.

Mecklenburg North Carolina Deferred Compensation Investment Account Plan

Description

How to fill out Mecklenburg North Carolina Deferred Compensation Investment Account Plan?

Preparing legal paperwork can be cumbersome. In addition, if you decide to ask a lawyer to write a commercial agreement, papers for proprietorship transfer, pre-marital agreement, divorce paperwork, or the Mecklenburg Deferred Compensation Investment Account Plan, it may cost you a lot of money. So what is the best way to save time and money and create legitimate forms in total compliance with your state and local regulations? US Legal Forms is an excellent solution, whether you're looking for templates for your personal or business needs.

US Legal Forms is largest online collection of state-specific legal documents, providing users with the up-to-date and professionally checked templates for any scenario gathered all in one place. Therefore, if you need the latest version of the Mecklenburg Deferred Compensation Investment Account Plan, you can easily find it on our platform. Obtaining the papers requires a minimum of time. Those who already have an account should check their subscription to be valid, log in, and pick the sample using the Download button. If you haven't subscribed yet, here's how you can get the Mecklenburg Deferred Compensation Investment Account Plan:

- Glance through the page and verify there is a sample for your region.

- Examine the form description and use the Preview option, if available, to make sure it's the template you need.

- Don't worry if the form doesn't satisfy your requirements - search for the correct one in the header.

- Click Buy Now when you find the needed sample and pick the best suitable subscription.

- Log in or sign up for an account to pay for your subscription.

- Make a transaction with a credit card or through PayPal.

- Choose the file format for your Mecklenburg Deferred Compensation Investment Account Plan and download it.

Once finished, you can print it out and complete it on paper or upload the template to an online editor for a faster and more convenient fill-out. US Legal Forms allows you to use all the paperwork ever purchased many times - you can find your templates in the My Forms tab in your profile. Try it out now!

Form popularity

FAQ

401(k) and 457(b) plans are similarly structured tax-advantaged retirement savings plans. 401(k) plans are sponsored by private employers, while 457(b) plans are offered by governments and some nonprofits. Contribution limits and the rules for withdrawals are also key differences between the two types of accounts.

There is no penalty for an early withdrawal, but be prepared to pay income tax on any money you withdraw from a 457 plan (at any age). Just like other retirement plans, you do need to start taking distributions from your 457 plan by the age of 70 and a half years old.

Unlike other retirement plans, under the IRC, 457 participants can withdraw funds before the age of 59½ as long as you either leave your employer or have a qualifying hardship. You can take money out of your 457 plan without penalty at any age, although you will have to pay income taxes on any money you withdraw.

16 1 Page 3 Federal tax law requires that most distributions from governmental 457(b) plans that are not directly rolled over to an IRA or other eligible retirement plan be subject to federal income tax withholding at the rate of 20%.

Although you won't pay any 457 early withdrawal penalties, it isn't easy to take money out of your plan if you're still with your employer. The only way you'll be able to is if you have a hardship withdrawal, and you're only allowed to claim a hardship if you have a qualifying unforeseeable emergency.

The 457 plan is a retirement savings plan and you generally cannot withdraw money while you are still employed. When you leave employment, you may withdraw funds; leave them in place; transfer them to a 457, 403(b) or 401(k) of a new employer; or roll them into an Individual Retirement Account (IRA).

If the payment from the Plan is a qualified distribution, you will not be taxed on any part of the payment even if you do not do a rollover. If you do a rollover, you will not be taxed on the amount you roll over and any earnings on the amount you roll over will not be taxed if paid later in a qualified distribution.

Typically, Fidelity says, you and your employer agree on when withdrawals can start. It may be five years, 10 years or not until you reach retirement. If you retire early, get fired or quit for another job before the due date, your employ gets to claw back some of that compensation as a penalty.

Although you won't pay any 457 early withdrawal penalties, it isn't easy to take money out of your plan if you're still with your employer. The only way you'll be able to is if you have a hardship withdrawal, and you're only allowed to claim a hardship if you have a qualifying unforeseeable emergency.

You can take penalty-free withdrawals from your 457 account at any age after you leave your job. Most other types of retirement-savings plans assess a 10% penalty if you withdraw money before age 55 or 59½, depending on when you leave your job.