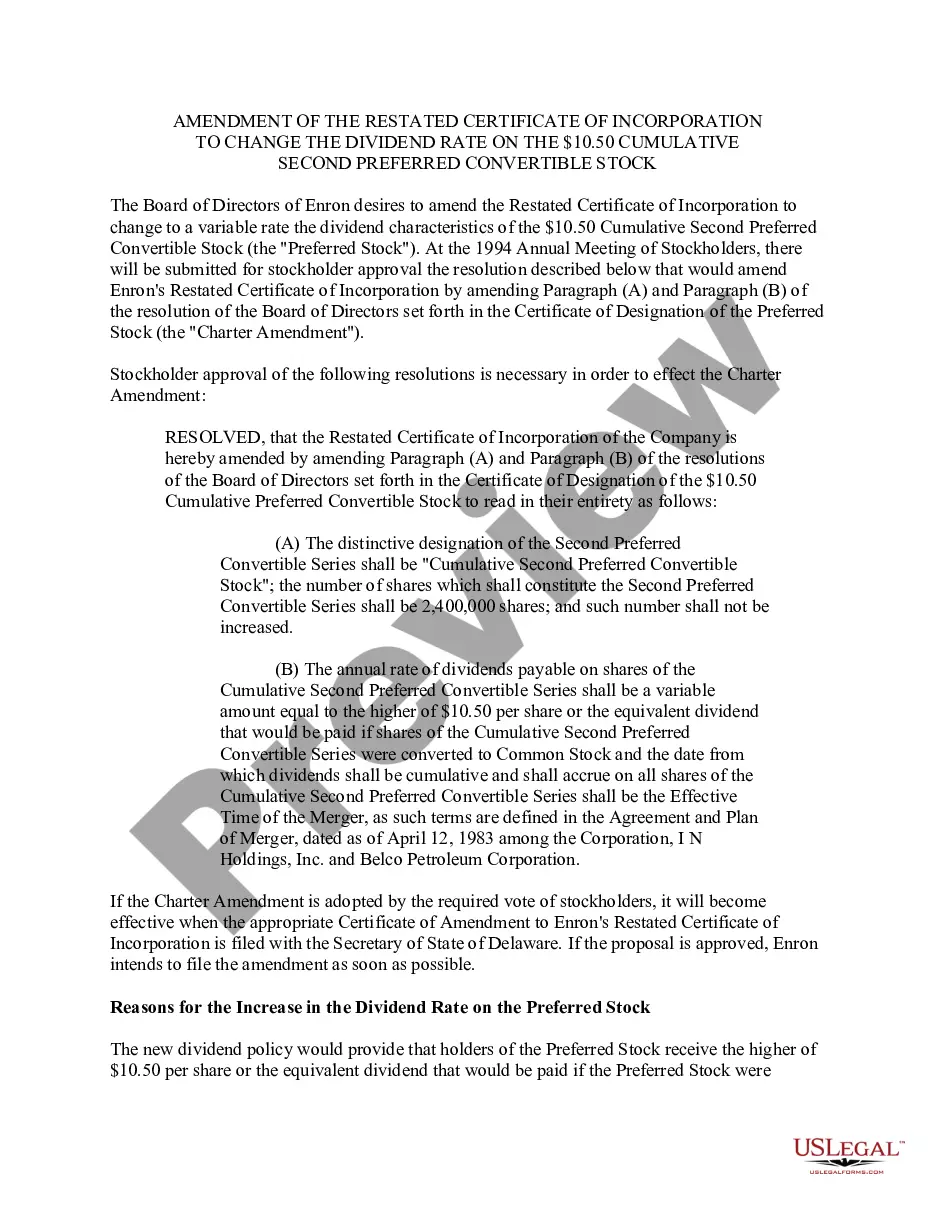

The Collin Texas Amendment of Restated Certificate of Incorporation refers to a specific modification made to the existing certificate of incorporation in the state of Texas. This amendment specifically targets the change in the dividend rate on the $10.50 cumulative second preferred convertible stock. The purpose of this amendment is to adjust the rate at which dividends are paid out to shareholders holding the $10.50 cumulative second preferred convertible stock. The original dividend rate may no longer be suitable or competitive in the current market conditions, prompting the need for this change. By modifying the dividend rate, the company endeavors to provide a more desirable return on investment for shareholders holding this particular class of stock. The amendment aims to attract potential investors and retain existing ones by offering a more favorable dividend payout. This amendment is highly significant for shareholders who have invested in the $10.50 cumulative second preferred convertible stock, as their potential earnings from dividends will be directly affected. It is crucial for these shareholders to review the details of this amendment to understand how it may impact their investments. In addition to the Collin Texas Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock, there may be other types of similar amendments related to different classes of stock or specific changes to the certificate of incorporation. Some potential variations may include amendments to adjust dividend rates for other classes of preferred stock, amendments to modify voting rights, or amendments to alter the rights and privileges associated with different types of shares. Overall, the Collin Texas Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock signifies a strategic decision made by the company to optimize shareholder value and promote investor confidence.

Collin Texas Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock

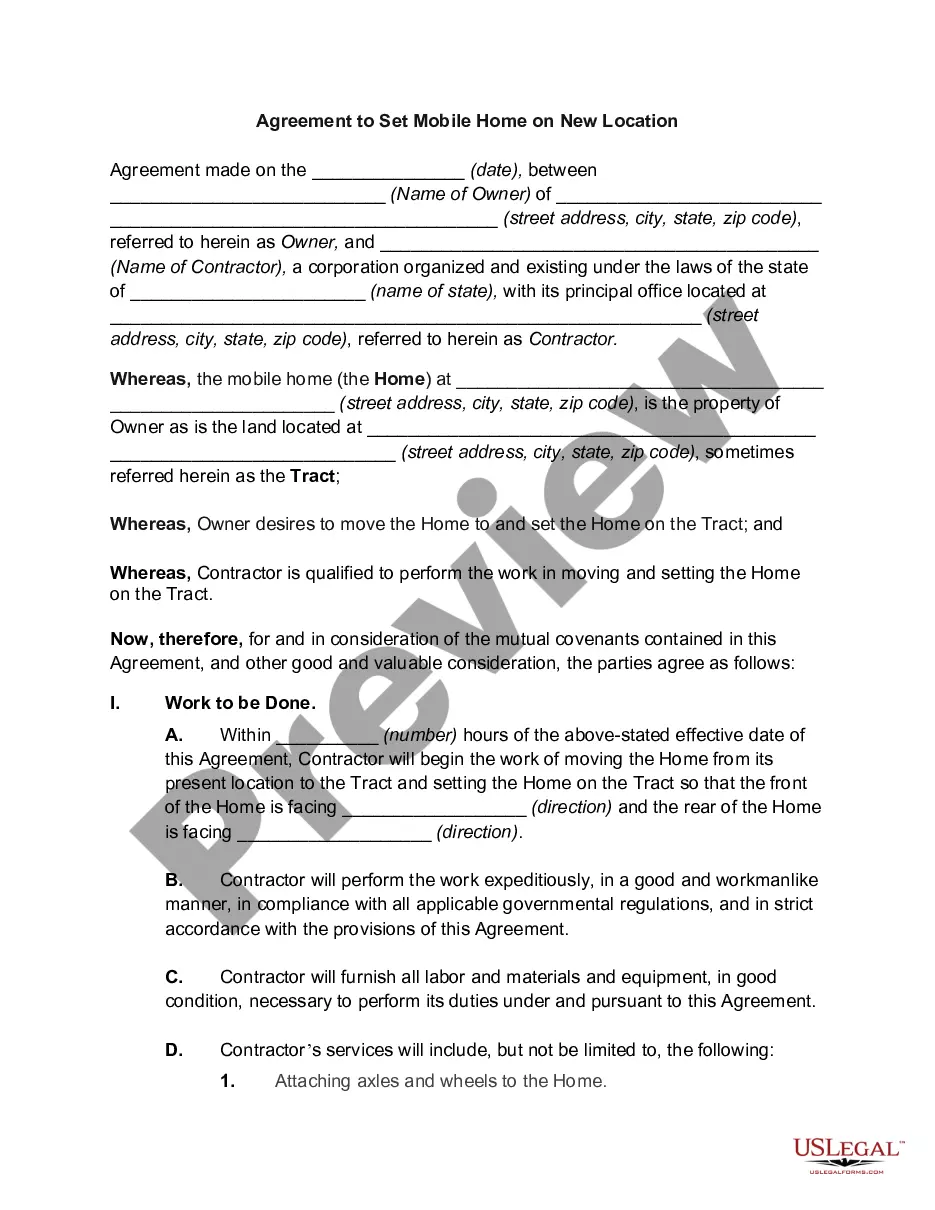

Description

How to fill out Collin Texas Amendment Of Restated Certificate Of Incorporation To Change Dividend Rate On $10.50 Cumulative Second Preferred Convertible Stock?

Creating legal forms is a must in today's world. Nevertheless, you don't always need to seek qualified assistance to draft some of them from scratch, including Collin Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock, with a service like US Legal Forms.

US Legal Forms has more than 85,000 forms to select from in various types ranging from living wills to real estate paperwork to divorce papers. All forms are organized according to their valid state, making the searching process less overwhelming. You can also find detailed resources and tutorials on the website to make any tasks related to document execution simple.

Here's how to find and download Collin Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock.

- Go over the document's preview and outline (if available) to get a basic idea of what you’ll get after getting the document.

- Ensure that the document of your choosing is specific to your state/county/area since state regulations can affect the legality of some documents.

- Examine the related forms or start the search over to locate the correct document.

- Hit Buy now and register your account. If you already have an existing one, choose to log in.

- Choose the pricing {plan, then a suitable payment gateway, and purchase Collin Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock.

- Choose to save the form template in any available file format.

- Go to the My Forms tab to re-download the document.

If you're already subscribed to US Legal Forms, you can locate the appropriate Collin Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock, log in to your account, and download it. Of course, our platform can’t take the place of a lawyer completely. If you have to deal with an exceptionally challenging situation, we recommend getting a lawyer to check your form before executing and filing it.

With over 25 years on the market, US Legal Forms became a go-to provider for many different legal forms for millions of users. Join them today and purchase your state-compliant documents effortlessly!