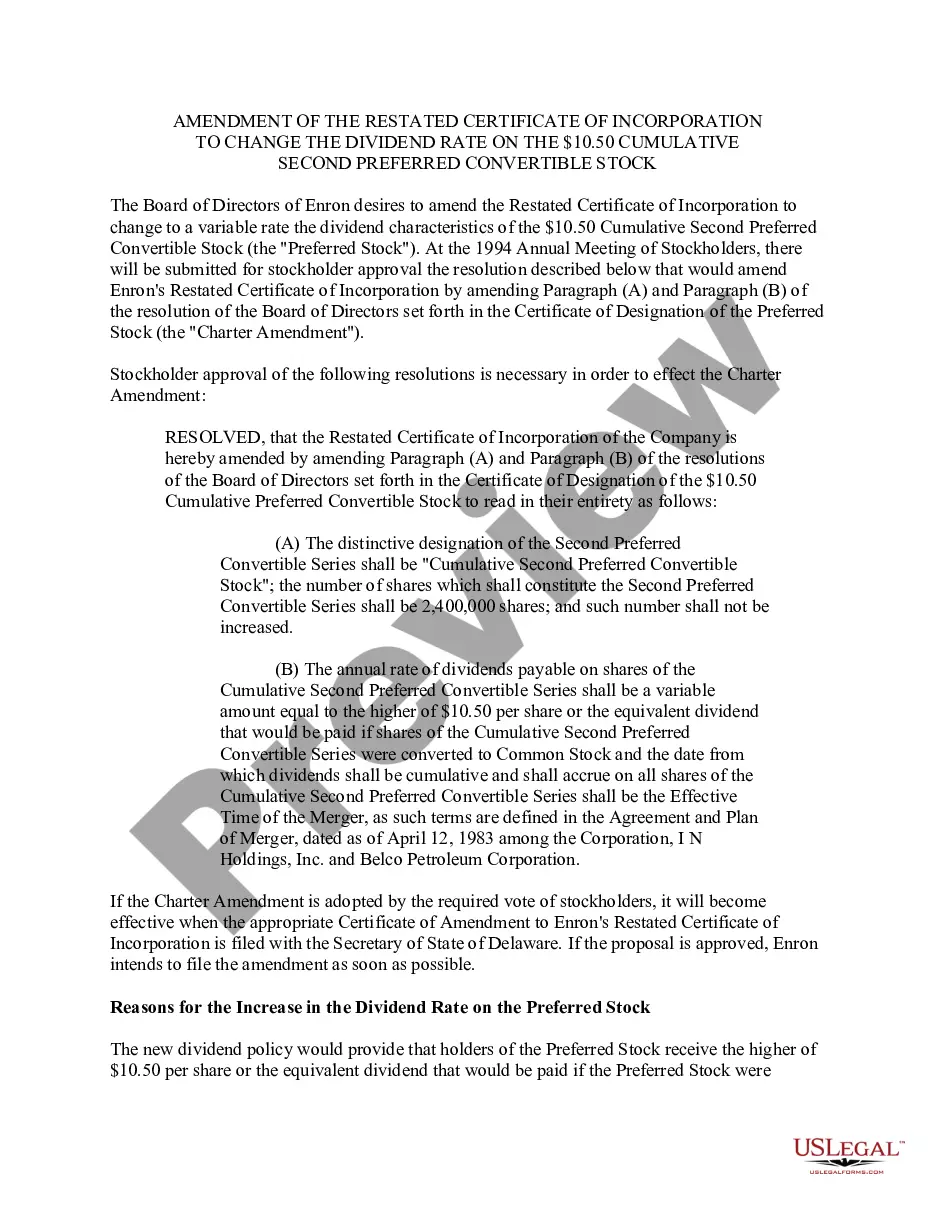

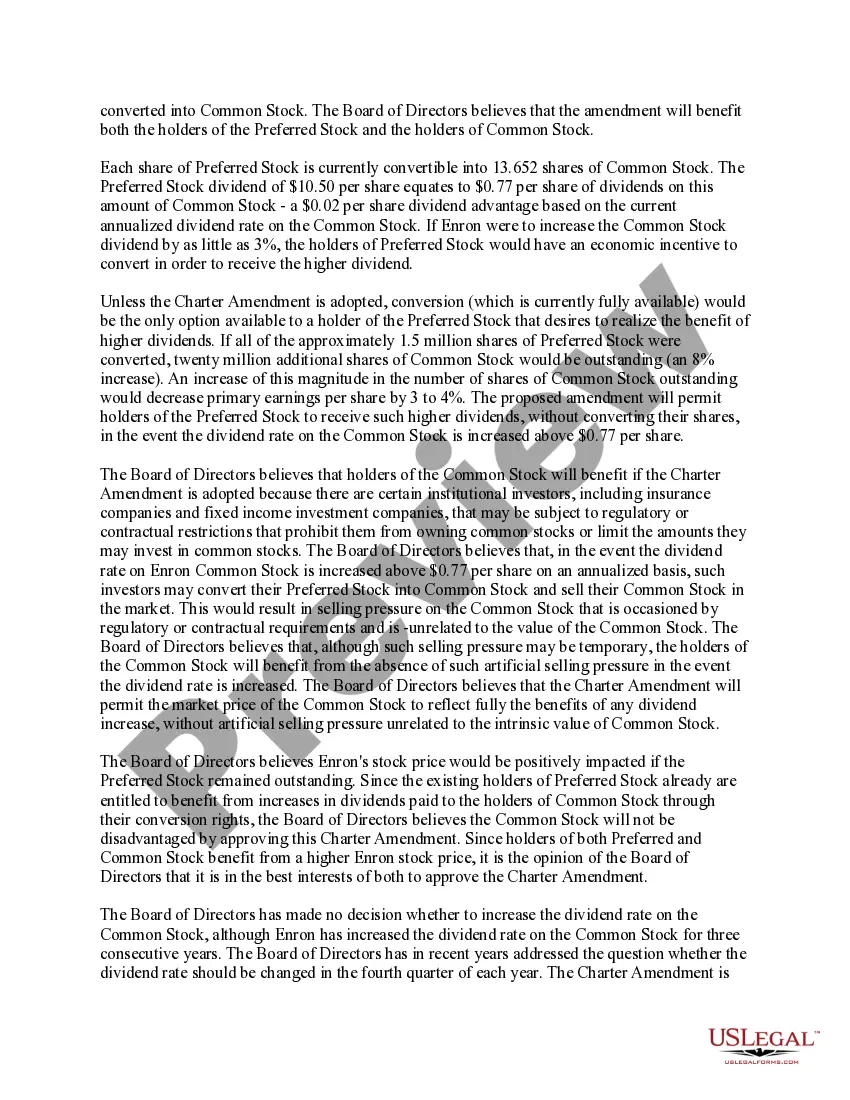

Fulton Georgia Amendment of Restated Certificate of Incorporation refers to the legal process of modifying the terms and provisions outlined in a company's certificate of incorporation in Fulton, Georgia. This particular amendment aims to alter the dividend rate on the $10.50 cumulative second preferred convertible stock. By changing this rate, the company seeks to adjust the amount it pays out to shareholders who hold this specific type of stock. The Fulton Georgia Amendment of Restated Certificate of Incorporation to change the dividend rate on $10.50 cumulative second preferred convertible stock is a vital step for the company's financial planning and capital structure. This amendment enables the company to maintain control over its cash flows and shareholder distributions, ensuring a fair return on investment for the preferred stockholders. This amendment, involving the $10.50 cumulative second preferred convertible stock, is specifically designed to modify the dividend rate associated with this particular class of shares. The company may have multiple classes of preferred stock, such as the $5.00 cumulative first preferred convertible stock or the $15.00 non-cumulative third preferred convertible stock. However, this amendment focuses solely on the $10.50 cumulative second preferred convertible stock, indicating its prominence and significance within the capital structure of the company. Key stakeholders impacted by this Fulton Georgia Amendment of Restated Certificate of Incorporation are the shareholders who hold the $10.50 cumulative second preferred convertible stock. By altering the dividend rate, their expected returns on investment will change, potentially influencing decisions around buying, selling, or holding these shares. Additionally, the company's overall financial stability and valuation may be affected by this amendment, as it directly impacts the distribution of profits to preferred stockholders. In summary, the Fulton Georgia Amendment of Restated Certificate of Incorporation to change the dividend rate on $10.50 cumulative second preferred convertible stock is a crucial step in maintaining the financial integrity and capital structure of the company. By making this amendment, the company can adjust the dividend payouts to preferred stockholders holding this specific class of shares. It is important to distinguish this amendment from others that may pertain to different classes of preferred stock, such as the $5.00 cumulative first preferred convertible stock or the $15.00 non-cumulative third preferred convertible stock.

Fulton Georgia Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock

Description

How to fill out Fulton Georgia Amendment Of Restated Certificate Of Incorporation To Change Dividend Rate On $10.50 Cumulative Second Preferred Convertible Stock?

Dealing with legal forms is a must in today's world. However, you don't always need to look for professional help to create some of them from scratch, including Fulton Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock, with a platform like US Legal Forms.

US Legal Forms has more than 85,000 templates to choose from in different categories ranging from living wills to real estate paperwork to divorce documents. All forms are arranged according to their valid state, making the searching process less frustrating. You can also find detailed materials and guides on the website to make any tasks related to document completion simple.

Here's how to find and download Fulton Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock.

- Go over the document's preview and outline (if available) to get a basic information on what you’ll get after getting the form.

- Ensure that the document of your choosing is specific to your state/county/area since state laws can affect the validity of some records.

- Check the similar forms or start the search over to locate the right document.

- Click Buy now and register your account. If you already have an existing one, select to log in.

- Choose the pricing {plan, then a suitable payment method, and purchase Fulton Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock.

- Select to save the form template in any available file format.

- Go to the My Forms tab to re-download the document.

If you're already subscribed to US Legal Forms, you can locate the appropriate Fulton Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock, log in to your account, and download it. Needless to say, our platform can’t replace a legal professional entirely. If you need to cope with an extremely complicated case, we advise getting an attorney to review your document before executing and filing it.

With more than 25 years on the market, US Legal Forms proved to be a go-to platform for many different legal forms for millions of customers. Become one of them today and get your state-specific documents with ease!

Form popularity

FAQ

Cumulative preferred stock is a type of preferred stock with a provision that stipulates that if any dividend payments have been missed in the past, the dividends owed must be paid out to cumulative preferred shareholders first.

A restated certificate of incorporation may omit (a) such provisions of the original certificate of incorporation which named the incorporator or incorporators, the initial board of directors and the original subscribers for shares, and (b) such provisions contained in any amendment to the certificate of incorporation

Restated Charter means the amended and restated certificate or articles of incorporation of the Company, as in effect at the time of determination, including any certificates of designation or articles of amendment.

Corporations that, in separate filings, have amended sections of the original Articles of Incorporation, can use the Restated Articles of Incorporation (Form DC-4) to restate the entire articles of incorporation so that there is only one document to reference in the future.

What is Cumulative Preferred Stock? Cumulative preferred stock is a class of shares wherein any unpaid or undeclared dividends for the current year must be accumulated and paid for in the future. However, such stocks are costlier, do not have voting rights, and cannot demand interim dividends.

?Amended? means ?changed?, i.e., that someone has revised the document. ?Restated? means ?presented in its entirety?, i.e., as a single, complete document. Accordingly, ?amended and restated? means a complete document into which one or more changes have been incorporated.

Preference dividends are cumulative in the sense that if they are not paid in one particular year, they will be carried forward as arrears and must be paid before dividends are given to common stockholders. In noncumulative preference dividends, if dividends are missed they are never paid.

When preferred stock is cumulative, preferred dividends not declared in a given period are called dividends in arrears. Dividends may be declared and paid in cash or stock. A debit balance in the Retained Earnings account is identified as a deficit. 11.

To the extent a dividend is not declared or set aside for a series of Preferred Stock for a designated quarterly dividend period, then the holder of such series of Preferred Stock will have no claim or right to such dividend payment in the future.

Related Definitions Restated Certificate of Incorporation means the certificate of incorporation of the Company, restated and filed pursuant to the Plan and including the Preferred Stock Certificate of Designation.