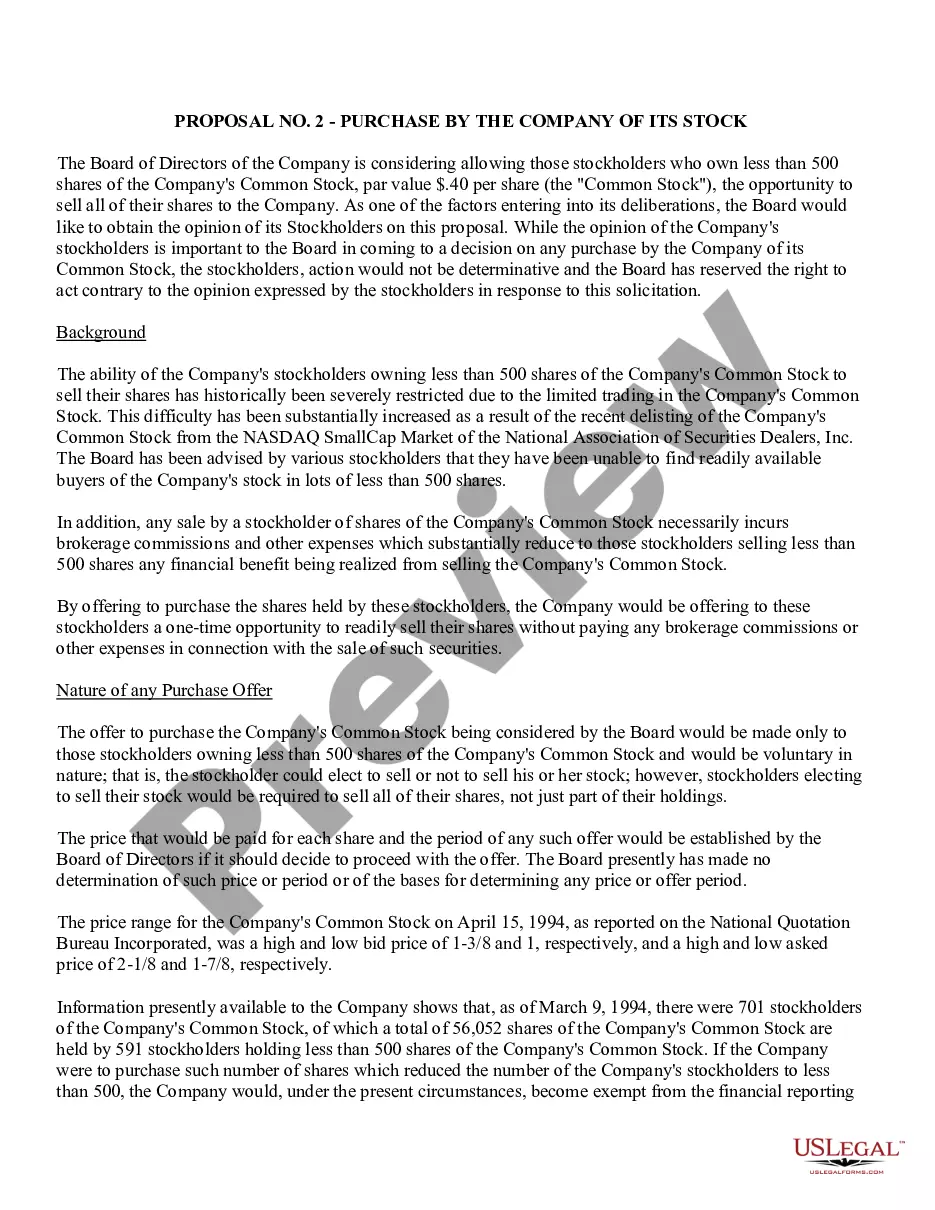

Queens New York Purchase of common stock for treasury of company

Description

How to fill out Purchase Of Common Stock For Treasury Of Company?

Are you seeking to swiftly draft a legally-binding Queens Purchase of common stock for the company's treasury or perhaps another document to manage your personal or business concerns.

You have two alternatives: engage a legal consultant to compose a legal document for you or entirely create it on your own. Fortunately, there's a different option - US Legal Forms.

If the form comes with a description, ensure to review what its intended purpose is.

If the form doesn’t meet your needs, initiate the search anew using the search bar located in the header. Choose the subscription that aligns best with your requirements and continue to the payment process. Choose the format you prefer for your document and download it. Print it, fill it out, and sign where indicated. If you have already set up an account, you can easily Log In to it, locate the Queens Purchase of common stock for the company's treasury template, and download it. To re-download the form, simply navigate to the My documents tab. It's simple to purchase and download legal documents when you use our services. Furthermore, the paperwork we provide is updated by legal professionals, which instills greater confidence when handling legal issues. Try US Legal Forms today and experience it for yourself!

- It will assist you in obtaining professionally drafted legal documents without incurring exorbitant fees for legal assistance.

- US Legal Forms offers a vast array of over 85,000 state-compliant document templates, including the Queens Purchase of common stock for the company's treasury and package forms.

- We supply templates for a variety of situations: from divorce documentation to real estate paperwork.

- We have been in business for more than 25 years and have established an impeccable reputation among our clientele.

- Here's how you can join them and acquire the necessary template without any unnecessary complications.

- First and foremost, verify if the Queens Purchase of common stock for the company's treasury is customized to conform to your state's or county's regulations.

Form popularity

FAQ

Treasury shares are included in the number reported for shares issued but are subtracted from issued shares to determine the number of outstanding shares. When treasury stock is sold, the accounts used to record the sale depend on whether the treasury stock was sold above or below the cost paid to purchase it.

What Happens to Treasury Stock? When a business buys back its own shares, these shares become treasury stock and are decommissioned. In and of itself, treasury stock doesn't have much value. These stocks do not have voting rights and do not pay any distributions.

Treasury stock is a contra equity account recorded in the shareholders' equity section of the balance sheet. Because treasury stock represents the number of shares repurchased from the open market, it reduces shareholders' equity by the amount paid for the stock.

The company can record the purchase of treasury stock with the journal entry of debiting the treasury stock account and crediting the cash account. In this journal entry, the par value or stated value of the stock, as well as the original issued price, is not included with recording the purchase of the treasury stock.

There are mainly two methods of accounting for treasury shares: the cost method and the par value method.

1 Accounting for the purchase of treasury stock. A reporting entity should recognize treasury stock based on the amount paid to repurchase its shares. It should be recorded as a reduction of stockholders' equity (i.e., as a contra-equity account).

Under the cost method of recording treasury stock, the cost of treasury stock is reported at the end of the Stockholders' Equity section of the balance sheet. Treasury stock will be a deduction from the amounts in Stockholders' Equity.

A company's own issued shares that it has repurchased but not cancelled. Shares can only be transferred into treasury where they have been purchased by a company from a shareholder out of distributable profits (section 724(1), Companies Act 2006).

When treasury stock is issued to pay all or a portion of a stock dividend, the dividend should be recorded at an amount equal to the fair value of the shares on the dividend declaration date. The reissuance of the treasury shares should be accounted for in the same manner as other reissuances of treasury stock.

Key Takeaways. Treasury stock is formerly outstanding stock that has been repurchased and is being held by the issuing company. Treasury stock reduces total shareholders' equity on a company's balance sheet, and it is therefore a contra equity account.