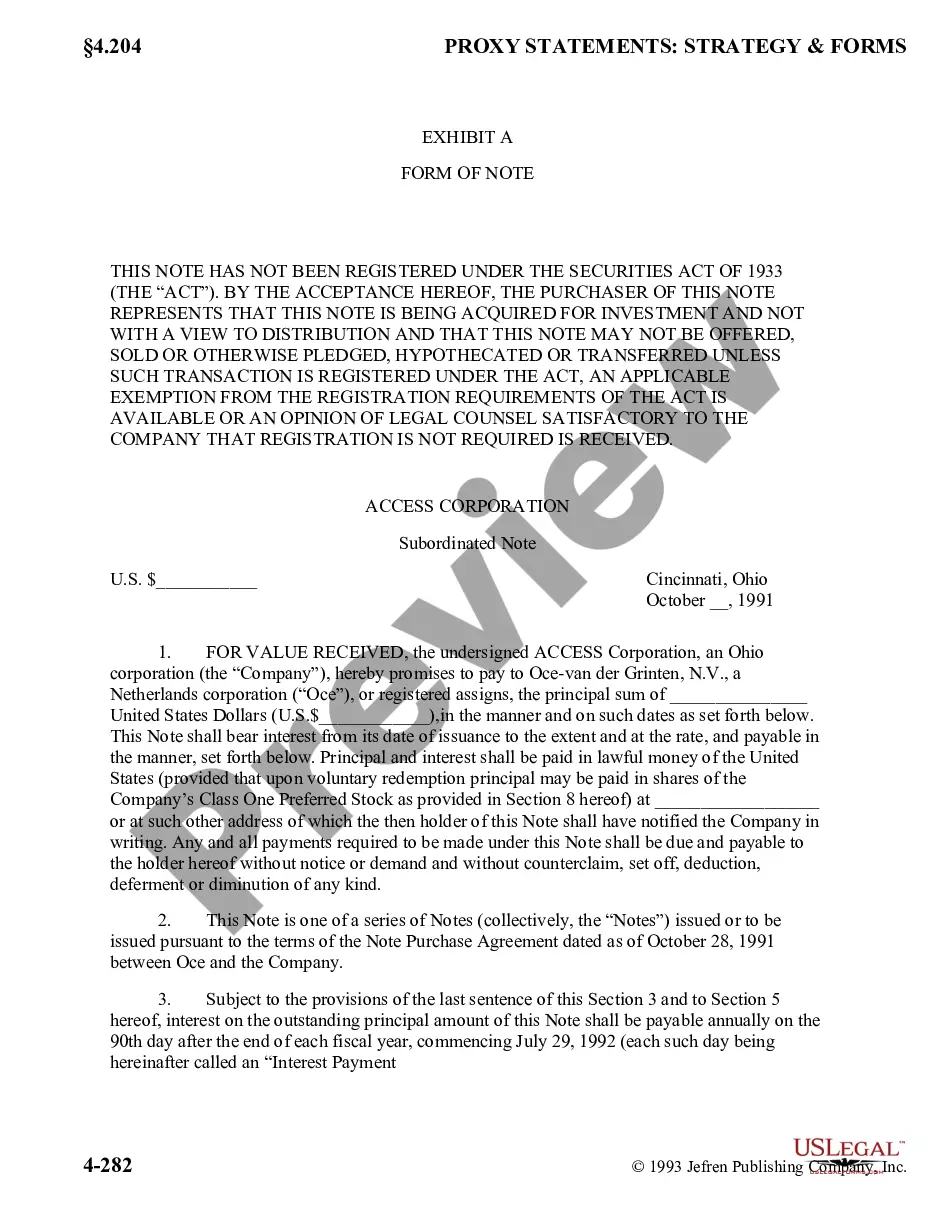

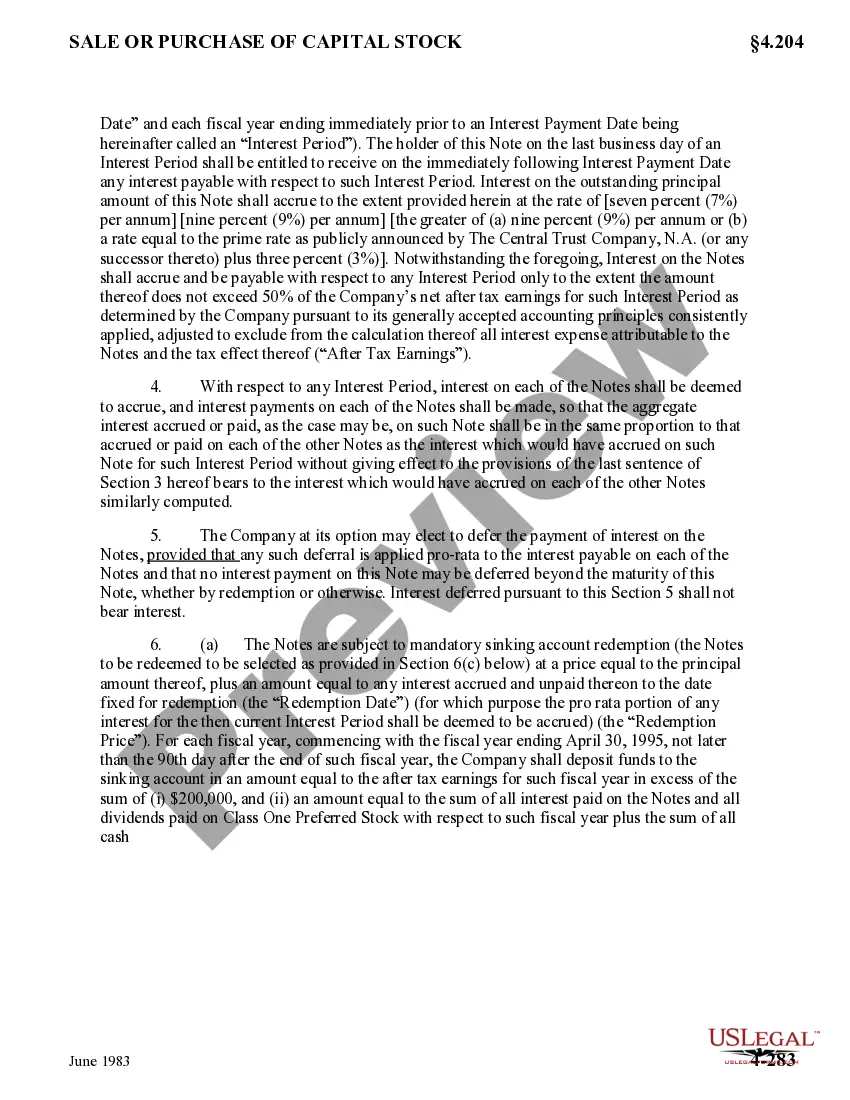

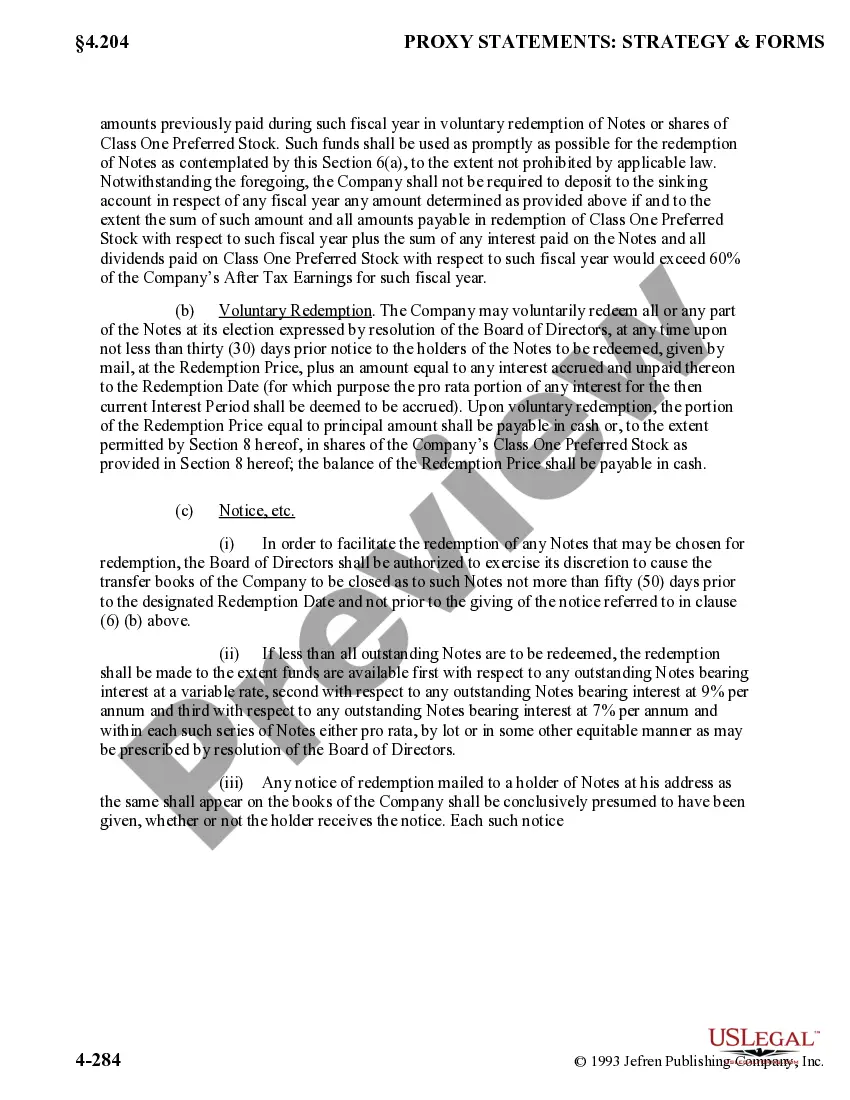

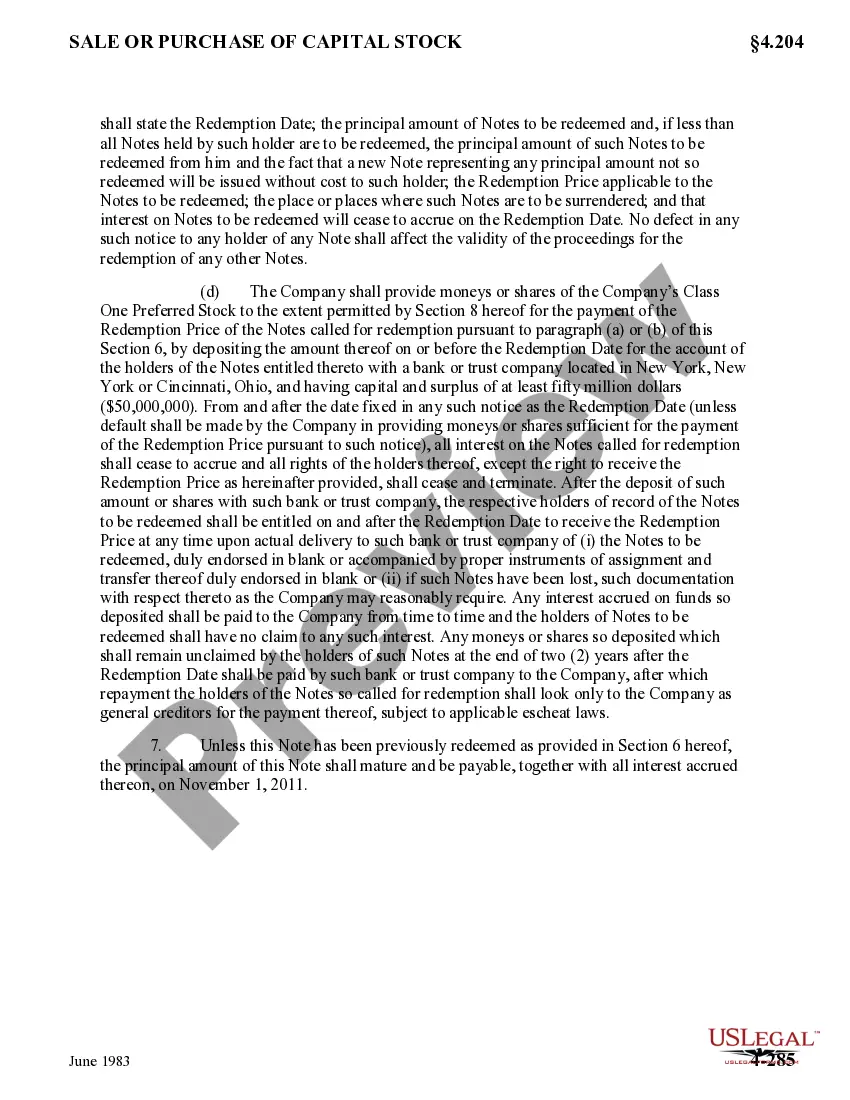

Suffolk New York Form of Note is a legal document used in the state of New York for various transactions involving the borrowing or lending of money. This written agreement outlines the responsibilities, terms, and conditions of the loan between the borrower and the lender. The Suffolk New York Form of Note provides a standardized format that ensures compliance with local laws and regulations. This form of note typically includes essential information such as the principal amount borrowed, the interest rate, the repayment terms, and any additional fees or charges associated with the loan. It also specifies the due date of repayment and the consequences of late or missed payments. Furthermore, the document may include provisions such as late fees, prepayment penalties, and default remedies. There are different types of Suffolk New York Forms of Note, each serving unique purposes based on the specific circumstances of the loan. Some common variations include: 1. Promissory Note: This is a standard form of note where the borrower promises to repay the borrowed money in a specified manner and timeframe. It includes information about the interest rate, payment schedule, and signatures of both parties. 2. Installment Note: This type of note outlines a loan that will be repaid in fixed, periodic payments over a specific time period. It typically includes details about the installment amounts, dates, and any interest that accrues during the repayment period. 3. Balloon Note: A balloon note is used when the borrower agrees to make regular payments for a specified time, but the remaining balance becomes due in full at the end of the term. This type of note often has a larger final payment, requiring careful planning by the borrower. 4. Adjustable-Rate Note: An adjustable-rate note features an interest rate that may change over time based on an identified financial index. This type of note provides flexibility, but borrowers should be aware of potential rate adjustments and their impact on future payments. 5. Interest-Only Note: In an interest-only note, the borrower is required to make regular payments that cover only the accrued interest on the loan. The principal balance remains unchanged until the end of the loan term, at which point it becomes due in full. When entering into a loan agreement in Suffolk, New York, it is crucial to utilize the appropriate Suffolk New York Form of Note that aligns with the specific loan terms and requirements. Using the correct form ensures legal compliance and helps to protect the rights and interests of both parties involved in the loan transaction.

Suffolk New York Form of Note

Description

How to fill out Suffolk New York Form Of Note?

Creating legal forms is a must in today's world. Nevertheless, you don't always need to look for professional help to create some of them from the ground up, including Suffolk Form of Note, with a platform like US Legal Forms.

US Legal Forms has over 85,000 forms to select from in different categories ranging from living wills to real estate papers to divorce papers. All forms are arranged based on their valid state, making the searching experience less challenging. You can also find information resources and tutorials on the website to make any tasks related to document execution straightforward.

Here's how to purchase and download Suffolk Form of Note.

- Take a look at the document's preview and description (if available) to get a basic information on what you’ll get after downloading the document.

- Ensure that the template of your choosing is adapted to your state/county/area since state regulations can affect the legality of some documents.

- Check the similar forms or start the search over to find the correct file.

- Hit Buy now and create your account. If you already have an existing one, choose to log in.

- Pick the option, then a needed payment gateway, and buy Suffolk Form of Note.

- Choose to save the form template in any available file format.

- Go to the My Forms tab to re-download the file.

If you're already subscribed to US Legal Forms, you can find the appropriate Suffolk Form of Note, log in to your account, and download it. Of course, our website can’t replace a legal professional entirely. If you need to cope with an exceptionally complicated situation, we advise using the services of a lawyer to review your form before signing and submitting it.

With more than 25 years on the market, US Legal Forms proved to be a go-to platform for many different legal forms for millions of customers. Join them today and purchase your state-specific documents with ease!