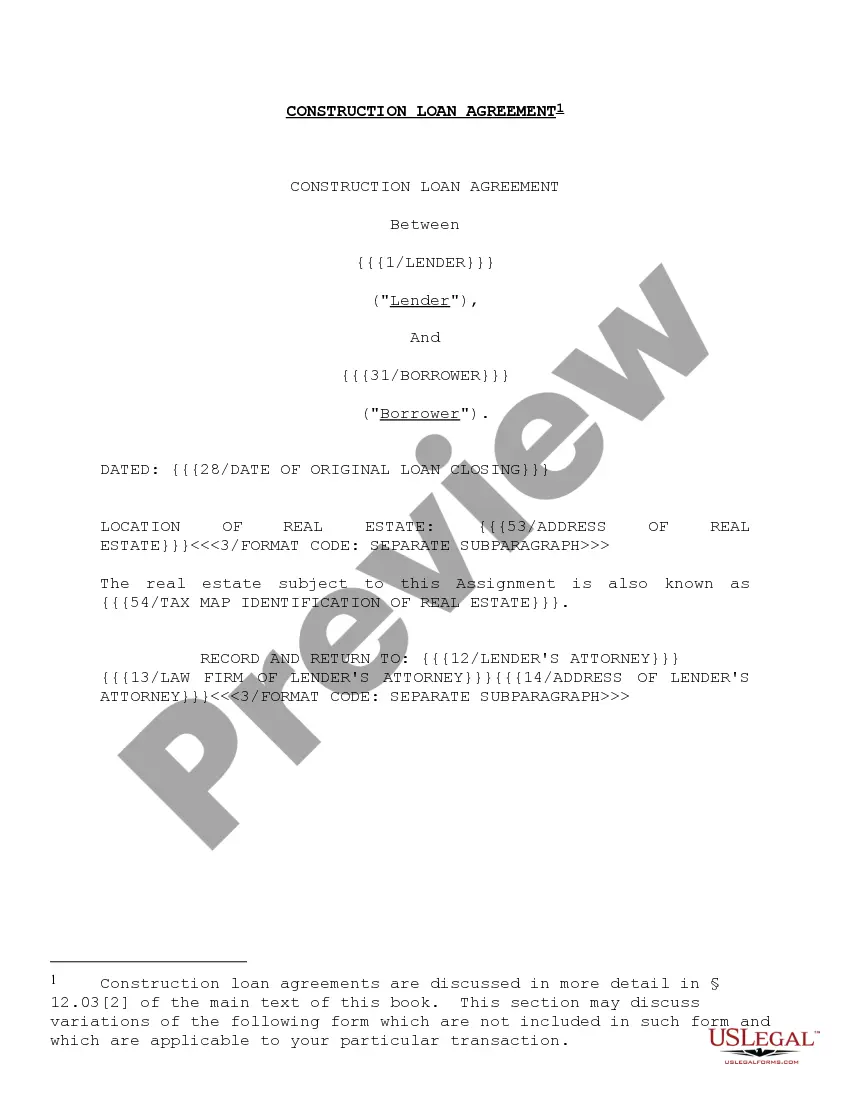

"Construction Loan Agreements and Variations" is a American Lawyer Media form. This form is to be used as a construction loan agreement.

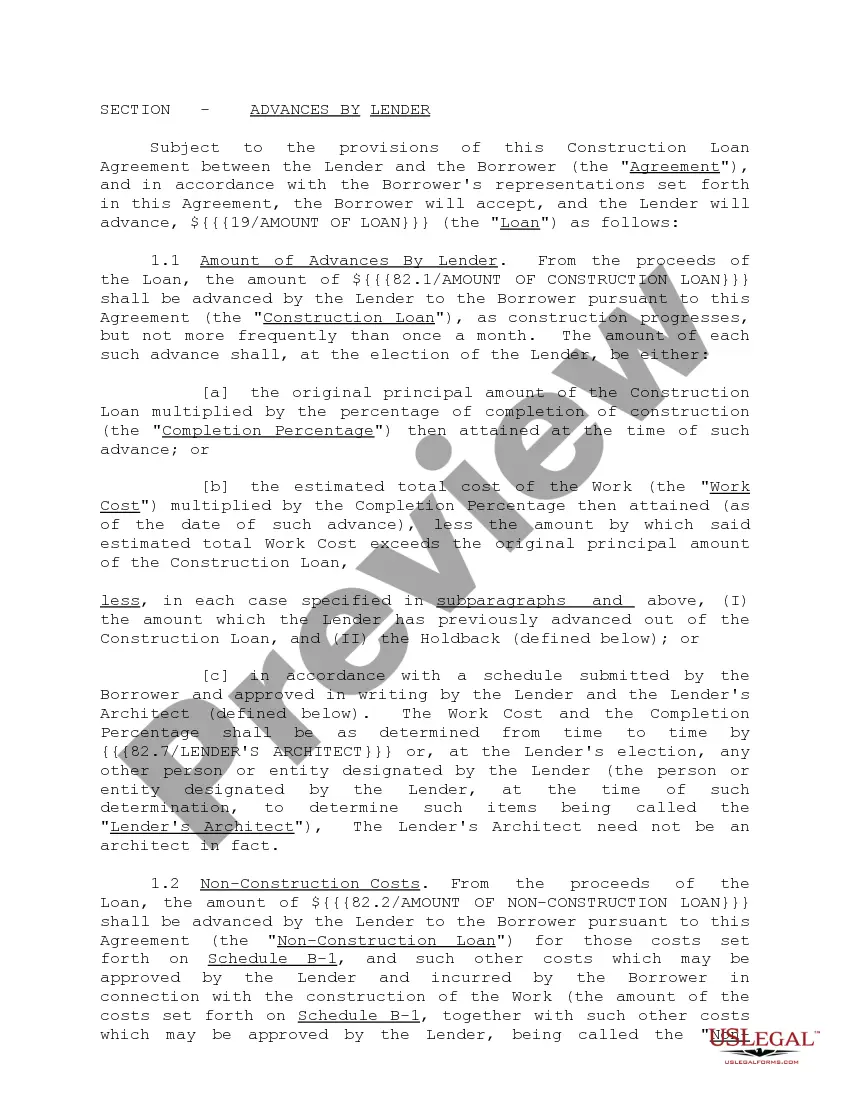

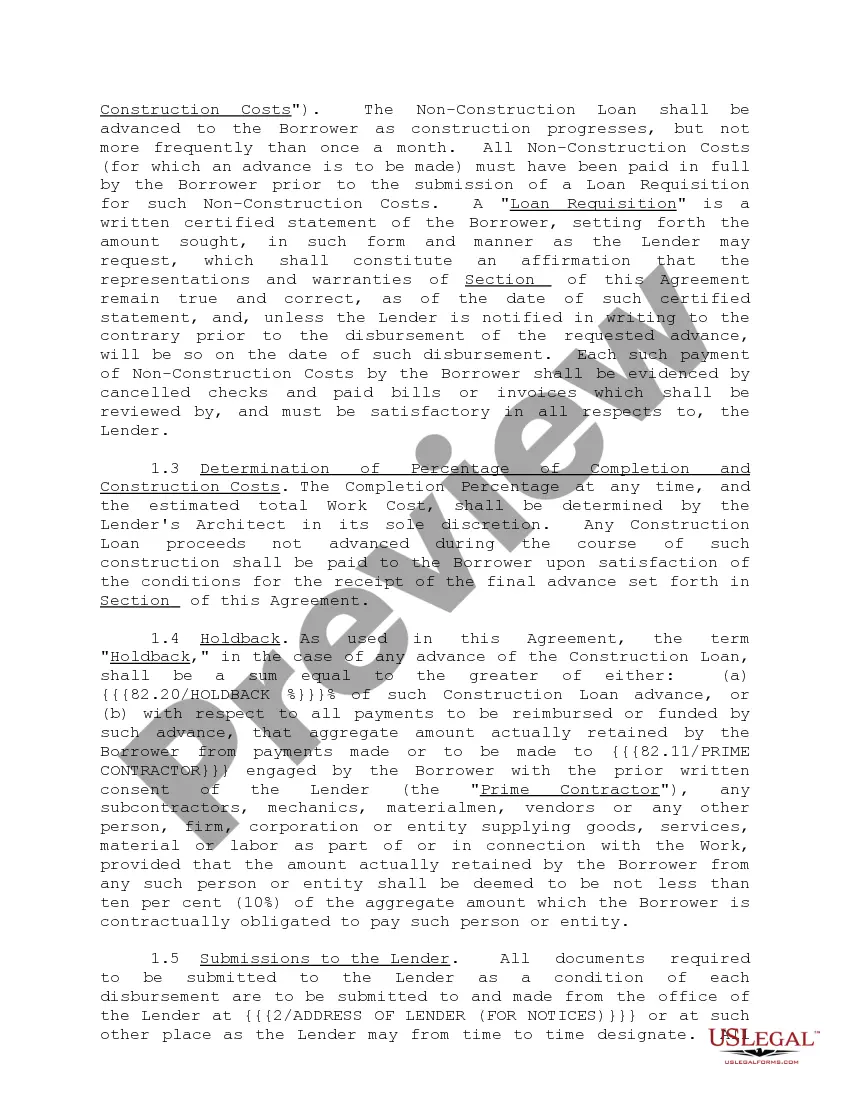

Contra Costa California Construction Loan Agreements and Variations serve as crucial legal documents that outline the terms and conditions between a lender and a borrower for financing construction projects in Contra Costa County, California. These agreements are specifically designed to address the unique risks and complexities associated with construction projects. Key Components of Contra Costa California Construction Loan Agreements: 1. Loan Amount and Disbursement: This section specifies the total loan amount and establishes the disbursement process, which typically follows pre-determined milestones or project completion stages. 2. Interest Rate and Payment Schedule: The agreement includes the interest rate charged on the loan and outlines the repayment schedule. Payments are usually structured to align with the project's progress. 3. Security and Collateral: Lenders require collateral to secure their investment. This section details the collateral, often the property or project being constructed, which protects the lender's interests in case of default. 4. Construction Draw Procedures: This section describes the process for obtaining construction draws, including the necessary documentation required to confirm project completion and disburse funds accordingly. 5. Construction Budget and Cost Overruns: The agreement sets a construction budget, outlining the estimated costs and contingencies. It may also include provisions for handling cost overruns, change orders, and unexpected expenses during the construction phase. 6. Builder's Risk and Insurance: Builders are responsible for obtaining insurance coverage to protect against potential damages or losses during construction. The agreement outlines the required insurance coverage and the lender's inclusion as a loss payee. 7. Project Completion and Final Payment: This section establishes the criteria and procedures for determining project completion, including a walkthrough, third-party inspections, and the release of final payment. Variations of Contra Costa California Construction Loan Agreements: 1. Traditional Construction Loan Agreements: These agreements follow the standard structure mentioned above. 2. Renovation or Remodeling Construction Loan Agreements: Specifically tailored for renovation or remodeling projects, these agreements include additional provisions addressing the unique requirements and challenges associated with such projects. 3. Fix and Flip Construction Loan Agreements: These agreements cater to real estate investors who purchase distressed properties, fix them up, and sell them quickly. They encompass specific terms related to the investment strategy, timeline, and potential profit sharing between the lender and borrower. 4. Owner-Builder Construction Loan Agreements: These agreements are designed for individuals who plan to act as their own general contractors or oversee the construction process personally. They may require additional documentation, such as proof of qualifications or experience in managing construction projects. In conclusion, Contra Costa California Construction Loan Agreements and Variations establish clear guidelines, responsibilities, and provisions to protect both lenders and borrowers throughout the construction process. The specific type of agreement chosen depends on the project's nature and the parties involved.