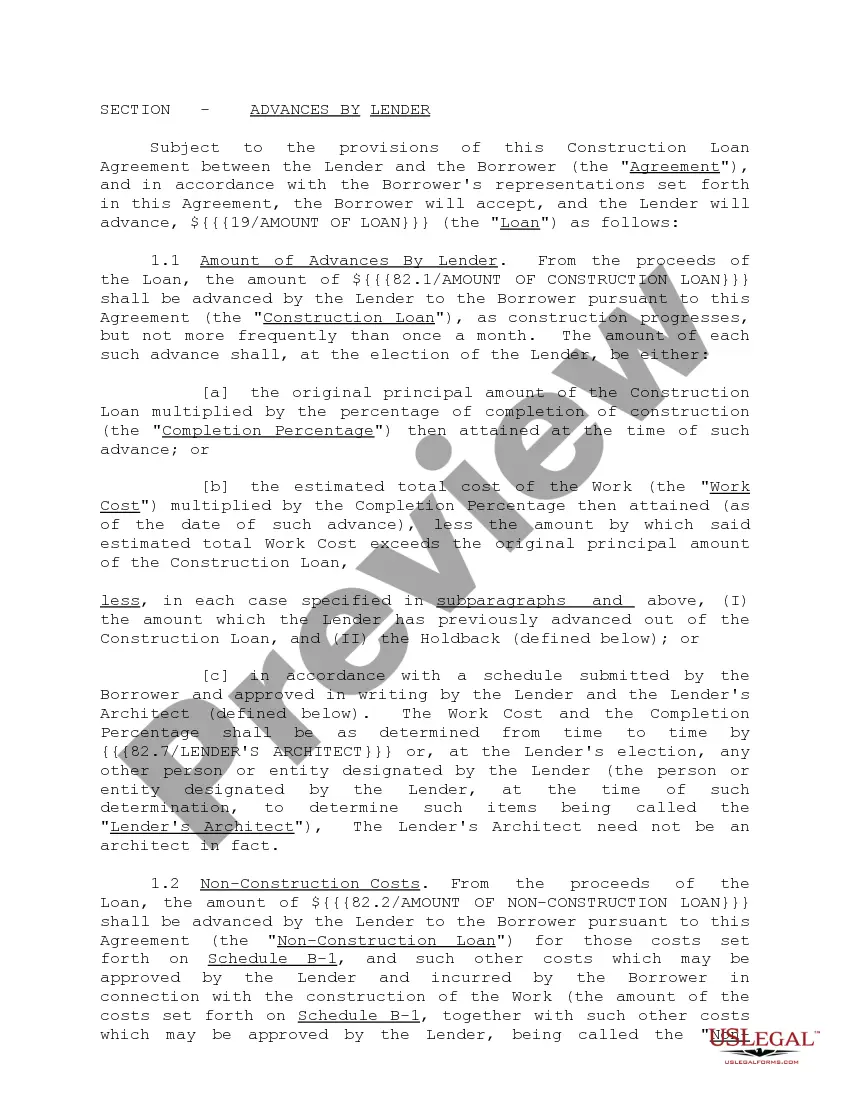

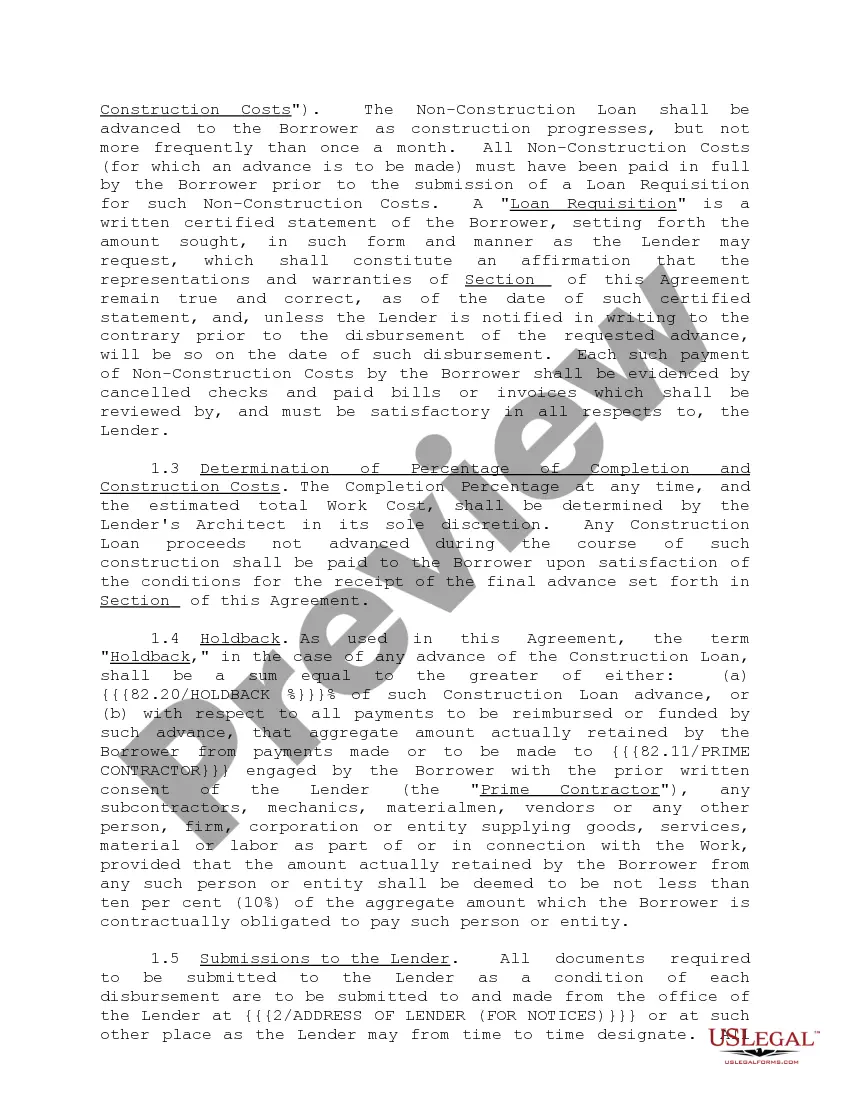

"Construction Loan Agreements and Variations" is a American Lawyer Media form. This form is to be used as a construction loan agreement.

Franklin Ohio Construction Loan Agreements and Variations, also known as construction mortgage agreements, are legal contracts designed to provide financing for construction projects in Franklin, Ohio. These agreements outline the terms and conditions under which the lender provides funds to the borrower for the purpose of financing the construction or renovation of a property. They are critical in ensuring proper funding and management throughout the construction project. There are several variations of construction loan agreements commonly used in Franklin, Ohio. Some of these variations include: 1. Construction-to-Permanent Loan Agreement: This type of agreement combines both the construction financing and the permanent mortgage into a single loan. It allows the borrower to secure long-term financing for the property once construction is complete. 2. Construction-Only Loan Agreement: In this type of agreement, the lender provides funds solely for the construction phase of the project. Once construction is finished, the borrower must secure permanent financing separately. 3. Single-Close Construction Loan Agreement: This agreement enables borrowers to combine both the construction financing and the permanent mortgage without the need for two separate loan applications or closings. It provides convenience and potentially cost savings for the borrower. The Franklin Ohio Construction Loan Agreements and their variations typically cover various aspects of the construction project, including the loan amount, interest rate, repayment terms, construction timeline, payment schedule, inspection requirements, and disbursement procedures. These agreements often outline the responsibilities of both the borrower and the lender, ensuring that the construction project progresses smoothly and without unnecessary delays. When applying for a Franklin Ohio Construction Loan Agreement, it is crucial for borrowers to provide detailed and accurate information about the proposed construction project, including architectural plans, construction estimates, permits, and any other relevant documents. Lenders will assess the feasibility and potential risks associated with the project before approving the loan. Before entering into a construction loan agreement, borrowers should carefully review the terms and conditions, seeking professional legal advice if necessary. It is essential to understand the interest rates, repayment terms, potential penalties for delays or defaults, and any other provisions that may affect the project. By doing so, borrowers can ensure that the loan agreement aligns with their construction timeline, budget, and long-term goals. In summary, Franklin Ohio Construction Loan Agreements and Variations enable borrowers to secure the necessary funds for construction projects while providing lenders with the assurance and security needed to protect their investment. By understanding the different types of agreements and carefully reviewing the terms, borrowers can navigate the construction financing process effectively and ensure the successful completion of their projects.Franklin Ohio Construction Loan Agreements and Variations, also known as construction mortgage agreements, are legal contracts designed to provide financing for construction projects in Franklin, Ohio. These agreements outline the terms and conditions under which the lender provides funds to the borrower for the purpose of financing the construction or renovation of a property. They are critical in ensuring proper funding and management throughout the construction project. There are several variations of construction loan agreements commonly used in Franklin, Ohio. Some of these variations include: 1. Construction-to-Permanent Loan Agreement: This type of agreement combines both the construction financing and the permanent mortgage into a single loan. It allows the borrower to secure long-term financing for the property once construction is complete. 2. Construction-Only Loan Agreement: In this type of agreement, the lender provides funds solely for the construction phase of the project. Once construction is finished, the borrower must secure permanent financing separately. 3. Single-Close Construction Loan Agreement: This agreement enables borrowers to combine both the construction financing and the permanent mortgage without the need for two separate loan applications or closings. It provides convenience and potentially cost savings for the borrower. The Franklin Ohio Construction Loan Agreements and their variations typically cover various aspects of the construction project, including the loan amount, interest rate, repayment terms, construction timeline, payment schedule, inspection requirements, and disbursement procedures. These agreements often outline the responsibilities of both the borrower and the lender, ensuring that the construction project progresses smoothly and without unnecessary delays. When applying for a Franklin Ohio Construction Loan Agreement, it is crucial for borrowers to provide detailed and accurate information about the proposed construction project, including architectural plans, construction estimates, permits, and any other relevant documents. Lenders will assess the feasibility and potential risks associated with the project before approving the loan. Before entering into a construction loan agreement, borrowers should carefully review the terms and conditions, seeking professional legal advice if necessary. It is essential to understand the interest rates, repayment terms, potential penalties for delays or defaults, and any other provisions that may affect the project. By doing so, borrowers can ensure that the loan agreement aligns with their construction timeline, budget, and long-term goals. In summary, Franklin Ohio Construction Loan Agreements and Variations enable borrowers to secure the necessary funds for construction projects while providing lenders with the assurance and security needed to protect their investment. By understanding the different types of agreements and carefully reviewing the terms, borrowers can navigate the construction financing process effectively and ensure the successful completion of their projects.