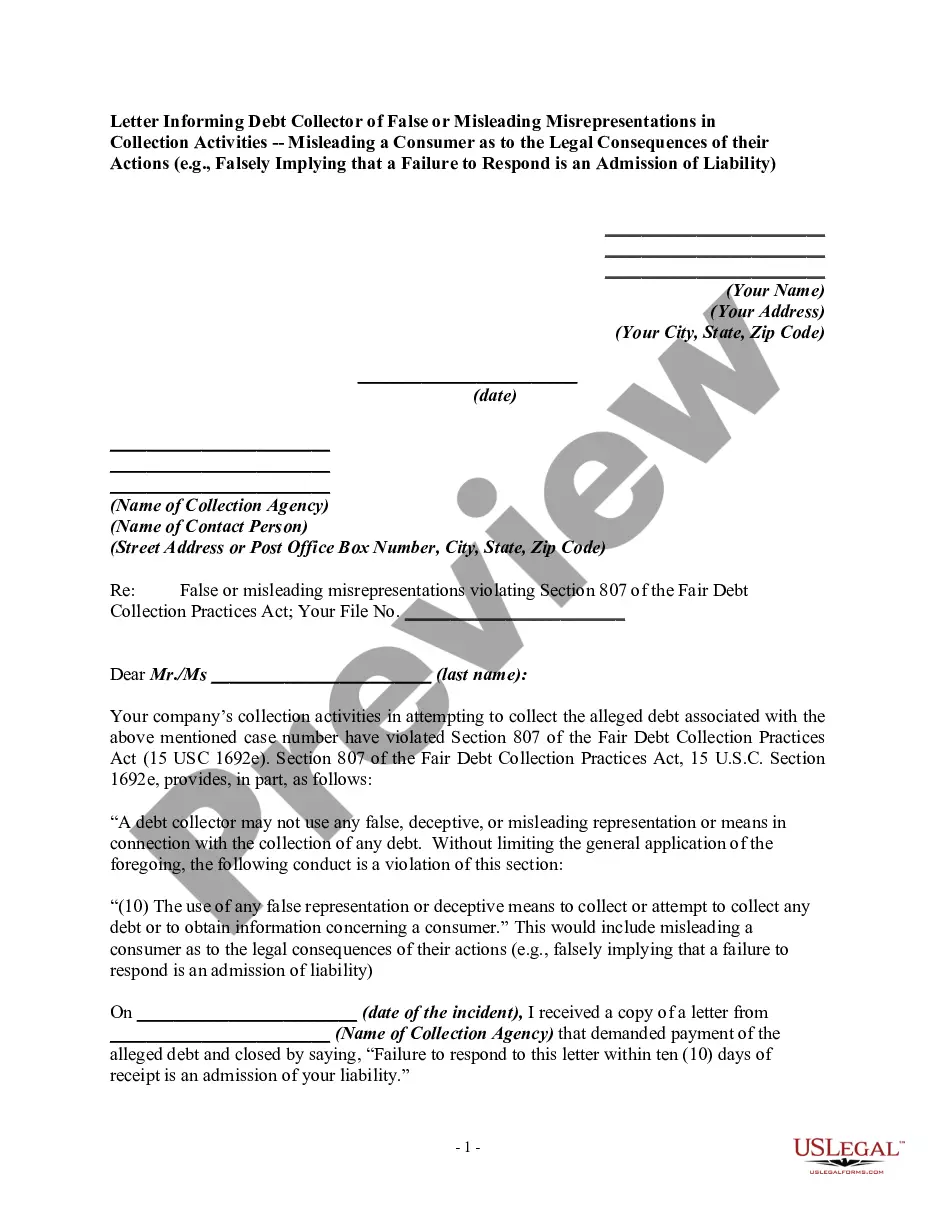

Section 807 of the Fair Debt Collection Practices Act, 15 U.S.C. Section 1692e, provides, in part, as follows: "A debt collector may not use any false, deceptive, or misleading representation or means in connection with the collection of any debt. Without limiting the general application of the foregoing, the following conduct is a violation of this section:

"(10) The use of any false representation or deceptive means to collect or attempt to collect any debt or to obtain information concerning a consumer."

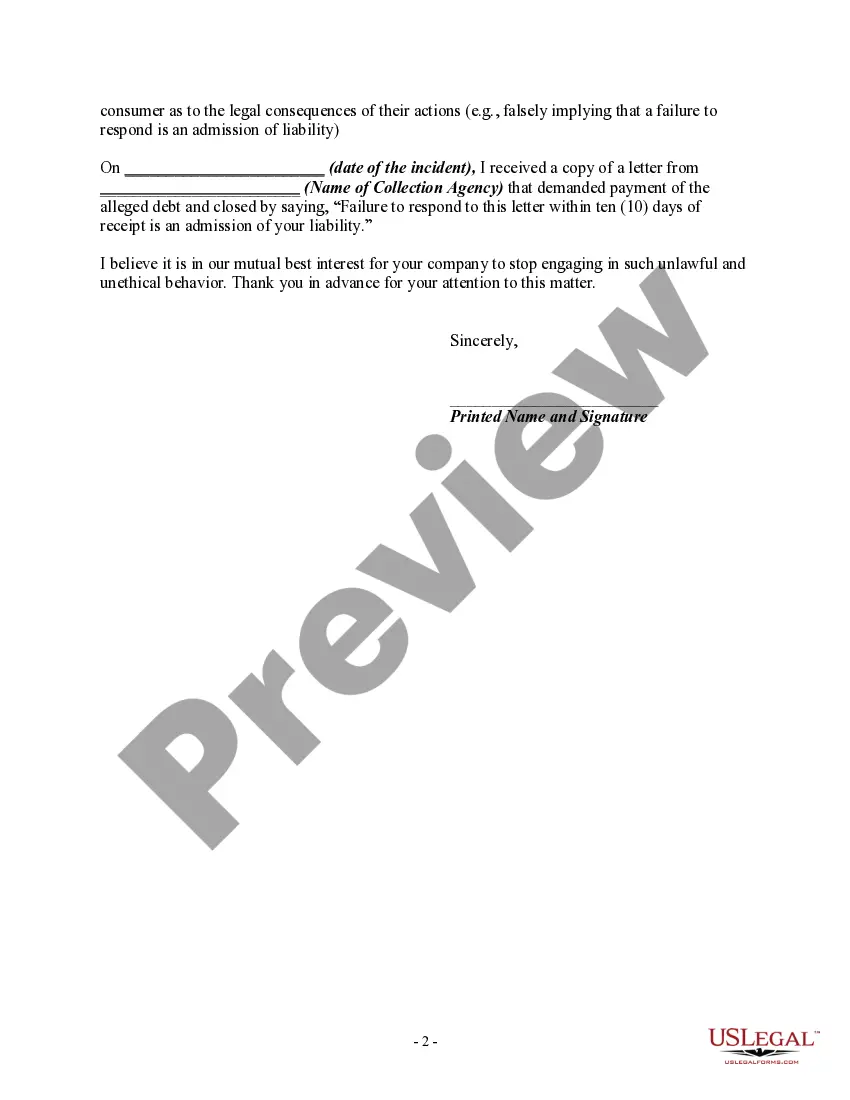

This would include misleading a consumer as to the legal consequences of their actions (e.g., falsely implying that a failure to respond is an admission of liability).

Title: Protecting Consumers' Rights: Maricopa Arizona Letters Exposing Misleading Debt Collection Practices Introduction: In Maricopa, Arizona, consumers are protected by extensive regulations against deceptive debt collection practices. One common tactic used by debt collectors is misleading consumers regarding the legal consequences of their actions. This includes falsely implying that a failure to respond to a debt collection notice is an admission of liability. To combat such practices, consumers can choose from different types of letters to inform debt collectors about these misleading misrepresentations. This article provides a detailed description of various Maricopa Arizona Letter Informing Debt Collector of False or Misleading Misrepresentations in Collection Activities. 1. Maricopa Arizona Letter Type 1: Disputing Misleading Representations This letter aims to explicitly dispute the debt collector's false or misleading statements regarding liability. It may address instances where collectors imply that a consumer's lack of response constitutes an acknowledgment of debt. By clearly stating that no admission of liability is implied or intended, consumers can assert their rights and ensure truthful representations. 2. Maricopa Arizona Letter Type 2: Requesting Clarification of Legal Consequences This letter seeks to challenge debt collectors' assertions by requesting a detailed explanation of the legal consequences associated with a consumer's failure to respond. The letter may highlight the collector's potential violation of the Fair Debt Collection Practices Act (FD CPA) by failing to provide accurate and complete information about the legal implications of inaction. 3. Maricopa Arizona Letter Type 3: Notifying Authorities of Deceptive Practices In cases of ongoing, persistent false representations, consumers can consider sending a letter informing relevant authorities, such as the Maricopa Attorney General's office or the Consumer Financial Protection Bureau (CFPB). This letter would detail the debt collector's misleading tactics, providing evidence to support the claim of deceptive practices. 4. Maricopa Arizona Letter Type 4: Demanding Immediate Cease and Desist In situations where prior communications with the debt collector have failed to rectify the misleading misrepresentations, consumers can send a cease and desist letter. This letter warns the collector that further deceptive actions will result in legal action being pursued. It emphasizes the consumer's rights under the FD CPA and the potential consequences for continued violations. Conclusion: Maricopa, Arizona provides consumers with effective strategies to address false or misleading debt collection practices. By utilizing different types of letters, individuals can assert their rights, dispute misleading representations, and demand accurate information regarding the legal consequences of their actions. These letters serve as a tool for protecting consumers from unjust harassment and deception, ensuring fair debt collection practices.Title: Protecting Consumers' Rights: Maricopa Arizona Letters Exposing Misleading Debt Collection Practices Introduction: In Maricopa, Arizona, consumers are protected by extensive regulations against deceptive debt collection practices. One common tactic used by debt collectors is misleading consumers regarding the legal consequences of their actions. This includes falsely implying that a failure to respond to a debt collection notice is an admission of liability. To combat such practices, consumers can choose from different types of letters to inform debt collectors about these misleading misrepresentations. This article provides a detailed description of various Maricopa Arizona Letter Informing Debt Collector of False or Misleading Misrepresentations in Collection Activities. 1. Maricopa Arizona Letter Type 1: Disputing Misleading Representations This letter aims to explicitly dispute the debt collector's false or misleading statements regarding liability. It may address instances where collectors imply that a consumer's lack of response constitutes an acknowledgment of debt. By clearly stating that no admission of liability is implied or intended, consumers can assert their rights and ensure truthful representations. 2. Maricopa Arizona Letter Type 2: Requesting Clarification of Legal Consequences This letter seeks to challenge debt collectors' assertions by requesting a detailed explanation of the legal consequences associated with a consumer's failure to respond. The letter may highlight the collector's potential violation of the Fair Debt Collection Practices Act (FD CPA) by failing to provide accurate and complete information about the legal implications of inaction. 3. Maricopa Arizona Letter Type 3: Notifying Authorities of Deceptive Practices In cases of ongoing, persistent false representations, consumers can consider sending a letter informing relevant authorities, such as the Maricopa Attorney General's office or the Consumer Financial Protection Bureau (CFPB). This letter would detail the debt collector's misleading tactics, providing evidence to support the claim of deceptive practices. 4. Maricopa Arizona Letter Type 4: Demanding Immediate Cease and Desist In situations where prior communications with the debt collector have failed to rectify the misleading misrepresentations, consumers can send a cease and desist letter. This letter warns the collector that further deceptive actions will result in legal action being pursued. It emphasizes the consumer's rights under the FD CPA and the potential consequences for continued violations. Conclusion: Maricopa, Arizona provides consumers with effective strategies to address false or misleading debt collection practices. By utilizing different types of letters, individuals can assert their rights, dispute misleading representations, and demand accurate information regarding the legal consequences of their actions. These letters serve as a tool for protecting consumers from unjust harassment and deception, ensuring fair debt collection practices.