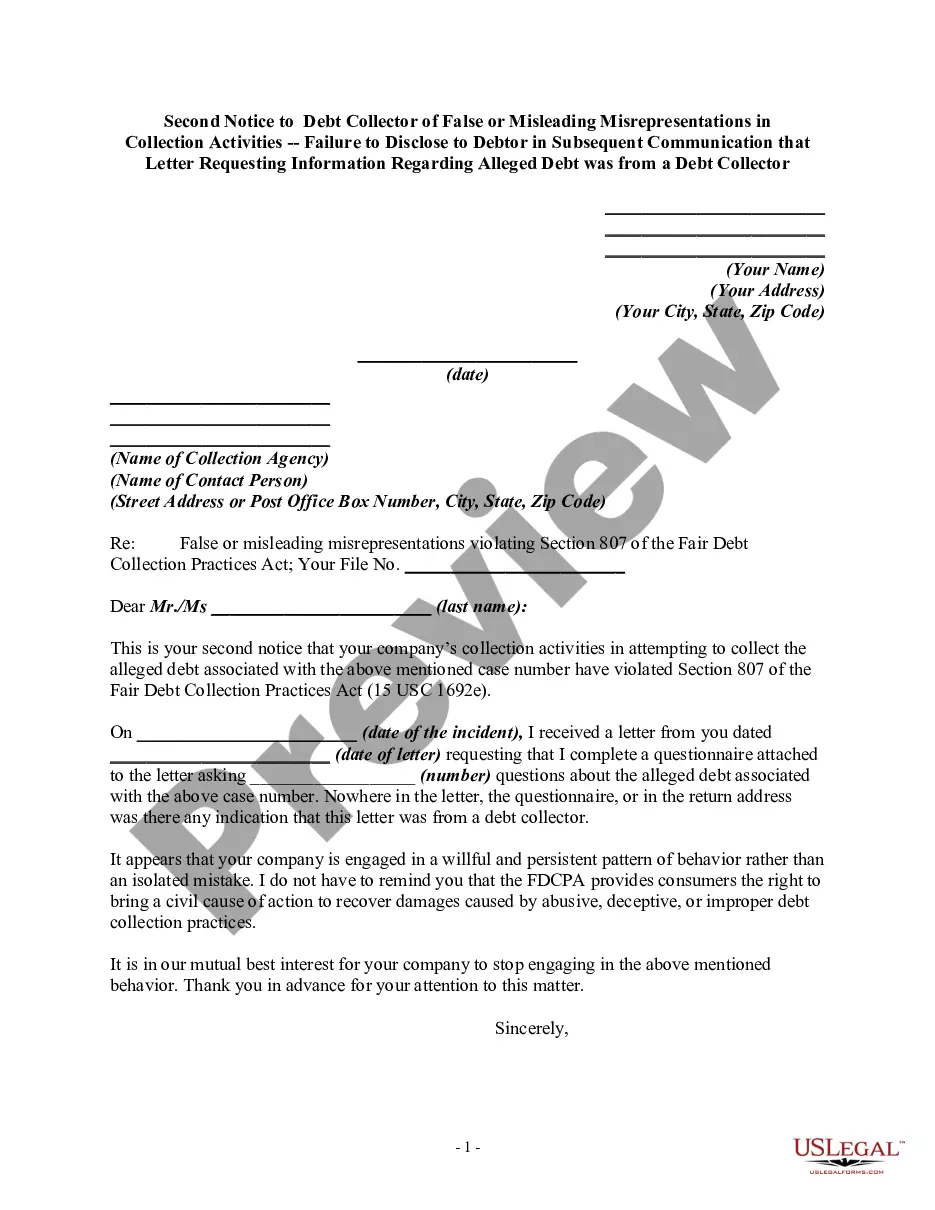

Section 807 of the Fair Debt Collection Practices Act, 15 U.S.C. Sec. 1692e, provides, in part, as follows:

A debt collector may not use any false, deceptive, or misleading representation or means in connection with the collection of any debt. Without limiting the general application of the foregoing, the following conduct is a violation of this section:

"11) The failure to disclose in the initial written communication with the consumer and, in addition, if the initial communication with the consumer is oral, in that initial oral communication, that the debt collector is attempting to collect a debt and that any information obtained will be used for that purpose, and the failure to disclose in subsequent communications that the communication is from a debt collector . . . ."

Cook Illinois Second Notice to Debt Collector of False or Misleading Misrepresentations in Collection Activities — Failure to Disclose to Debtor in Subsequent Communication that Letter Requesting Information Regarding Alleged Debt was from a Debt Collector is a legal document designed to address any false or misleading statements made by a debt collector during the collection process. This notice is crucial in maintaining transparency and protecting the rights of debtors. In situations where a debt collector has sent a letter requesting information regarding an alleged debt without disclosing their status as a debt collector, this second notice becomes necessary. It aims to rectify the previous misrepresentation and ensure that all subsequent communication rightly identifies the sender as a debt collector. By failing to disclose their identity as a debt collector in subsequent communication, the debt collector may further mislead the debtor and disregard the legal obligations set forth by the Fair Debt Collection Practices Act (FD CPA). This act governs debt collection activities and emphasizes the importance of honesty, fairness, and transparency in the interactions between debt collectors and debtors. Some examples of misleading misrepresentations in collection activities that may require a Cook Illinois Second Notice include: 1. False claims or misleading statements regarding the nature or amount of the debt. 2. Misrepresentation of the debt collector's legal authority to collect the debt. 3. Failure to disclose the debtor's rights, such as the right to dispute the debt or request verification. 4. Deceptive tactics or intimidation to coerce payment. 5. Falsely implying that non-payment will result in legal consequences or damage to the debtor's credit score. The Cook Illinois Second Notice serves as an official written warning to the debt collector, urging them to rectify their previous misrepresentation and comply with the legally mandated disclosure requirements. It allows the debtor to assert their rights, request accurate information regarding the alleged debt, and seek appropriate remedies if the debt collector fails to comply. In conclusion, the Cook Illinois Second Notice to Debt Collector of False or Misleading Misrepresentations in Collection Activities — Failure to Disclose to Debtor in Subsequent Communication that Letter Requesting Information Regarding Alleged Debt was from a Debt Collector is a vital legal document that ensures transparency, fairness, and adherence to the law in debt collection processes. By providing debtors with the means to address false or misleading statements made by debt collectors, it helps protect their rights and promote ethical debt collection practices.