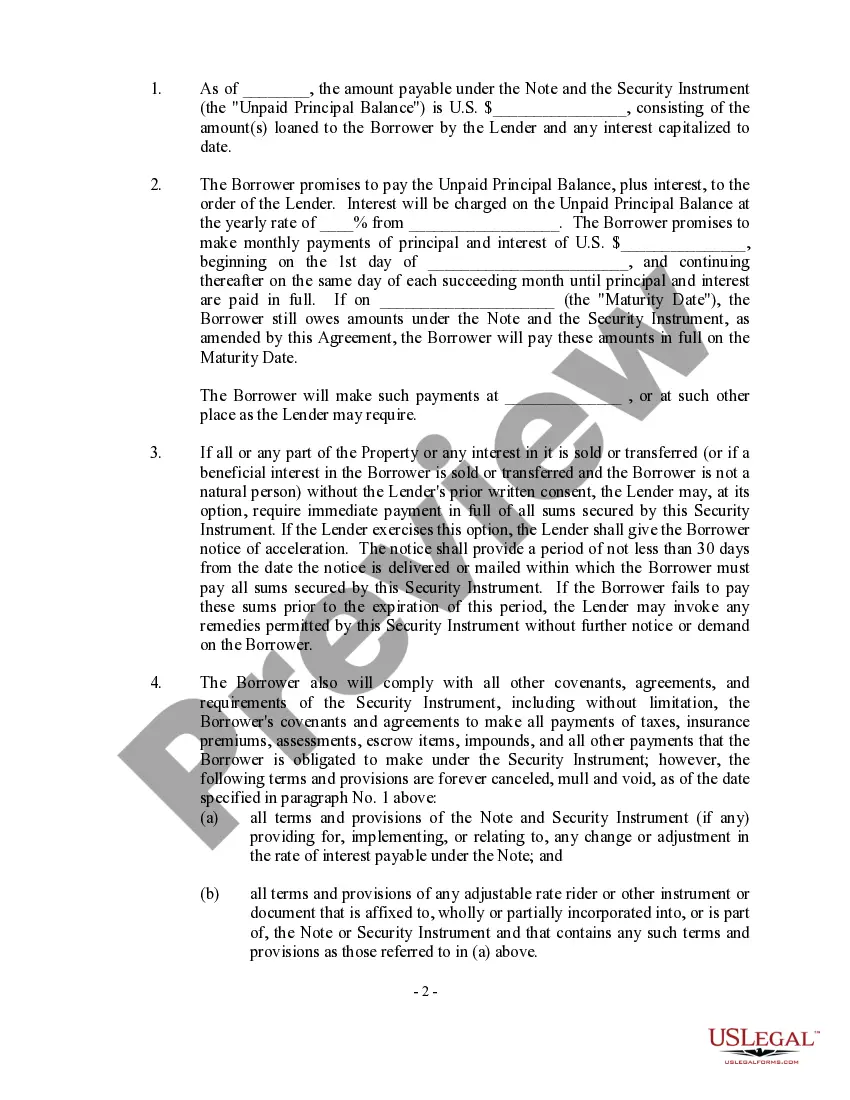

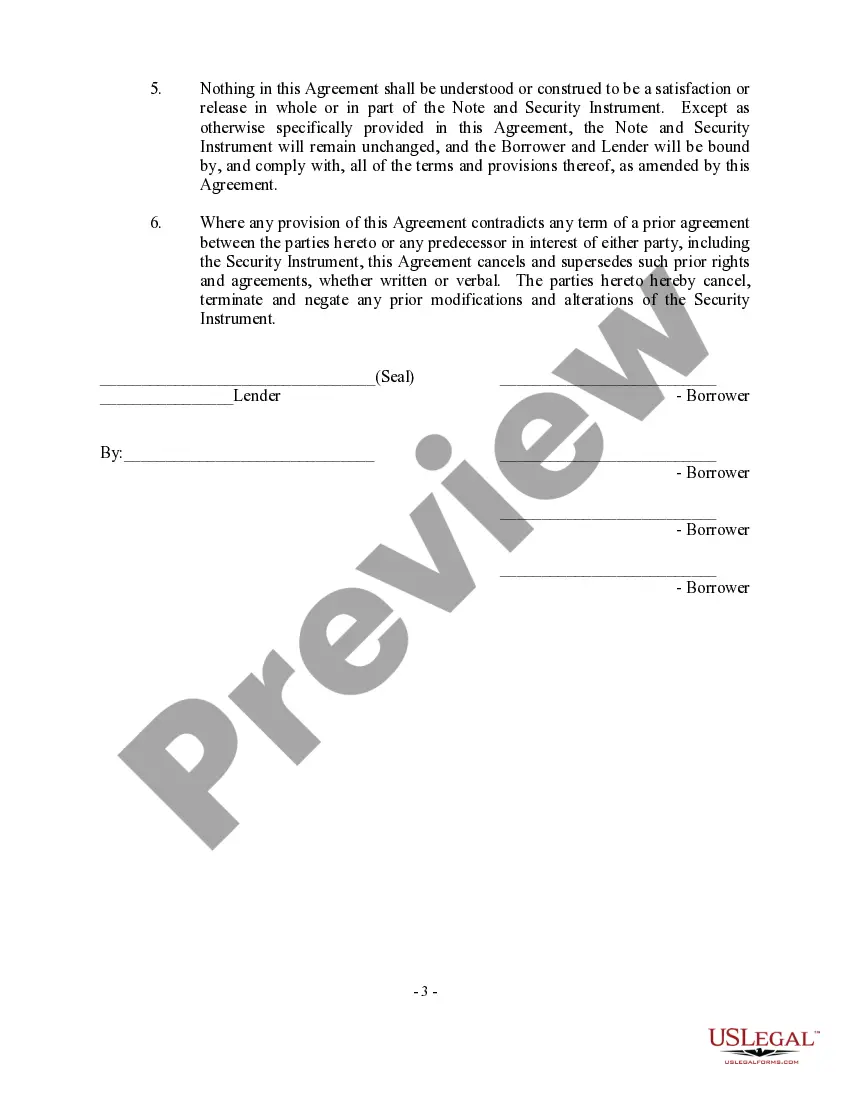

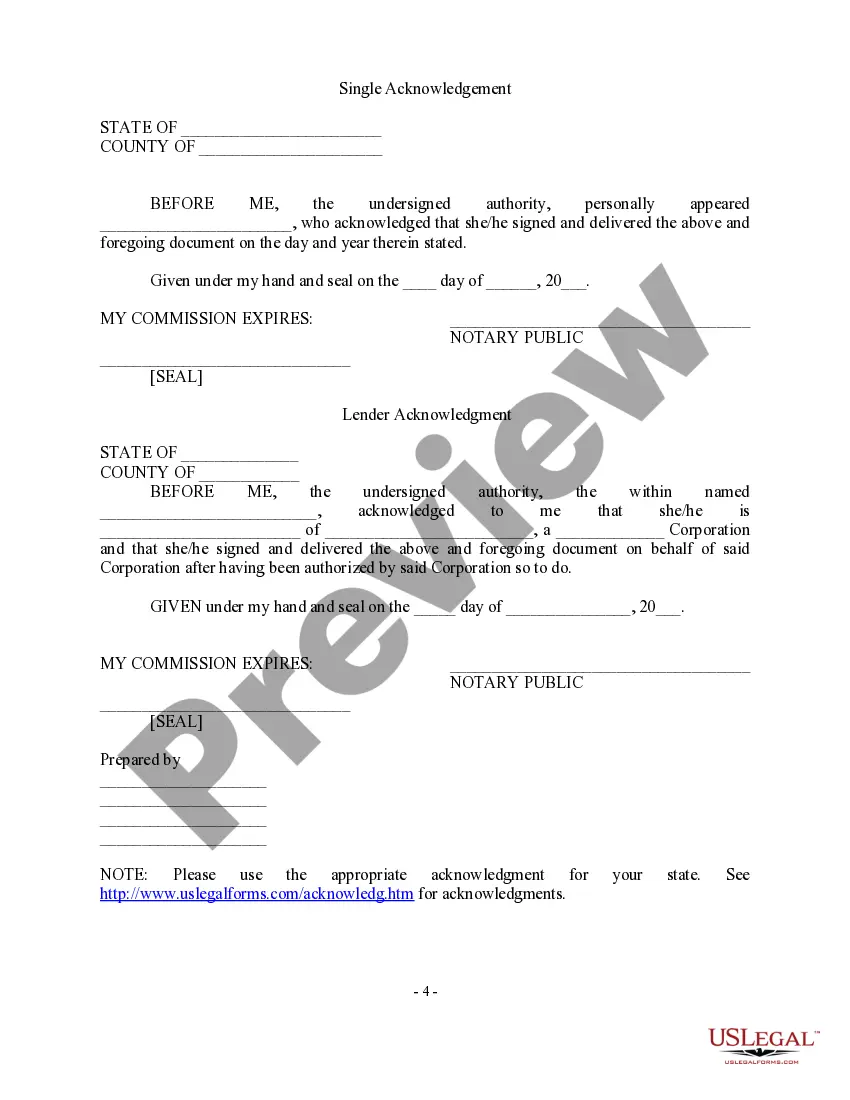

A Loan Modification Agreement is a legal document that is commonly used in San Antonio, Texas, and other states to modify the terms of an existing loan. It is specifically designed to help homeowners who are struggling to meet their mortgage payments and avoid foreclosure. The San Antonio Texas Loan Modification Agreement — Multistate is a standardized form that caters to borrowers residing in San Antonio, Texas, and other interested parties in multiple states. This agreement is authorized and regulated by state and federal laws, making it a legally binding contract between the lender and the borrower. The purpose of a Loan Modification Agreement is to provide borrowers with additional options to ensure the successful repayment of their mortgage loan. It allows for a renegotiation of terms such as interest rates, monthly payments, loan duration, and even principal balance adjustments. By modifying the original loan agreement, borrowers can potentially lower their monthly payments, improve their financial situation, and avoid the devastating consequences of foreclosure. In San Antonio, Texas, there can be several types of Loan Modification Agreements tailored to meet the specific needs of different borrowers. These may include: 1. Rate Reduction Modification: This modification focuses on lowering the interest rate applied to the loan. It is particularly beneficial for borrowers facing financial hardships or adverse market conditions that have caused their mortgage payments to become unaffordable. A reduced interest rate can significantly lower their monthly payments, making it easier to meet their repayment obligations. 2. Term Extension Modification: In this type of modification, the loan's term is extended, allowing borrowers to have a longer time frame to repay their loan. This can help reduce the monthly payment burden by redistributing the principal balance over a more extended period. By extending the loan term, borrowers can make their payments more manageable and increase their chances of meeting their obligations. 3. Forbearance Agreement Modification: A forbearance agreement provides temporary relief to borrowers who are experiencing short-term financial difficulties. This modification typically involves the lender agreeing to temporarily suspend, reduce, or accept partial payments for a predetermined period. It allows borrowers to regain their financial stability without facing immediate foreclosure or damaging their credit score. 4. Principal Reduction Modification: For borrowers who owe more on their mortgage loan than their home is currently worth, a principal reduction modification may be an option. This modification involves reducing the outstanding principal balance of the loan, which can result in lower monthly payments and make the loan more affordable. It is important to note that the specific terms and conditions of a Loan Modification Agreement may vary depending on the lender, borrower's circumstances, and applicable state laws. Consulting with a qualified attorney or a reputable loan modification professional is highly recommended before entering into any loan modification agreement to ensure that your rights and interests are protected.

San Antonio Texas Loan Modification Agreement - Multistate

Description

How to fill out San Antonio Texas Loan Modification Agreement - Multistate?

A document routine always goes along with any legal activity you make. Opening a company, applying or accepting a job offer, transferring ownership, and many other life situations require you prepare official documentation that varies throughout the country. That's why having it all collected in one place is so helpful.

US Legal Forms is the largest online collection of up-to-date federal and state-specific legal forms. Here, you can easily find and download a document for any personal or business objective utilized in your region, including the San Antonio Loan Modification Agreement - Multistate.

Locating samples on the platform is amazingly simple. If you already have a subscription to our service, log in to your account, find the sample using the search bar, and click Download to save it on your device. After that, the San Antonio Loan Modification Agreement - Multistate will be accessible for further use in the My Forms tab of your profile.

If you are using US Legal Forms for the first time, follow this quick guide to obtain the San Antonio Loan Modification Agreement - Multistate:

- Ensure you have opened the proper page with your localised form.

- Utilize the Preview mode (if available) and scroll through the sample.

- Read the description (if any) to ensure the template satisfies your requirements.

- Search for another document using the search tab in case the sample doesn't fit you.

- Click Buy Now once you find the required template.

- Decide on the appropriate subscription plan, then log in or register for an account.

- Choose the preferred payment method (with credit card or PayPal) to proceed.

- Opt for file format and save the San Antonio Loan Modification Agreement - Multistate on your device.

- Use it as needed: print it or fill it out electronically, sign it, and send where requested.

This is the easiest and most reliable way to obtain legal paperwork. All the templates provided by our library are professionally drafted and checked for correspondence to local laws and regulations. Prepare your paperwork and run your legal affairs properly with the US Legal Forms!