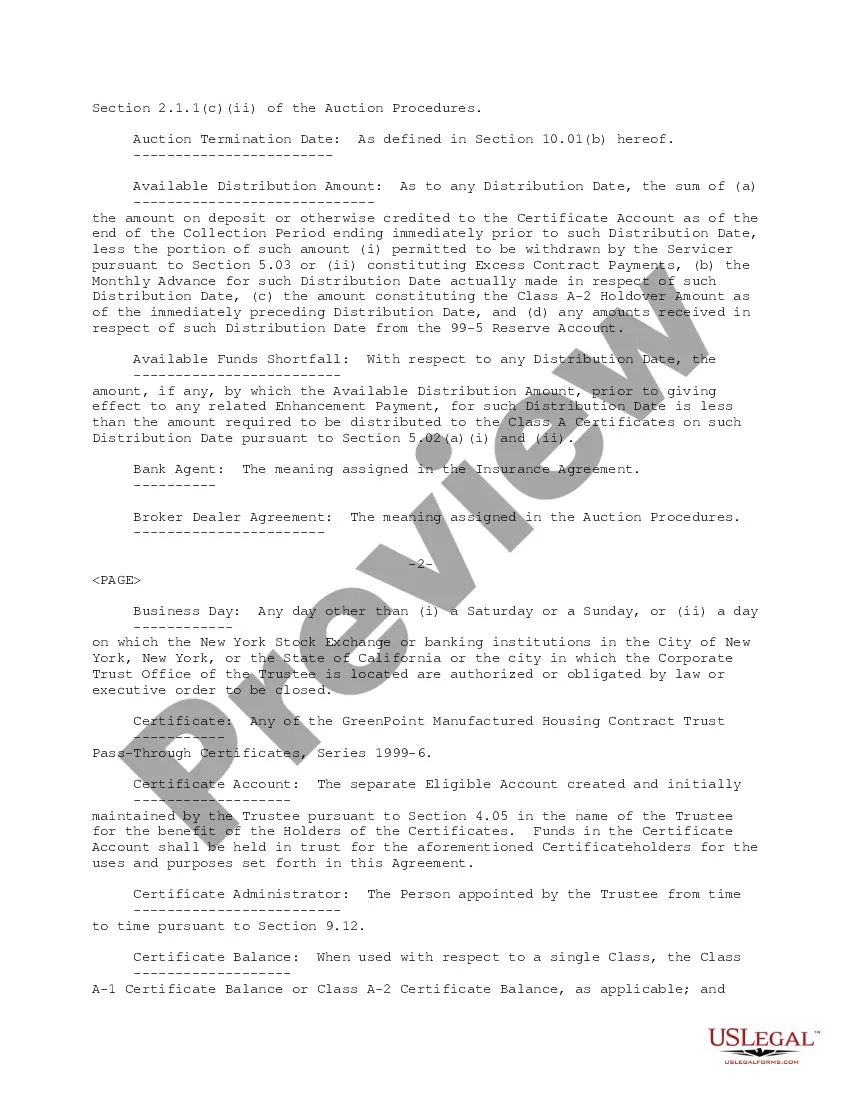

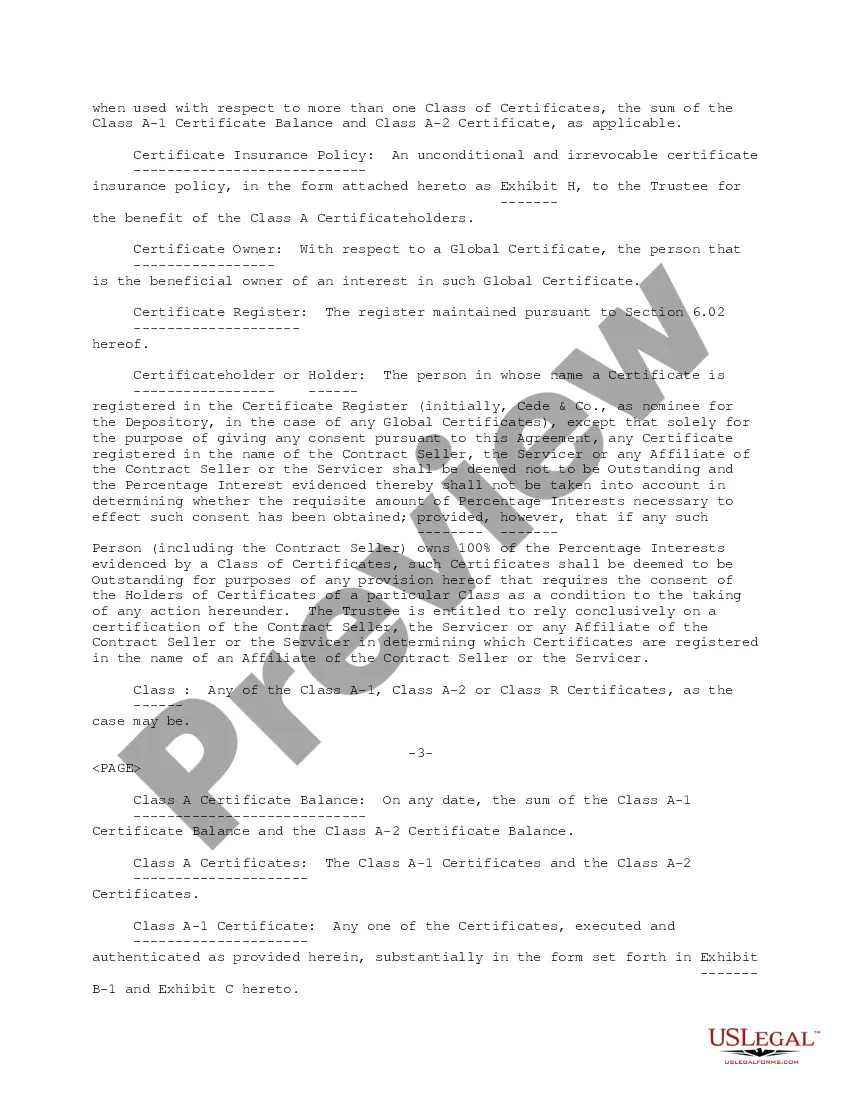

The Cook Illinois Pooling and Servicing Agreement between Green point Credit, LLC and Bank One, National Association is a legal contract that outlines the terms and conditions of pooling and servicing residential mortgage loans. This agreement typically covers the securitization process, including the pooling of loans, issuance of securities, and the ongoing servicing of the mortgage loans. One type of Cook Illinois Pooling and Servicing Agreement that may exist between Green point Credit, LLC and Bank One, National Association is the "Master Pooling and Servicing Agreement." This agreement serves as a foundational document that governs the overall relationship between the two parties in pooling and servicing residential mortgage loans. It establishes the roles, responsibilities, and obligations of both Green point Credit, LLC (the originator/seller) and Bank One, National Association (the trustee). Another type of Cook Illinois Pooling and Servicing Agreement could be the "Supplemental Pooling and Servicing Agreement." These agreements act as addendums to the master agreement, addressing specific provisions and conditions related to a particular pool of mortgage loans. The supplemental agreements may define additional eligibility criteria, loan types, credit enhancements, or performance criteria as required for a specific securitization transaction. The Cook Illinois Pooling and Servicing Agreement also encompasses a range of key elements and provisions, such as: 1. Loan Pool Characteristics: It details the characteristics of the mortgage loans included in the pool, such as loan type (e.g., fixed-rate, adjustable-rate), loan balance, interest rate, and geographical location. 2. Pooling Criteria: The agreement defines the criteria for including loans in the pool, such as credit scores, loan-to-value ratios, payment history, and documentation requirements. 3. Servicing Duties: It outlines the duties and responsibilities of the service, such as collecting mortgage payments, maintaining escrow accounts, managing delinquencies, and handling loan modifications or defaults. 4. Cash Flows and Disbursement: The agreement specifies how the cash flows related to the mortgage loans are collected, distributed, and allocated among various parties, including investors and services. 5. Representations and Warranties: It includes representations and warranties made by the originator regarding the accuracy and completeness of loan information, compliance with applicable laws, and the absence of fraud or misrepresentation. 6. Prepayment and Default: The agreement addresses the treatment of prepayments, defaulting loans, foreclosure procedures, and the allocation of losses and recoveries. Overall, the Cook Illinois Pooling and Servicing Agreement between Green point Credit, LLC and Bank One, National Association serves to define the rights, responsibilities, and obligations of the parties involved in the securitization and servicing of residential mortgage loans. It ensures compliance with applicable regulations and establishes a framework for efficient loan administration and investor protection.

Cook Illinois Pooling and Servicing Agreement between Greenpoint Credit, LLC and Bank One, National Association

Description

How to fill out Cook Illinois Pooling And Servicing Agreement Between Greenpoint Credit, LLC And Bank One, National Association?

Do you need to quickly create a legally-binding Cook Pooling and Servicing Agreement between Greenpoint Credit, LLC and Bank One, National Association or maybe any other form to take control of your personal or corporate affairs? You can select one of the two options: contact a legal advisor to write a valid document for you or draft it entirely on your own. The good news is, there's another option - US Legal Forms. It will help you receive neatly written legal paperwork without having to pay unreasonable fees for legal services.

US Legal Forms provides a rich catalog of over 85,000 state-specific form templates, including Cook Pooling and Servicing Agreement between Greenpoint Credit, LLC and Bank One, National Association and form packages. We offer documents for a myriad of life circumstances: from divorce papers to real estate document templates. We've been out there for more than 25 years and gained a rock-solid reputation among our clients. Here's how you can become one of them and obtain the necessary template without extra hassles.

- To start with, double-check if the Cook Pooling and Servicing Agreement between Greenpoint Credit, LLC and Bank One, National Association is tailored to your state's or county's laws.

- In case the document has a desciption, make sure to verify what it's intended for.

- Start the searching process over if the form isn’t what you were seeking by using the search bar in the header.

- Choose the subscription that is best suited for your needs and move forward to the payment.

- Choose the file format you would like to get your document in and download it.

- Print it out, fill it out, and sign on the dotted line.

If you've already registered an account, you can easily log in to it, find the Cook Pooling and Servicing Agreement between Greenpoint Credit, LLC and Bank One, National Association template, and download it. To re-download the form, simply head to the My Forms tab.

It's effortless to find and download legal forms if you use our services. Additionally, the templates we provide are updated by law professionals, which gives you greater confidence when dealing with legal matters. Try US Legal Forms now and see for yourself!