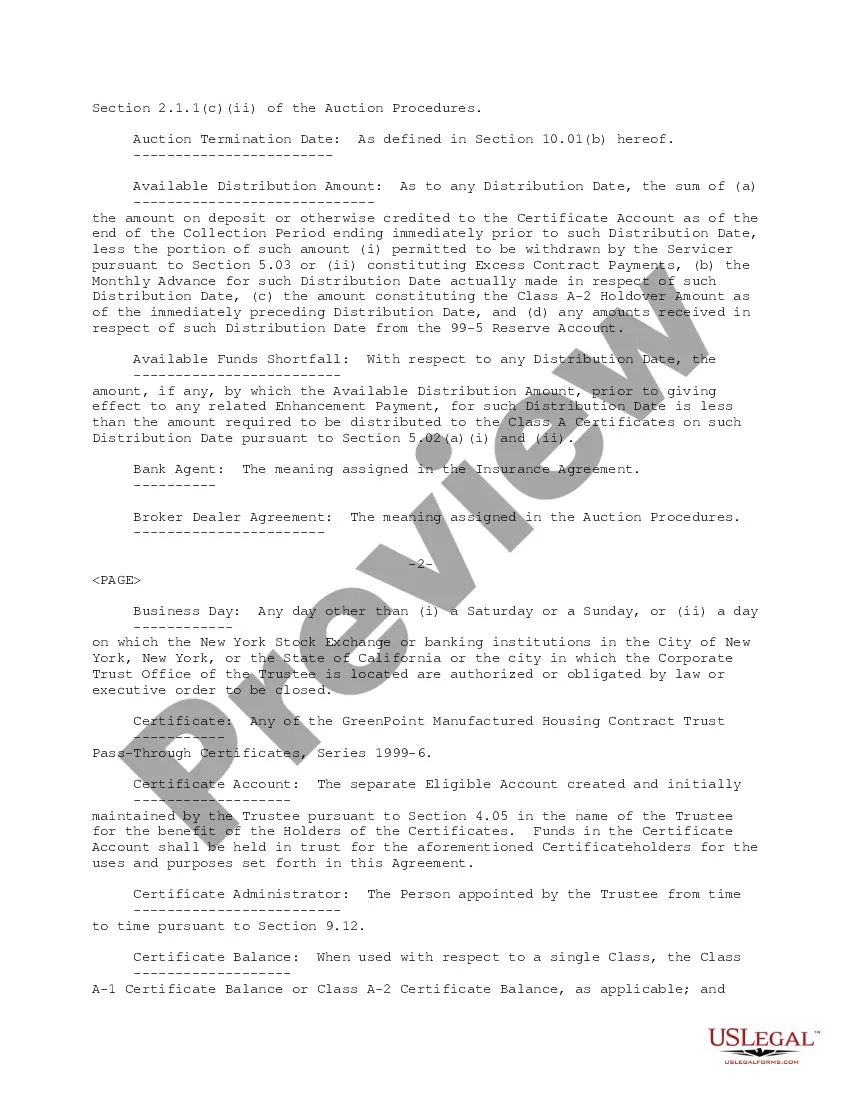

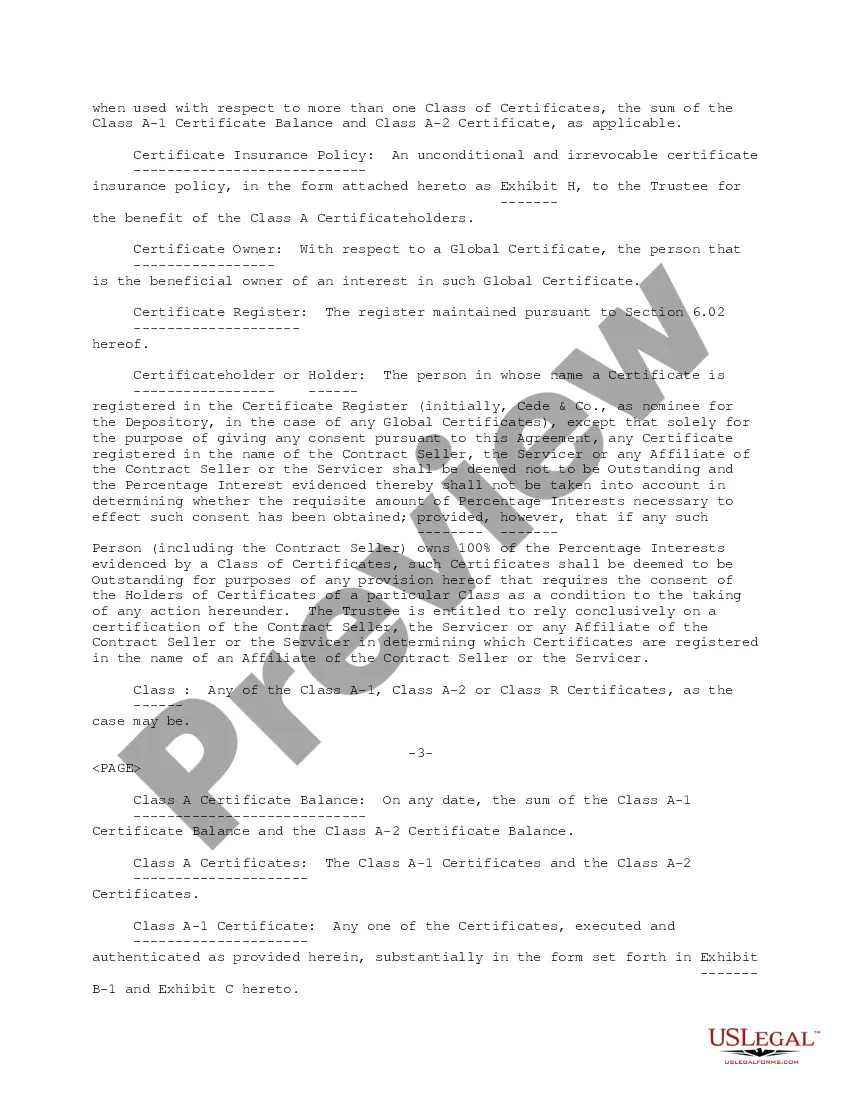

Phoenix Arizona Pooling and Servicing Agreement between Green point Credit, LLC and Bank One, National Association is a legal agreement that outlines the specific terms and conditions governing the pooling and servicing of mortgage loans. This agreement is crucial for both parties involved in the securitization and management of mortgage-backed securities (MBS) in Phoenix, Arizona. The Phoenix Arizona Pooling and Servicing Agreement establishes a comprehensive framework for the transfer and management of mortgage loans, including the collection of payments, distribution of cash flows, and resolution of delinquencies or defaults. It establishes the rights, obligations, and duties of both Green point Credit, LLC (originator/service) and Bank One, National Association (trustee), ensuring the smooth functioning and compliance with relevant regulations. Keywords: Phoenix Arizona, Pooling and Servicing Agreement, Green point Credit, LLC, Bank One, National Association, mortgage loans, mortgage-backed securities, securitization, management, cash flows, delinquencies, defaults, originator, service, trustee, compliance, regulations. Different types of Phoenix Arizona Pooling and Servicing Agreements between Green point Credit, LLC and Bank One, National Association may vary based on the type and characteristics of the mortgage loans being securitized or serviced. These types can include but are not limited to: 1. Prime Mortgage Pooling and Servicing Agreement: This agreement involves prime mortgage loans, which are typically issued to borrowers with excellent credit and low default risk. The agreement may contain specific provisions tailored to the characteristics of prime loans, including prepayment penalties or particular eligibility criteria. 2. Subprime Mortgage Pooling and Servicing Agreement: This type of agreement applies to subprime mortgage loans, which are offered to borrowers with less favorable credit profiles. The agreement may incorporate additional risk mitigation measures and safeguards to address the higher default risk associated with subprime mortgages. 3. Adjustable-Rate Mortgage (ARM) Pooling and Servicing Agreement: This agreement pertains to mortgage loans with adjustable interest rates. It outlines how the interest rates are adjusted and how the servicing and cash flow management are adapted to accommodate the changing nature of ARM loans. 4. Jumbo Mortgage Pooling and Servicing Agreement: This type of agreement focuses on jumbo mortgage loans, which exceed the maximum loan limits set by government-sponsored enterprises (Uses) like Fannie Mae or Freddie Mac. It may include specific provisions related to the higher loan amounts and lending criteria associated with jumbo mortgages. These are some possible variations of Phoenix Arizona Pooling and Servicing Agreements between Green point Credit, LLC and Bank One, National Association. The specific terms, conditions, and types of agreements depend on the nature of the mortgage loans, market conditions, and regulatory requirements prevailing at the time of the agreement's creation.

Phoenix Arizona Pooling and Servicing Agreement between Greenpoint Credit, LLC and Bank One, National Association

Description

How to fill out Phoenix Arizona Pooling And Servicing Agreement Between Greenpoint Credit, LLC And Bank One, National Association?

Preparing legal paperwork can be burdensome. In addition, if you decide to ask a legal professional to draft a commercial agreement, papers for ownership transfer, pre-marital agreement, divorce papers, or the Phoenix Pooling and Servicing Agreement between Greenpoint Credit, LLC and Bank One, National Association, it may cost you a lot of money. So what is the best way to save time and money and draft legitimate forms in total compliance with your state and local laws and regulations? US Legal Forms is an excellent solution, whether you're looking for templates for your personal or business needs.

US Legal Forms is largest online collection of state-specific legal documents, providing users with the up-to-date and professionally checked forms for any scenario accumulated all in one place. Consequently, if you need the current version of the Phoenix Pooling and Servicing Agreement between Greenpoint Credit, LLC and Bank One, National Association, you can easily find it on our platform. Obtaining the papers takes a minimum of time. Those who already have an account should check their subscription to be valid, log in, and select the sample with the Download button. If you haven't subscribed yet, here's how you can get the Phoenix Pooling and Servicing Agreement between Greenpoint Credit, LLC and Bank One, National Association:

- Glance through the page and verify there is a sample for your area.

- Examine the form description and use the Preview option, if available, to ensure it's the template you need.

- Don't worry if the form doesn't satisfy your requirements - search for the correct one in the header.

- Click Buy Now once you find the required sample and pick the best suitable subscription.

- Log in or register for an account to pay for your subscription.

- Make a payment with a credit card or through PayPal.

- Choose the file format for your Phoenix Pooling and Servicing Agreement between Greenpoint Credit, LLC and Bank One, National Association and download it.

Once done, you can print it out and complete it on paper or import the template to an online editor for a faster and more practical fill-out. US Legal Forms allows you to use all the paperwork ever obtained multiple times - you can find your templates in the My Forms tab in your profile. Try it out now!