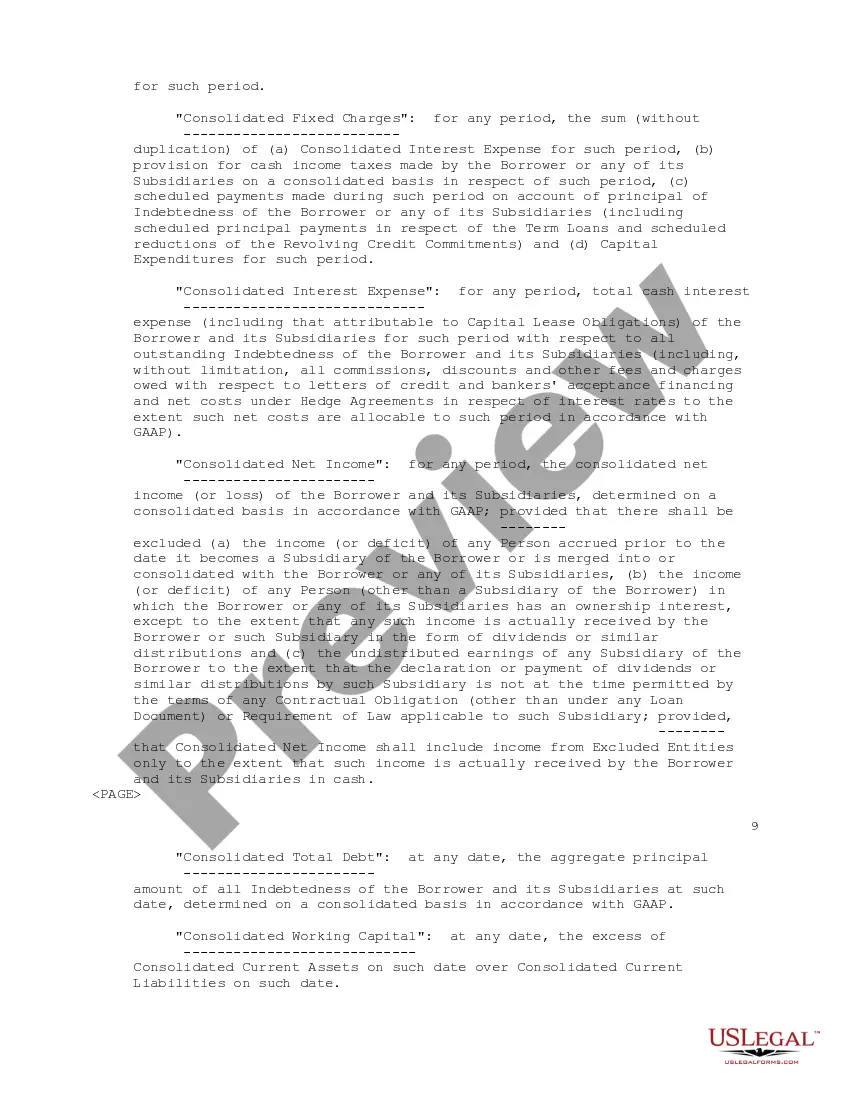

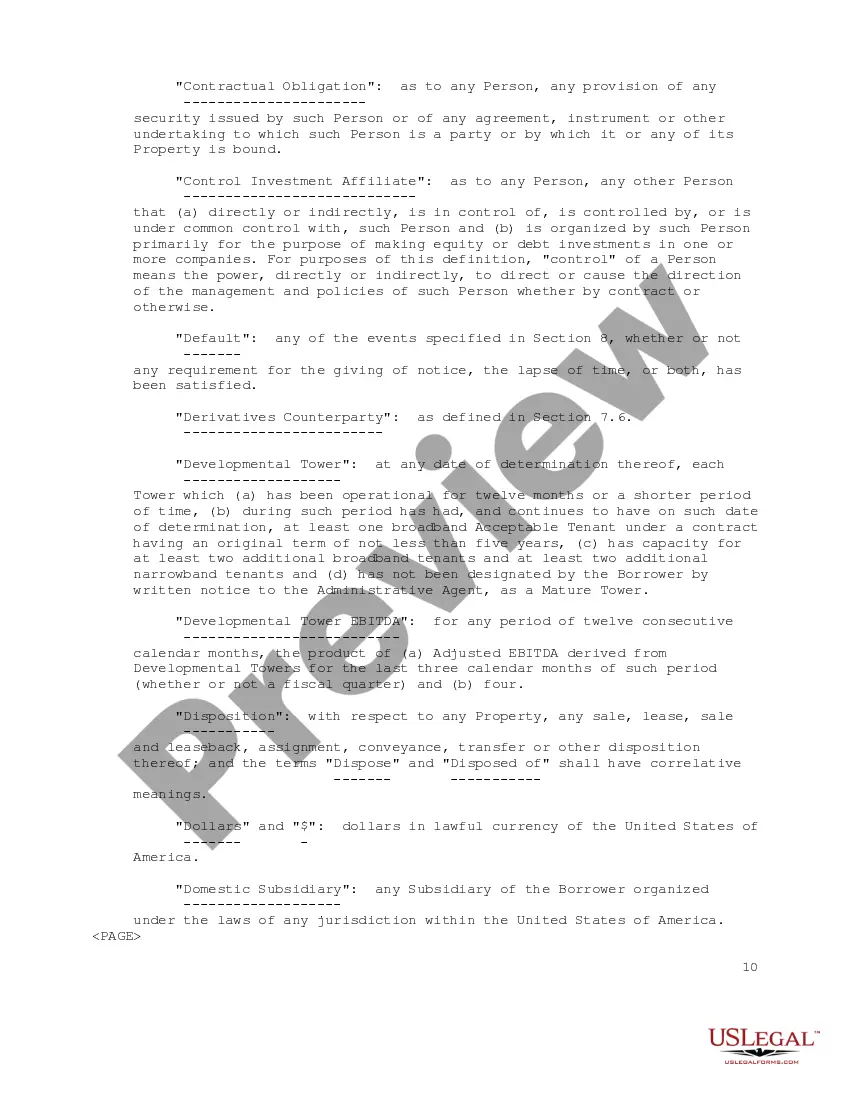

The Contra Costa California Second Amended and Restated Credit Agreement is a legally binding document among SBA Communications, Corp., SBA Telecommunications, Inc., and several banks and financial institutions. This agreement serves as a lending and borrowing mechanism, outlining the terms and conditions under which the borrower, SBA Communications, Corp. and SBA Telecommunications, Inc., can access credit facilities provided by the lenders. Keywords: Contra Costa California SCC, Second Amended and Restated Credit Agreement, SBA Communications, Corp., SBA Telecommunications, Inc., banks, financial institutions, lending, borrowing, credit facilities. There may be different types of Contra Costa California Second Amended and Restated Credit Agreement, and they could be categorized based on various factors such as duration, purpose, and specific terms. Some possible types could include: 1. Revolving Credit Facility Agreement: This type of agreement allows the borrower to access credit on an ongoing basis up to a predetermined limit. The borrower can borrow, repay, and borrow again within the agreed-upon timeframe. The lenders provide a revolving line of credit, and interest is charged on the outstanding balance. 2. Term Loan Agreement: In this type of agreement, the borrower receives a lump sum loan for a specific period, known as the term. The loan is repaid in regular installments over the term, typically with fixed interest rates. It provides a more structured approach to borrowing, suitable for long-term financing needs. 3. Syndicated Credit Agreement: This agreement involves multiple lenders who come together to provide a large credit facility to the borrower. The lenders form a syndicate to share the financial risk and diversify their exposure. The borrower benefits from accessing a larger pool of funds through this type of agreement. 4. Secured Credit Agreement: This agreement involves the borrower providing collateral as security against the credit facility. The collateral could be assets such as real estate, equipment, or inventory. This provides the lenders with a form of recourse if the borrower fails to repay the loan, reducing their risk. 5. Unsecured Credit Agreement: On the contrary, this agreement does not require any collateral from the borrower. The lenders rely solely on the borrower's creditworthiness and ability to repay the loan based on their financial strength and cash flow. Unsecured credit agreements may have higher interest rates to compensate for the increased risk. These are just a few examples of the possible types of Contra Costa California Second Amended and Restated Credit Agreements. The specific terms and conditions, as well as the type chosen, would depend on the unique needs and circumstances of the parties involved.

Contra Costa California Second Amended and Restated Credit Agreement among SBA Communications, Corp., SBA Telecommunications, Inc., Several Banks and Financial Institutions

Description

How to fill out Contra Costa California Second Amended And Restated Credit Agreement Among SBA Communications, Corp., SBA Telecommunications, Inc., Several Banks And Financial Institutions?

Preparing legal documentation can be burdensome. Besides, if you decide to ask a lawyer to draft a commercial agreement, documents for ownership transfer, pre-marital agreement, divorce papers, or the Contra Costa Second Amended and Restated Credit Agreement among SBA Communications, Corp., SBA Telecommunications, Inc., Several Banks and Financial Institutions, it may cost you a lot of money. So what is the best way to save time and money and create legitimate documents in total compliance with your state and local laws and regulations? US Legal Forms is a great solution, whether you're searching for templates for your individual or business needs.

US Legal Forms is biggest online library of state-specific legal documents, providing users with the up-to-date and professionally verified templates for any use case collected all in one place. Therefore, if you need the latest version of the Contra Costa Second Amended and Restated Credit Agreement among SBA Communications, Corp., SBA Telecommunications, Inc., Several Banks and Financial Institutions, you can easily find it on our platform. Obtaining the papers takes a minimum of time. Those who already have an account should check their subscription to be valid, log in, and select the sample by clicking on the Download button. If you haven't subscribed yet, here's how you can get the Contra Costa Second Amended and Restated Credit Agreement among SBA Communications, Corp., SBA Telecommunications, Inc., Several Banks and Financial Institutions:

- Look through the page and verify there is a sample for your region.

- Examine the form description and use the Preview option, if available, to ensure it's the template you need.

- Don't worry if the form doesn't suit your requirements - look for the right one in the header.

- Click Buy Now once you find the needed sample and choose the best suitable subscription.

- Log in or register for an account to purchase your subscription.

- Make a payment with a credit card or via PayPal.

- Opt for the file format for your Contra Costa Second Amended and Restated Credit Agreement among SBA Communications, Corp., SBA Telecommunications, Inc., Several Banks and Financial Institutions and save it.

When done, you can print it out and complete it on paper or upload the template to an online editor for a faster and more practical fill-out. US Legal Forms enables you to use all the documents ever purchased many times - you can find your templates in the My Forms tab in your profile. Try it out now!