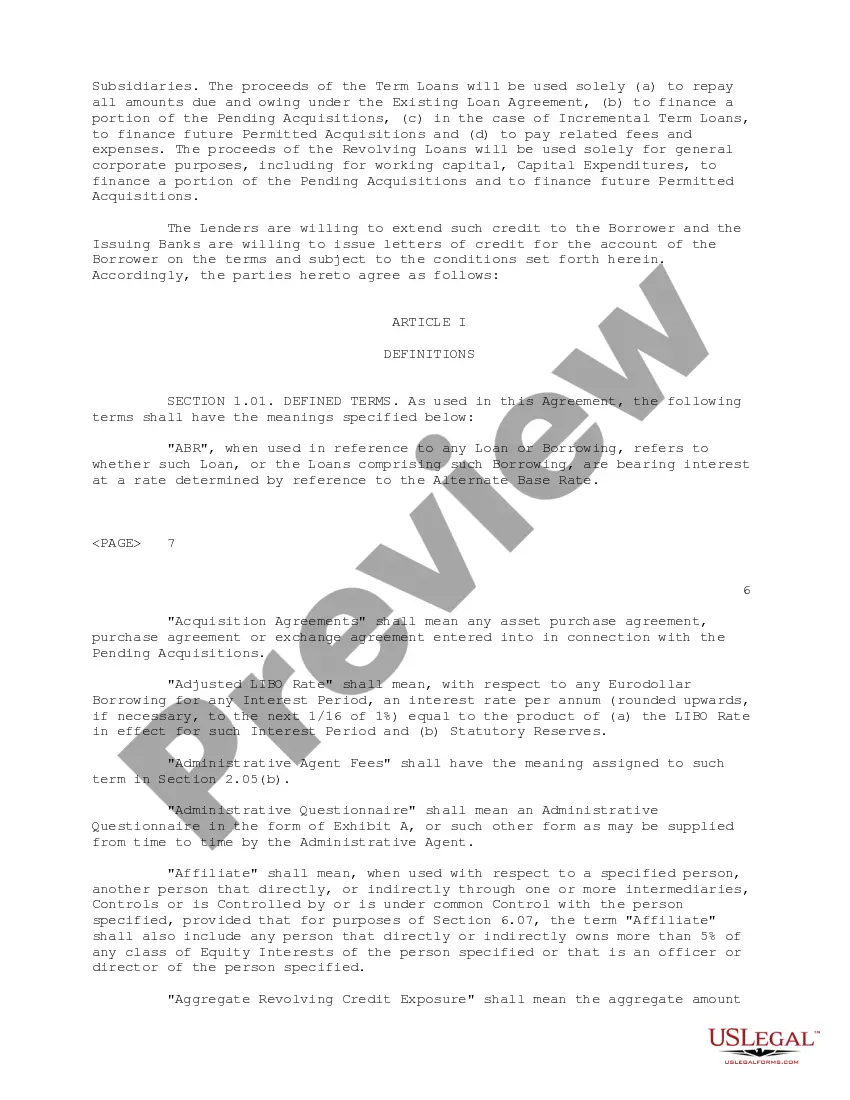

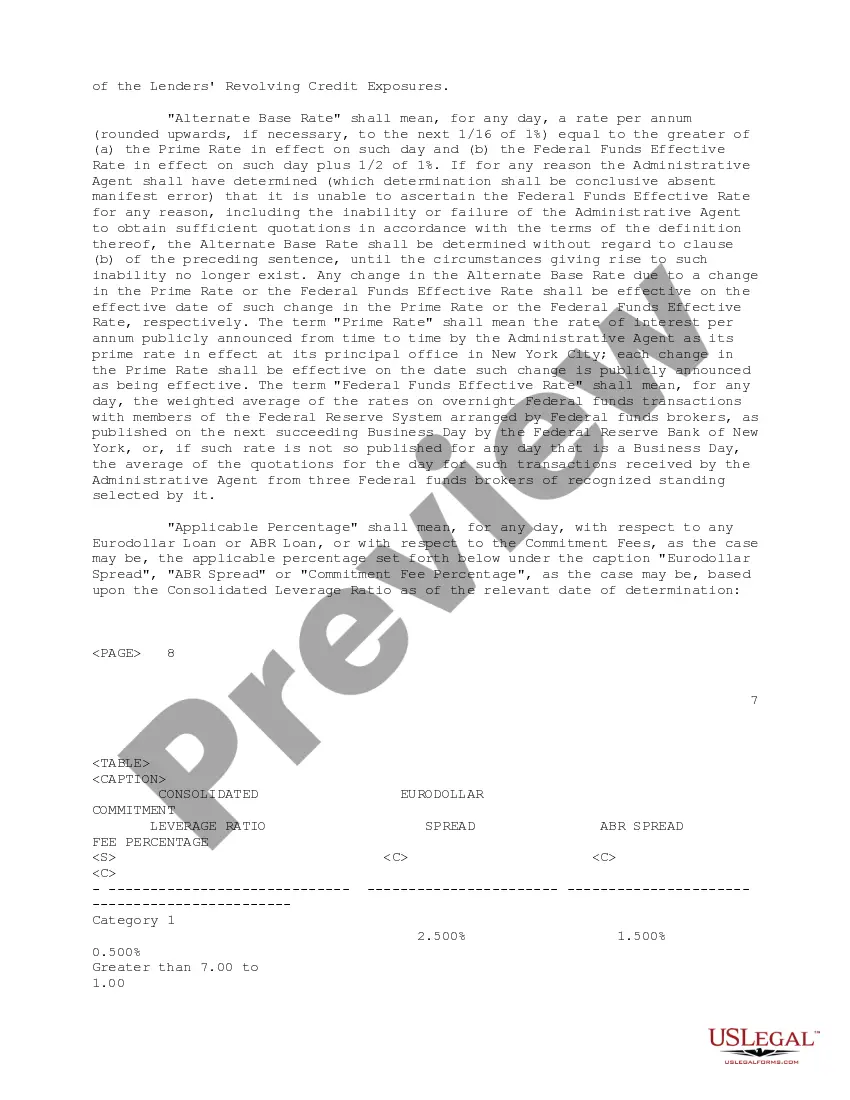

Riverside California Credit Agreement regarding extension of credit is a legal contract between a lender and a borrower, outlining the terms and conditions for providing credit. This agreement specifies the amount of credit being extended, the interest rates and fees associated with the credit, and the repayment terms. Riverside California Credit Agreement can be categorized into various types based on the purpose of credit extension. Some common types include: 1. Personal Credit Agreement: This type of agreement is used when individuals borrow money for personal needs, such as purchasing a home or a vehicle. The terms and conditions may vary, but generally include the loan amount, interest rate, monthly repayment installments, and any collateral required. 2. Business Credit Agreement: When businesses require funding to support their operations or expansion plans, they enter into a business credit agreement. This agreement outlines the terms for credit extension, such as credit limits, repayment schedule, and any specific conditions associated with the credit facility. It may also include provisions for business loans, lines of credit, or commercial credit cards. 3. Revolving Credit Agreement: A revolving credit agreement allows borrowers to access a predetermined credit limit repeatedly, as long as they repay the borrowed amounts within specified timeframes. This type of agreement is often used for business purposes, providing flexibility for cash flow management and short-term financing needs. 4. Secured Credit Agreement: In a secured credit agreement, the borrower provides collateral, such as real estate, equipment, or inventory, as security for the credit being extended. This reduces the lender's risk and typically leads to lower interest rates for the borrower. If the borrower defaults on repayment, the lender can seize and sell the collateral to recover the outstanding debt. 5. Unsecured Credit Agreement: Unlike secured credit agreements, unsecured credit agreements do not require collateral. These agreements are primarily based on the borrower's creditworthiness, financial history, and income. Due to the higher risk involved for the lender, interest rates on unsecured credit may be higher compared to secured credit agreements. 6. Credit Card Agreement: Credit card agreements fall under the Riverside California Credit Agreement umbrella as well. These agreements specify the terms and conditions for using a credit card, including the credit limit, interest rates, fees, and payment terms. They also define the borrower's responsibilities, such as timely repayments and reporting lost or stolen cards. In Riverside California, as in any other jurisdiction, Credit Agreements regarding extension of credit must comply with applicable state and federal laws to ensure fair practices, consumer protection, and transparency.

Riverside California Credit Agreement regarding extension of credit

Description

How to fill out Riverside California Credit Agreement Regarding Extension Of Credit?

Draftwing paperwork, like Riverside Credit Agreement regarding extension of credit, to take care of your legal matters is a tough and time-consumming process. Many situations require an attorney’s participation, which also makes this task not really affordable. However, you can take your legal affairs into your own hands and manage them yourself. US Legal Forms is here to the rescue. Our website features more than 85,000 legal forms intended for different cases and life situations. We ensure each document is compliant with the laws of each state, so you don’t have to worry about potential legal issues compliance-wise.

If you're already aware of our services and have a subscription with US, you know how easy it is to get the Riverside Credit Agreement regarding extension of credit template. Go ahead and log in to your account, download the template, and personalize it to your needs. Have you lost your document? No worries. You can find it in the My Forms tab in your account - on desktop or mobile.

The onboarding process of new users is just as easy! Here’s what you need to do before downloading Riverside Credit Agreement regarding extension of credit:

- Make sure that your document is specific to your state/county since the rules for creating legal papers may differ from one state another.

- Discover more information about the form by previewing it or going through a quick description. If the Riverside Credit Agreement regarding extension of credit isn’t something you were looking for, then use the header to find another one.

- Sign in or register an account to start using our website and download the document.

- Everything looks good on your side? Click the Buy now button and select the subscription plan.

- Select the payment gateway and enter your payment details.

- Your template is good to go. You can go ahead and download it.

It’s easy to locate and buy the needed document with US Legal Forms. Thousands of organizations and individuals are already benefiting from our extensive collection. Sign up for it now if you want to check what other benefits you can get with US Legal Forms!

Form popularity

FAQ

A credit agreement is a legally-binding contract documenting the terms of a loan agreement; it is made between a person or party borrowing money and a lender. The credit agreement outlines all of the terms associated with the loan.

Also known as a loan agreement. The main transaction document for a loan financing between one or more lenders and a borrower.

Extension of Credit means the right to defer payment of debt or to incur debt and defer its payment offered or granted primarily for personal, family, or household purposes.

More Definitions of Amended and Restated Credit Agreement Amended and Restated Credit Agreement means the Credit Agreement, dated as of the Issue Date, among the Company, the lenders party thereto from time to time and JPMorgan Chase Bank, National Association, as administrative agent thereunder.

Credit agreements are not legally binding. Lenders do not check a person's likelihood to repay before accepting a credit agreement. An annual fee is an amount paid to you by the credit card company for using their service each year.

These include credit sale agreements, hire purchase agreements and conditional sale agreements.

How do I find my Credit Agreements? Your reported Credit Agreements will appear on your Credit Report, giving you a detailed list of your current and past lenders, amounts owed, the status of the accounts, and more.

Credit, transaction between two parties in which one (the creditor or lender) supplies money, goods, services, or securities in return for a promised future payment by the other (the debtor or borrower).

A credit agreement is a legally binding contract between a borrower and a lender that must be agreed by both parties. It holds the terms of any type of credit, such as overdrafts, credit cards or personal loans. That's why a credit agreement for a personal loan is normally referred to as a loan agreement.

While a loan provides all the money requested in one go at the time it is issued, in the case of a credit, the bank provides the customer with an amount of money, which can be used as required, using the entire amount borrowed, part of it or none at all.