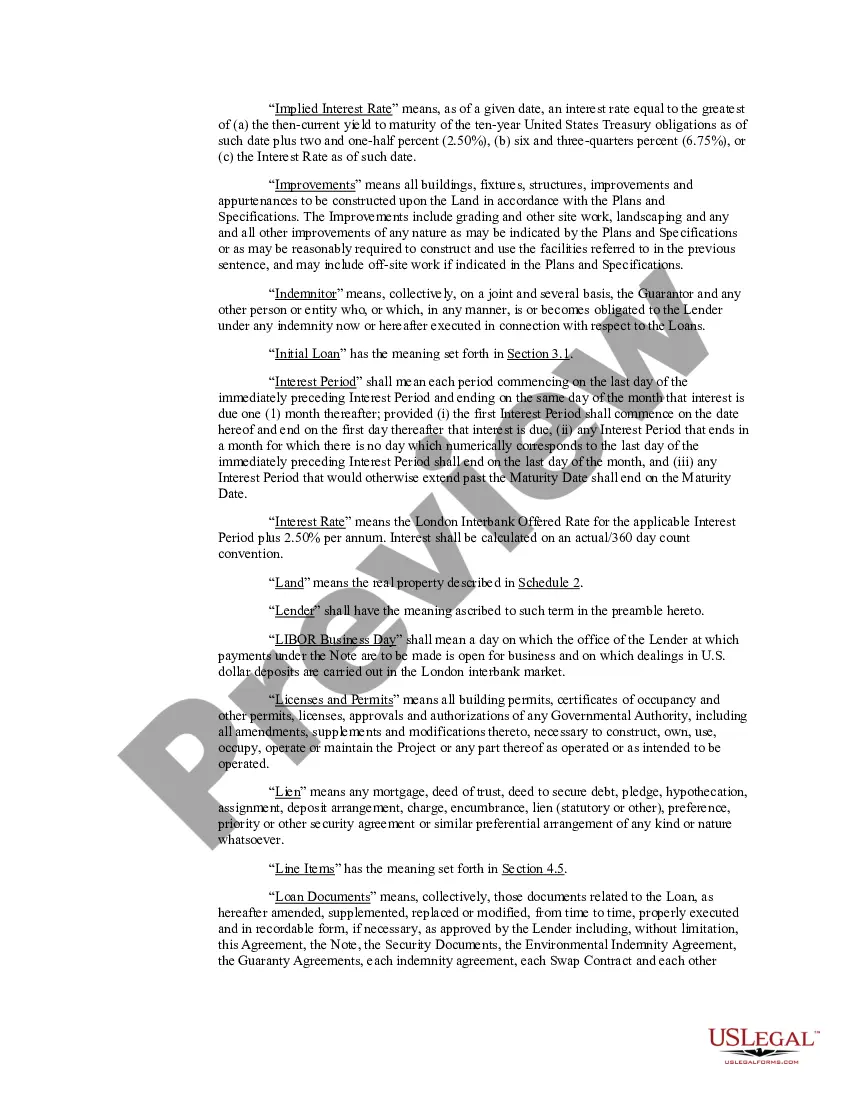

Wake North Carolina Construction Loan Agreement is a legal document that outlines the terms and conditions between a lender and a borrower for a construction loan in the Wake County area of North Carolina. This agreement is essential for ensuring a smooth and regulated lending process in the construction industry. The Wake North Carolina Construction Loan Agreement includes various key elements that define the rights and obligations of both parties involved. It specifies the loan amount, interest rate, repayment terms, and other financial details. Additionally, it contains provisions regarding the disbursement of funds, construction milestones, and potential penalties or fees associated with delays or defaults. There are different types of Wake North Carolina Construction Loan Agreements that cater to specific construction projects and borrower needs. These types include: 1. Traditional Construction Loan Agreement: This is the most common type of construction loan agreement, where the borrower obtains a loan to finance the construction of a new residential or commercial property. The agreement outlines the loan terms, draw schedule, and requirements for the borrower to access funds at different stages of the construction process. 2. Renovation Construction Loan Agreement: This type of agreement is designed for borrowers seeking financing to renovate or rehabilitate an existing property. It covers the renovation costs, project timeline, and the release of funds based on completed stages of the renovation work. 3. Speculative Construction Loan Agreement: Speculative construction loans are for builders or investors who construct properties without a pre-existing buyer. The agreement outlines the terms for the construction of a property that will be listed for sale upon completion. It may include provisions related to marketing efforts, repayment schedule, and the handling of proceeds from the sale. 4. Bridge Construction Loan Agreement: A bridge loan agreement is used when a borrower requires financing to bridge the gap between a construction project's completion and the long-term financing solution, such as securing a mortgage or selling the property. This agreement sets out the terms and specific repayment conditions until the permanent financing is obtained. 5. Owner-Builder Construction Loan Agreement: This type of agreement is suitable for individuals who act as both the borrower and the builder. It outlines the terms and responsibilities of the owner-builder throughout the construction process, including compliance with building codes, permits, and liability insurance requirements. In conclusion, the Wake North Carolina Construction Loan Agreement is a formal legal document that establishes the terms and conditions for financing construction projects in the Wake County area. Different types of agreements cater to various construction scenarios, such as new construction, renovations, speculations, bridge financing, and owner-builder projects. Ensuring a comprehensive and well-drafted agreement is essential to protect the interests of both the borrower and the lender during the construction loan process.

Wake North Carolina Construction Loan Agreement

Description

How to fill out Wake North Carolina Construction Loan Agreement?

Draftwing forms, like Wake Construction Loan Agreement, to manage your legal matters is a difficult and time-consumming task. A lot of cases require an attorney’s participation, which also makes this task not really affordable. However, you can take your legal issues into your own hands and take care of them yourself. US Legal Forms is here to save the day. Our website comes with more than 85,000 legal documents created for different scenarios and life circumstances. We make sure each form is compliant with the laws of each state, so you don’t have to worry about potential legal pitfalls associated with compliance.

If you're already aware of our website and have a subscription with US, you know how easy it is to get the Wake Construction Loan Agreement template. Simply log in to your account, download the template, and personalize it to your needs. Have you lost your form? Don’t worry. You can find it in the My Forms folder in your account - on desktop or mobile.

The onboarding process of new customers is just as straightforward! Here’s what you need to do before getting Wake Construction Loan Agreement:

- Ensure that your form is compliant with your state/county since the rules for writing legal paperwork may vary from one state another.

- Discover more information about the form by previewing it or reading a brief description. If the Wake Construction Loan Agreement isn’t something you were looking for, then use the header to find another one.

- Sign in or create an account to begin utilizing our service and get the document.

- Everything looks great on your side? Click the Buy now button and choose the subscription plan.

- Select the payment gateway and type in your payment details.

- Your form is ready to go. You can go ahead and download it.

It’s an easy task to find and buy the needed document with US Legal Forms. Thousands of businesses and individuals are already taking advantage of our rich library. Sign up for it now if you want to check what other perks you can get with US Legal Forms!