Queens New York How to Request a Home Affordable Modification Guide

Description

How to fill out Queens New York How To Request A Home Affordable Modification Guide?

Preparing legal paperwork can be difficult. In addition, if you decide to ask a lawyer to write a commercial contract, documents for ownership transfer, pre-marital agreement, divorce papers, or the Queens How to Request a Home Affordable Modification Guide, it may cost you a fortune. So what is the most reasonable way to save time and money and draw up legitimate documents in total compliance with your state and local laws and regulations? US Legal Forms is a perfect solution, whether you're searching for templates for your individual or business needs.

US Legal Forms is the most extensive online catalog of state-specific legal documents, providing users with the up-to-date and professionally checked templates for any use case collected all in one place. Therefore, if you need the recent version of the Queens How to Request a Home Affordable Modification Guide, you can easily locate it on our platform. Obtaining the papers takes a minimum of time. Those who already have an account should check their subscription to be valid, log in, and select the sample by clicking on the Download button. If you haven't subscribed yet, here's how you can get the Queens How to Request a Home Affordable Modification Guide:

- Look through the page and verify there is a sample for your area.

- Examine the form description and use the Preview option, if available, to ensure it's the template you need.

- Don't worry if the form doesn't suit your requirements - look for the right one in the header.

- Click Buy Now when you find the required sample and select the best suitable subscription.

- Log in or sign up for an account to pay for your subscription.

- Make a payment with a credit card or through PayPal.

- Choose the document format for your Queens How to Request a Home Affordable Modification Guide and download it.

Once finished, you can print it out and complete it on paper or import the samples to an online editor for a faster and more convenient fill-out. US Legal Forms enables you to use all the documents ever purchased many times - you can find your templates in the My Forms tab in your profile. Give it a try now!

Form popularity

FAQ

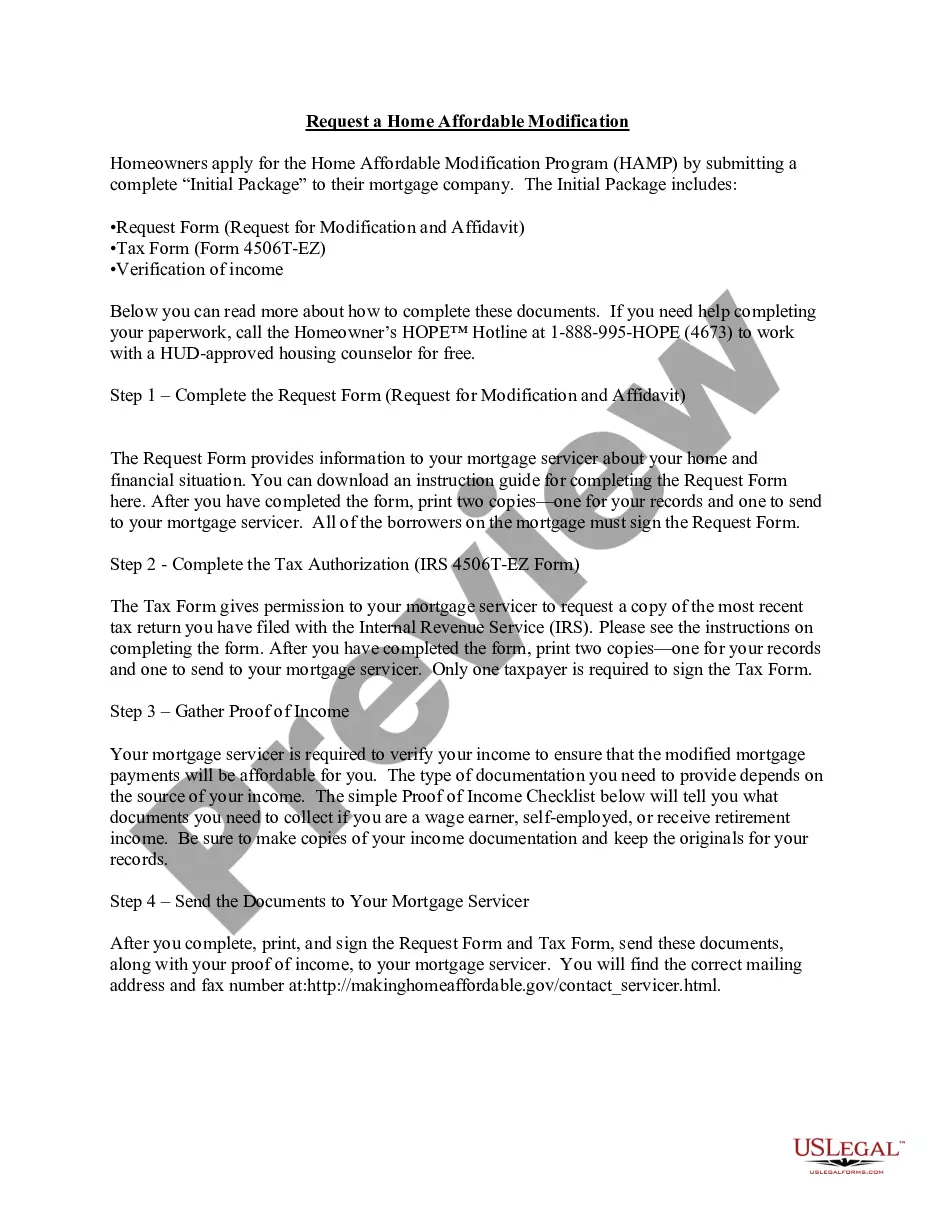

The HAMP allowed homeowners to reduce their mortgage principal and/or interest rates, temporarily postpone payments, or get loan extensions. The program expired at the end of 2016 and has not been renewed.

The Home Affordable Modification Program (HAMP), created in 2009 by the federal government, made it possible for struggling homeowners to stay afloat by modifying the original terms of their mortgage loans. The program ended in 2016, but other mortgage modifications programs have cropped up.

Loan modification is when a lender agrees to alter the terms of a homeowner's existing loan to help them avoid default and keep their house during times of financial hardship. The goal of a mortgage loan modification is to reduce the borrower's payments so they can afford their loan month-to-month.

Fannie Mae and Freddie Mac announced on Wednesday their replacement for the Home Affordable Modification Program. The government sponsored enterprises revealed the Flex Modification foreclosure prevention program, which is designed to help America's families by offering reductions to their monthly mortgage payments.

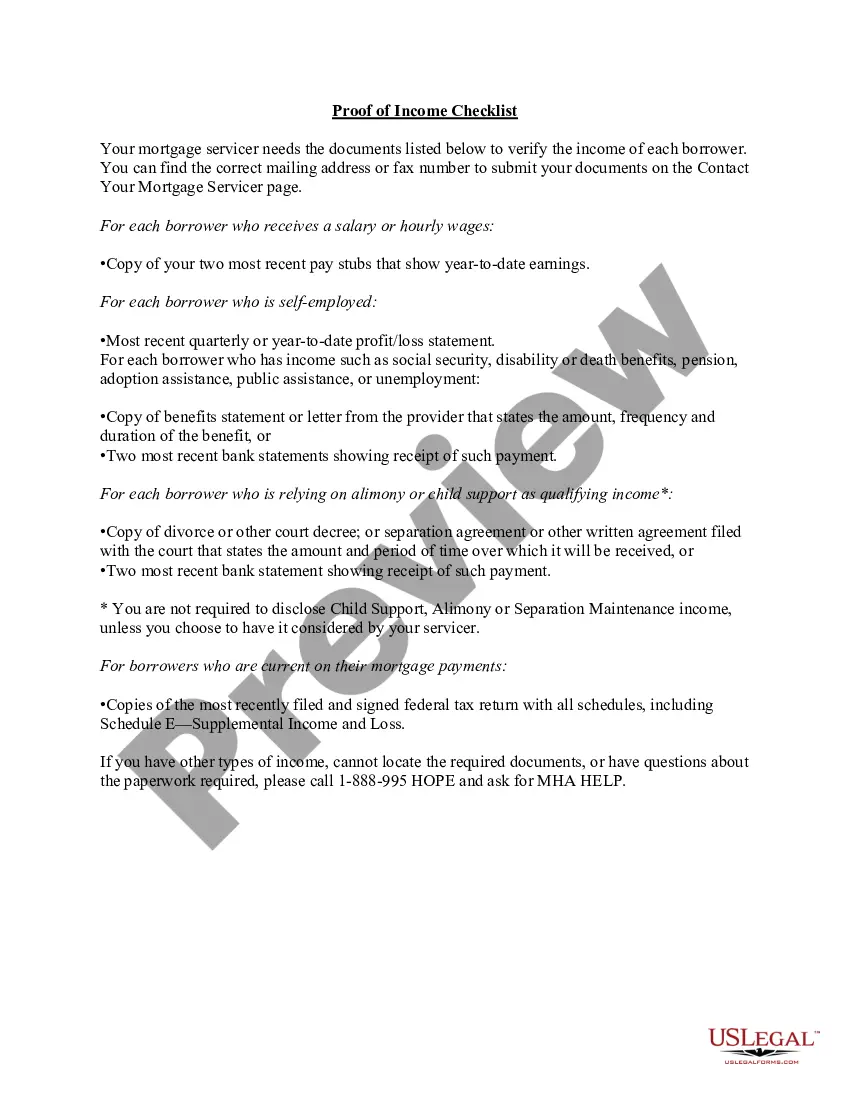

To qualify for a modification, you'll have to submit a complete "loss mitigation" application to your loan servicer. It's best to submit your application as soon as you know you'll have trouble making your payments or shortly after you fall behind.

How to Negotiate a Loan Modification Do Not Ignore Your Lender. When facing foreclosure, your lender will likely contact you regularly.Stay in the Home.Collect Evidence.Contact a Foreclosure Defense Attorney.Contact Your Lender.Be Patient.Let Our Florida Foreclosure Defense Lawyers Help With Your Loan Modification.

Tips for Getting a Mortgage Modification Approved Apply as soon as you can.Pay attention to detail.Send in all items requested by your loan servicers.Hold on to all information provided by your servicer.Put together a new monthly budget.Write a hardship letter and put careful thought into it.

You must have had the pre-modification FHA loan for at least 12 months before qualifying. If you've had the loan for only 12 months, you must have made at least 4 payments on it. The loan must be in default or imminent default, in which a missed payment is reasonably foreseeable.

It's not theoretically impossible to refinance under HARP after a HAMP modification. However, it may depend upon the terms of the modification, such as whether or not the loan modification included principal forgiveness or deferment, and other factors.

The loan modification process typically takes six (6) months to nine (9) months depending mostly on your bank and your ability to efficiently work through the process with your attorney.

Interesting Questions

More info

Griffith's program allows homeowners to get their existing mortgage modified under certain conditions. Those conditions include an initial down payment of 10 percent or less and a monthly payment of 20 percent of the home's value for three or more years. Griffiths works with a number of nonprofit agencies, like the National Community Reinvestment Coalition, to help distressed borrowers obtain loans to buy a home, either through the government mortgage market or from private lenders.

Disclaimer

The materials in this section are taken from public sources. We disclaim all representations or any warranties, express or implied, as to the accuracy, authenticity, reliability, accessibility, adequacy, or completeness of any data in this paragraph. Nevertheless, we make every effort to cite public sources deemed reliable and trustworthy.