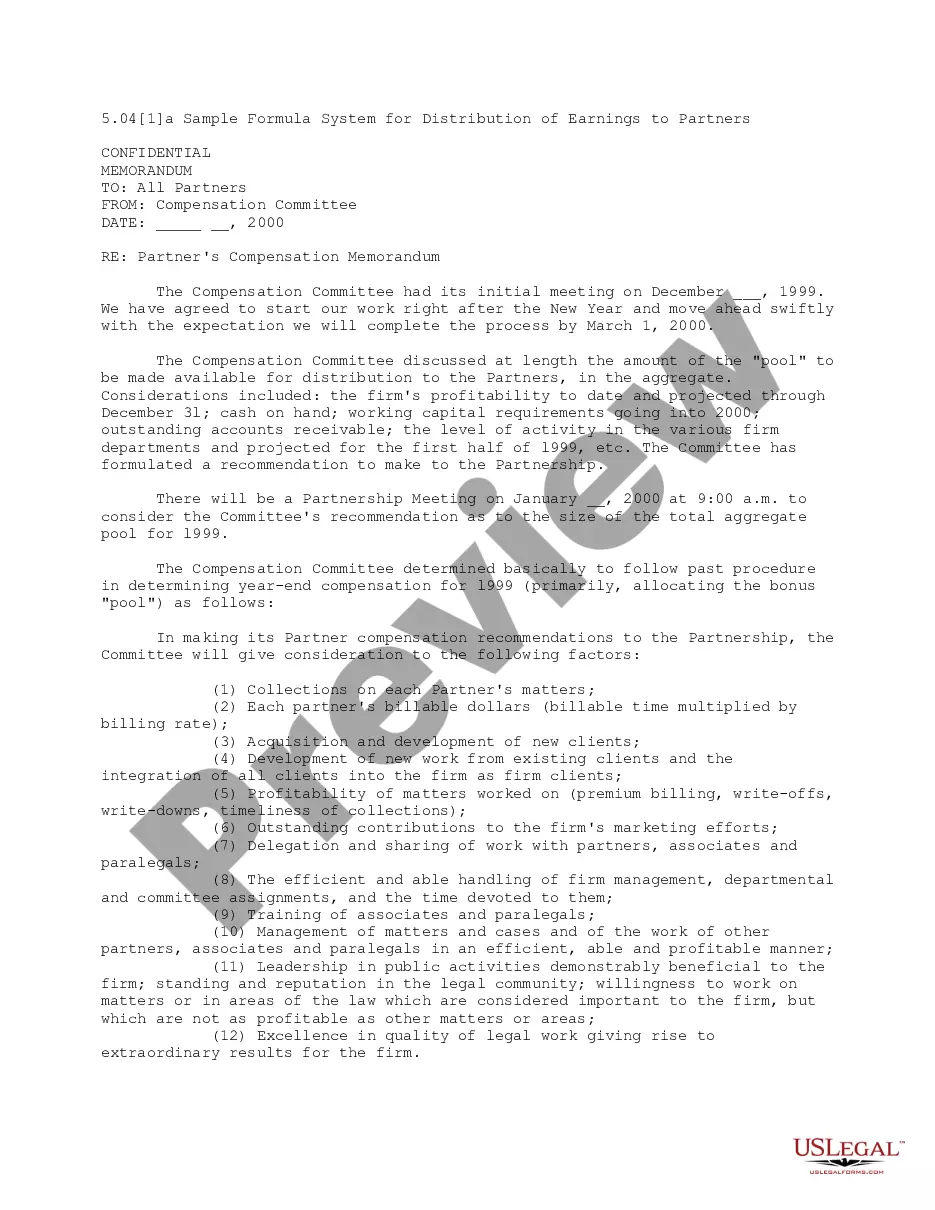

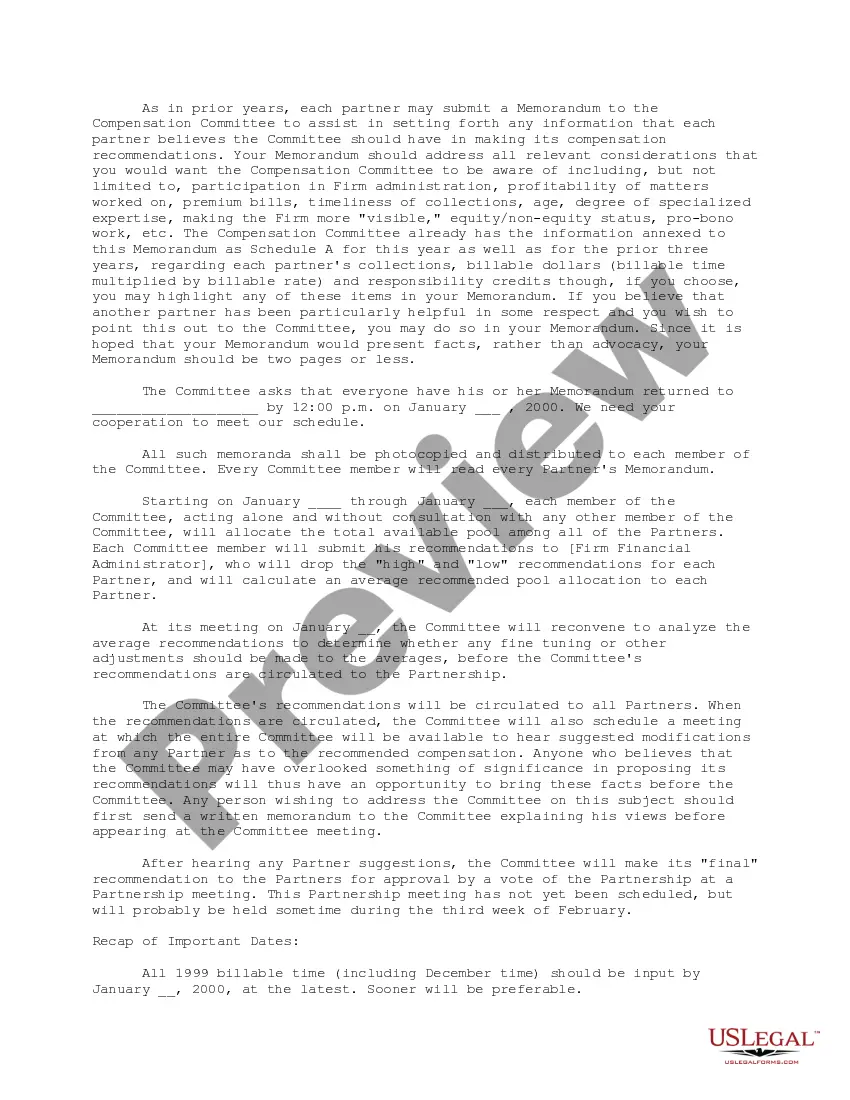

This Formula System for Distribution of Earnings to Partners provides a list of provisions to conside when making partner distribution recommendations. Some of the factors to consider are: Collections on each partner's matters, acquisition and development of new clients, profitablity of matters worked on, training of associates and paralegals, contributions to the firm's marketing practices, and others.

Cook Illinois Formula System for Distribution of Earnings to Partners is a method used by partnerships to distribute profits and losses among its partners. The formula takes into consideration several factors to allocate earnings in a fair and equitable manner. The Cook Illinois Formula System considers the following keywords and variables while calculating the distribution of earnings to partners: 1. Capital Contributions: The amount of initial investment made by each partner plays a crucial role in determining their share of profit or loss. Partners who have contributed more capital will generally receive a larger portion of the earnings. 2. Profit and Loss Sharing Ratios: The partnership agreement outlines the specific ratio or percentage in which the partners will share profits and losses. This ratio is typically based on various factors like the partners' contributions, experience, expertise, or the nature of their roles within the partnership. 3. Time and Effort: The time and effort devoted by each partner towards the partnership's activities can also affect the distribution of earnings. Partners who actively participate in the management and operations of the business may be entitled to a higher share of the profits. 4. Special Agreements: Partnerships may have specific arrangements or agreements that impact the distribution of earnings. These agreements can include provisions for performance-based bonuses, preferential profit sharing for certain partners, or additional compensation for bringing in new clients or business opportunities. 5. Additional Contributions: If a partner contributes additional resources or assets to the partnership, such as property or equipment, it may be considered when calculating the distribution of earnings. These additional contributions can increase a partner's stake in the profits. 6. Tax Allocations: The Cook Illinois Formula System also considers the tax implications for each partner. Partners with higher tax liabilities may receive a larger portion of the profits to offset their tax obligations. Different types or variations of Cook Illinois Formula System for Distribution of Earnings to Partners may exist depending on the specific partnership agreement. For instance, there might be variations in profit and loss sharing ratios, or additional factors considered in the formula. These variations are unique to each partnership and are generally agreed upon by the partners when forming the partnership or when amending the partnership agreement.Cook Illinois Formula System for Distribution of Earnings to Partners is a method used by partnerships to distribute profits and losses among its partners. The formula takes into consideration several factors to allocate earnings in a fair and equitable manner. The Cook Illinois Formula System considers the following keywords and variables while calculating the distribution of earnings to partners: 1. Capital Contributions: The amount of initial investment made by each partner plays a crucial role in determining their share of profit or loss. Partners who have contributed more capital will generally receive a larger portion of the earnings. 2. Profit and Loss Sharing Ratios: The partnership agreement outlines the specific ratio or percentage in which the partners will share profits and losses. This ratio is typically based on various factors like the partners' contributions, experience, expertise, or the nature of their roles within the partnership. 3. Time and Effort: The time and effort devoted by each partner towards the partnership's activities can also affect the distribution of earnings. Partners who actively participate in the management and operations of the business may be entitled to a higher share of the profits. 4. Special Agreements: Partnerships may have specific arrangements or agreements that impact the distribution of earnings. These agreements can include provisions for performance-based bonuses, preferential profit sharing for certain partners, or additional compensation for bringing in new clients or business opportunities. 5. Additional Contributions: If a partner contributes additional resources or assets to the partnership, such as property or equipment, it may be considered when calculating the distribution of earnings. These additional contributions can increase a partner's stake in the profits. 6. Tax Allocations: The Cook Illinois Formula System also considers the tax implications for each partner. Partners with higher tax liabilities may receive a larger portion of the profits to offset their tax obligations. Different types or variations of Cook Illinois Formula System for Distribution of Earnings to Partners may exist depending on the specific partnership agreement. For instance, there might be variations in profit and loss sharing ratios, or additional factors considered in the formula. These variations are unique to each partnership and are generally agreed upon by the partners when forming the partnership or when amending the partnership agreement.