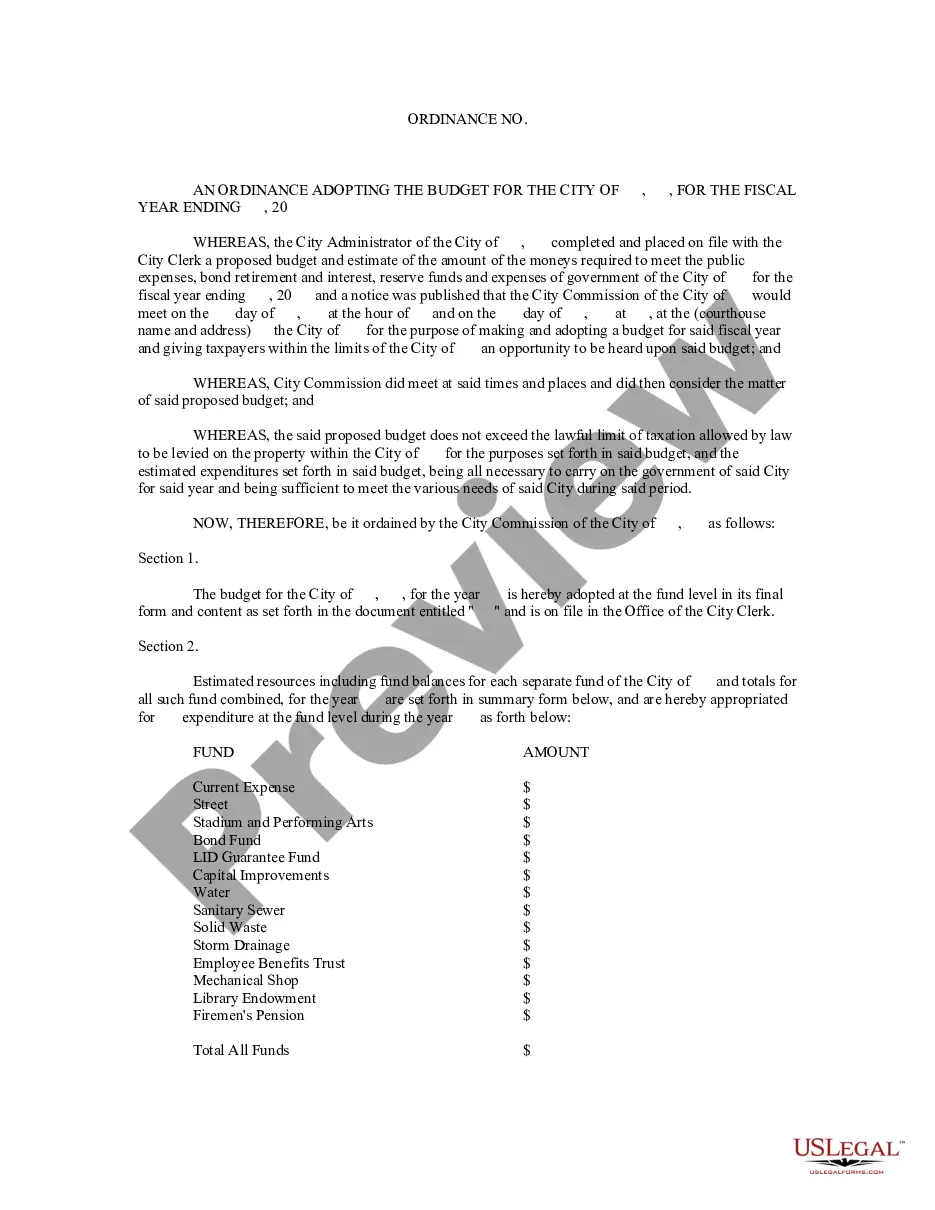

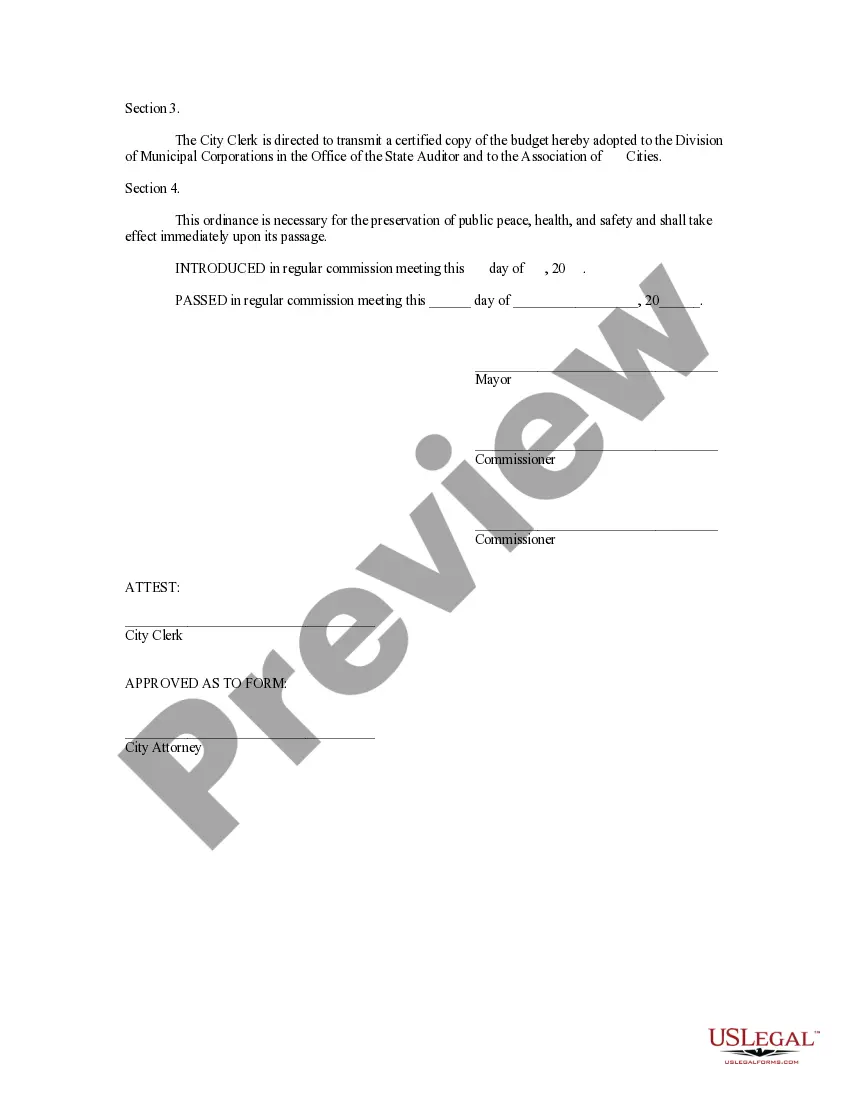

Hennepin Minnesota Ordinance Adopting the Budget is a crucial legislative process in Hennepin County, Minnesota, which outlines the financial plan for the upcoming fiscal year. This ordinance sets forth the allocation and distribution of funds to various departments, programs, and services to ensure the county's smooth functioning and the provision of essential services. Keywords: Hennepin Minnesota, ordinance adopting the budget, fiscal year, financial plan, allocation of funds, distribution of funds, departments, programs, services. This comprehensive ordinance typically consists of: 1. General Fund Budget: The General Fund Budget is the core component of the Hennepin Minnesota Ordinance Adopting the Budget. It covers the county's day-to-day operations and funds key services like public safety, parks and recreational facilities, transportation infrastructure, public health initiatives, and various administrative functions. 2. Special Revenue Funds: The Ordinance also addresses Special Revenue Funds allocated to specific programs or projects outside the general operations. These funds often come from restricted revenue sources, such as grants or dedicated taxes, and support initiatives like road maintenance or environmental conservation efforts. 3. Capital Improvement Plan (CIP): The CIP is a critical part of the Ordinance, outlining Hennepin County's long-term infrastructure investment strategy. It involves budgeting for large-scale construction projects, facility improvements, equipment purchases, and land acquisitions. 4. Debt Service: The Ordinance may include provisions related to debt service, addressing the repayment of outstanding bonds or loans taken by the county to finance capital projects in previous years. This ensures responsible financial management and accountability. 5. Budgetary Policies and Guidelines: Hennepin Minnesota Ordinance Adopting the Budget may include specific policies or guidelines related to appropriations. These guidelines help county departments in preparing their budget proposals, outline performance expectations, and ensure financial transparency and accountability. 6. Public Input and Review Process: The ordinance may outline the process for public input and review, allowing residents, community organizations, businesses, and other stakeholders to provide suggestions, concerns, or feedback. This ensures that the budget aligns with community needs and priorities. 7. Amendments and Approval: The Ordinance may detail the procedures for amendments to the budget proposal and the legal requirements for its final approval, typically involving the County Board of Commissioners or a similar governing body. In conclusion, the Hennepin Minnesota Ordinance Adopting the Budget outlines the financial framework for the county, determining how funds will be allocated across various departments, programs, and services. It encompasses multiple components such as the General Fund Budget, Special Revenue Funds, Capital Improvement Plan, debt service considerations, budgetary policies, and public input processes.

Hennepin Minnesota Ordinance Adopting the Budget

Description

How to fill out Hennepin Minnesota Ordinance Adopting The Budget?

Whether you plan to start your business, enter into an agreement, apply for your ID update, or resolve family-related legal issues, you must prepare specific paperwork meeting your local laws and regulations. Finding the correct papers may take a lot of time and effort unless you use the US Legal Forms library.

The platform provides users with more than 85,000 expertly drafted and verified legal documents for any personal or business occurrence. All files are collected by state and area of use, so picking a copy like Hennepin Ordinance Adopting the Budget is quick and straightforward.

The US Legal Forms website users only need to log in to their account and click the Download key next to the required template. If you are new to the service, it will take you a few more steps to get the Hennepin Ordinance Adopting the Budget. Follow the instructions below:

- Make sure the sample meets your individual needs and state law requirements.

- Look through the form description and check the Preview if available on the page.

- Utilize the search tab providing your state above to find another template.

- Click Buy Now to obtain the sample when you find the proper one.

- Choose the subscription plan that suits you most to continue.

- Sign in to your account and pay the service with a credit card or PayPal.

- Download the Hennepin Ordinance Adopting the Budget in the file format you prefer.

- Print the copy or complete it and sign it electronically via an online editor to save time.

Documents provided by our website are multi-usable. Having an active subscription, you can access all of your previously purchased paperwork at any moment in the My Forms tab of your profile. Stop wasting time on a endless search for up-to-date official documentation. Join the US Legal Forms platform and keep your paperwork in order with the most extensive online form collection!