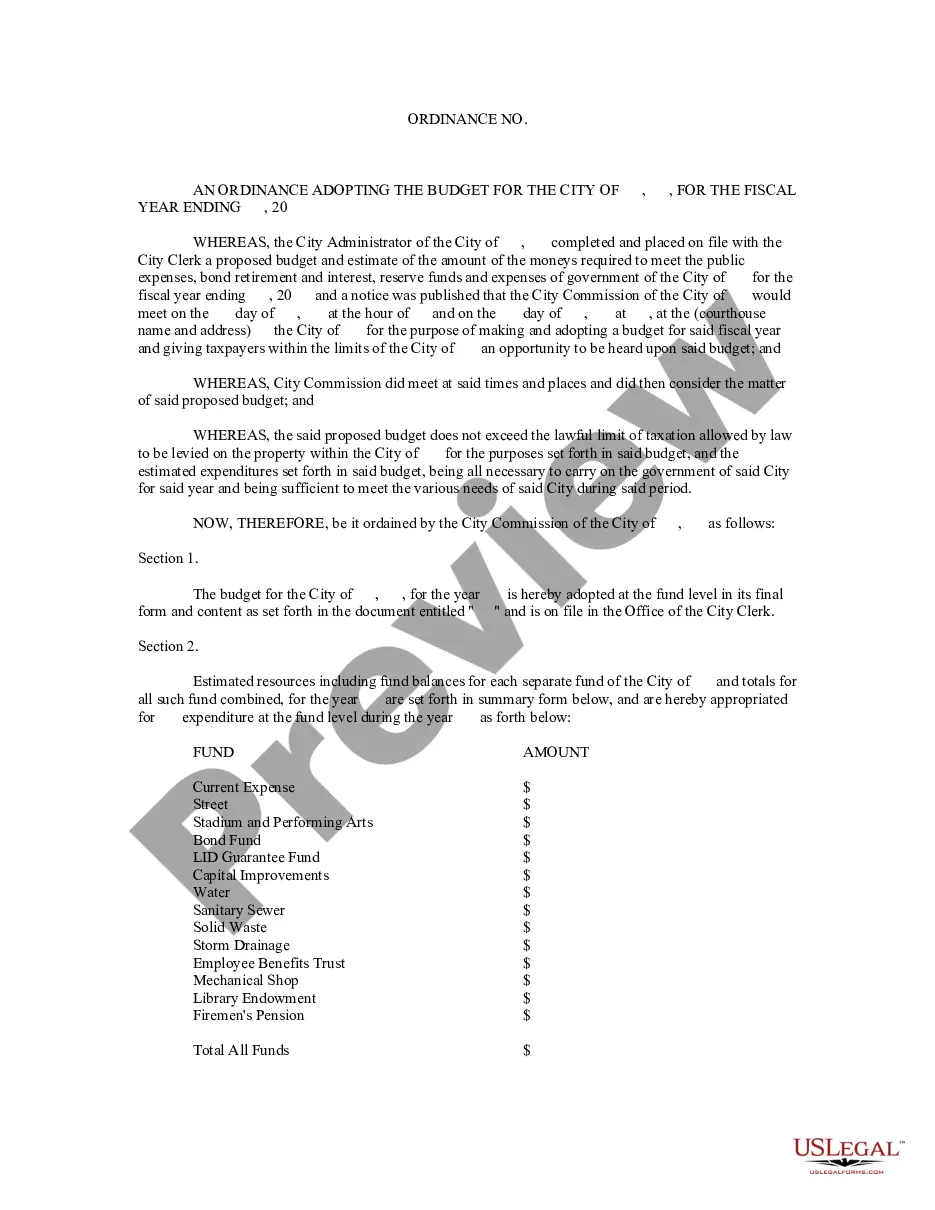

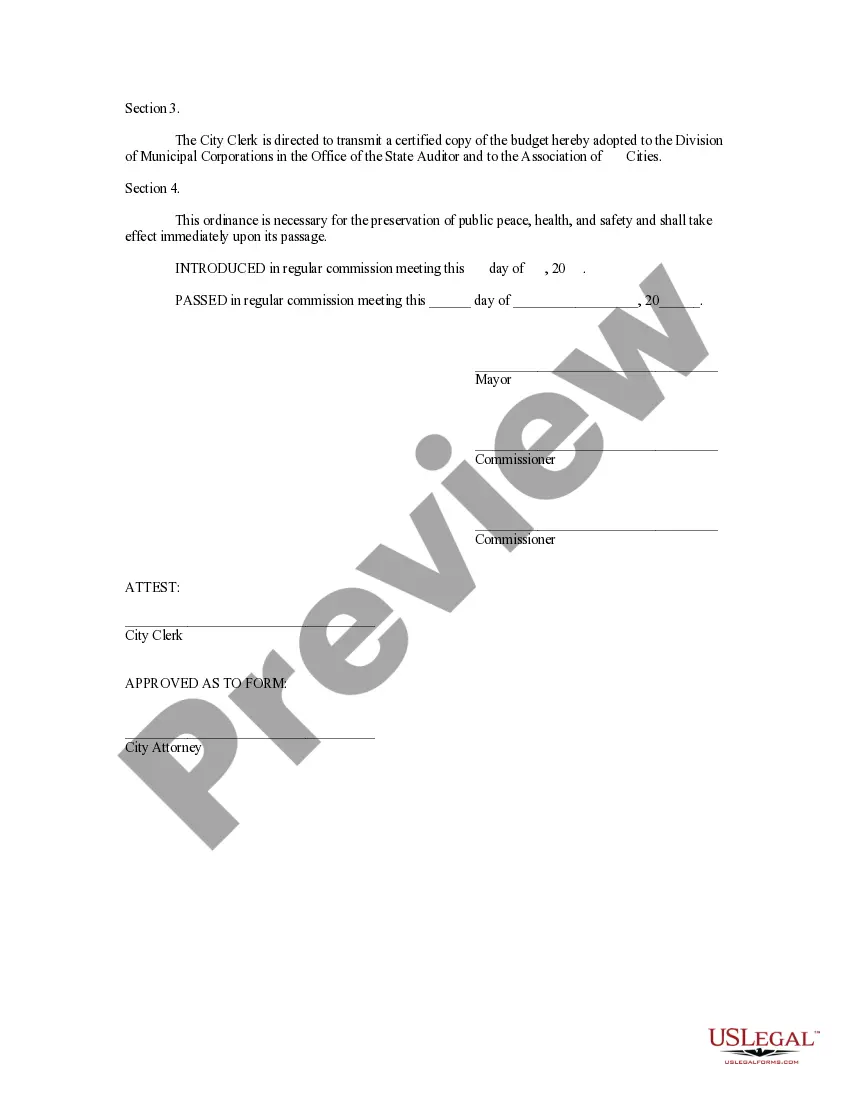

Oakland Michigan is a county located in the state of Michigan, United States. It encompasses several cities, townships, and various municipalities. The Oakland Michigan Ordinance Adopting the Budget is a legal document that outlines the process and regulations for approving and implementing the county's annual budget. This ordinance serves as a guiding framework for fiscal planning, revenue allocation, expenditure management, and resource allocation for the county government. It ensures transparency, accountability, and efficiency in financial decision-making processes. The Oakland Michigan Ordinance Adopting the Budget plays a crucial role in determining the allocation of funds to different departments, programs, and services within the county. The budget adoption process involves several stages, including budget preparation, review, and public hearings. The county government, under the guidance of elected officials and expert financial professionals, creates a comprehensive budget proposal that addresses the identified priorities and needs of the Oakland Michigan community. The Oakland Michigan Ordinance Adopting the Budget establishes the timeline and procedures for public input and participation. It outlines the different funds and accounts within the budget, such as general funds, special revenue funds, enterprise funds, and capital improvement funds. It also details the revenue sources, such as taxes, grants, fees, and intergovernmental transfers. Additionally, the ordinance may include provisions related to contingency funds, debt management, reserves, and other financial matters. It may address guidelines for budget amendments, carryovers, and appropriations. The Oakland Michigan Ordinance Adopting the Budget is a dynamic document that can change from year to year based on the changing needs, priorities, and economic conditions of the county. Types of Oakland Michigan Ordinance Adopting the Budget: 1. Annual Budget Ordinance: This type of ordinance adopts the annual budget for the upcoming fiscal year and is the most common and essential form of budget adoption. It provides a comprehensive overview of planned expenditures and revenue sources for the entire county. 2. Supplemental Budget Ordinance: In certain cases, amendments or adjustments to the approved annual budget may be necessary. A supplemental budget ordinance is adopted to incorporate these changes. It may address unexpected additional revenues, unforeseen expenses, or reallocation of funds within the existing budget. 3. Capital Improvement Budget Ordinance: This type of ordinance focuses specifically on the allocation of funds for capital projects, infrastructure development, and long-term investments. It outlines the priorities, funding sources, and timeline for these capital improvement projects. 4. Budget Appropriation and Transfers Ordinance: Sometimes, mid-year adjustments or transfers of funds between departments or programs become necessary. The budget appropriation and transfers ordinance provide guidelines and regulations for these changes, ensuring proper financial management and control. In conclusion, the Oakland Michigan Ordinance Adopting the Budget is a critical regulatory document that guides fiscal planning and resource allocation for the county government. It ensures transparency, accountability, and community involvement in financial decision-making processes. The different types of ordinances related to budget adoption address various aspects of financial management, including annual budgeting, amendments, capital projects, and fund transfers.

Oakland Michigan Ordinance Adopting the Budget

Description

How to fill out Oakland Michigan Ordinance Adopting The Budget?

A document routine always goes along with any legal activity you make. Opening a business, applying or accepting a job offer, transferring property, and many other life situations require you prepare formal paperwork that varies from state to state. That's why having it all collected in one place is so helpful.

US Legal Forms is the most extensive online library of up-to-date federal and state-specific legal forms. On this platform, you can easily locate and get a document for any personal or business objective utilized in your county, including the Oakland Ordinance Adopting the Budget.

Locating forms on the platform is remarkably straightforward. If you already have a subscription to our library, log in to your account, find the sample through the search field, and click Download to save it on your device. After that, the Oakland Ordinance Adopting the Budget will be available for further use in the My Forms tab of your profile.

If you are using US Legal Forms for the first time, adhere to this quick guideline to get the Oakland Ordinance Adopting the Budget:

- Make sure you have opened the correct page with your local form.

- Utilize the Preview mode (if available) and scroll through the sample.

- Read the description (if any) to ensure the template satisfies your needs.

- Search for another document using the search tab if the sample doesn't fit you.

- Click Buy Now once you find the required template.

- Select the appropriate subscription plan, then log in or create an account.

- Select the preferred payment method (with credit card or PayPal) to proceed.

- Choose file format and save the Oakland Ordinance Adopting the Budget on your device.

- Use it as needed: print it or fill it out electronically, sign it, and send where requested.

This is the simplest and most trustworthy way to obtain legal paperwork. All the templates provided by our library are professionally drafted and checked for correspondence to local laws and regulations. Prepare your paperwork and manage your legal affairs properly with the US Legal Forms!