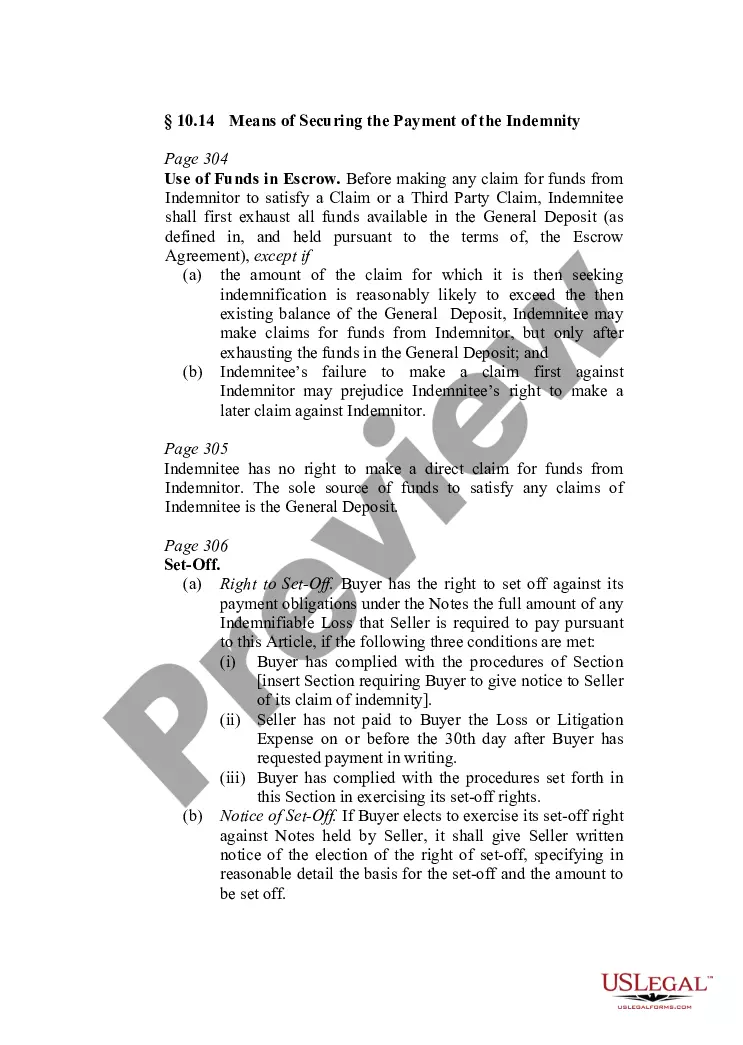

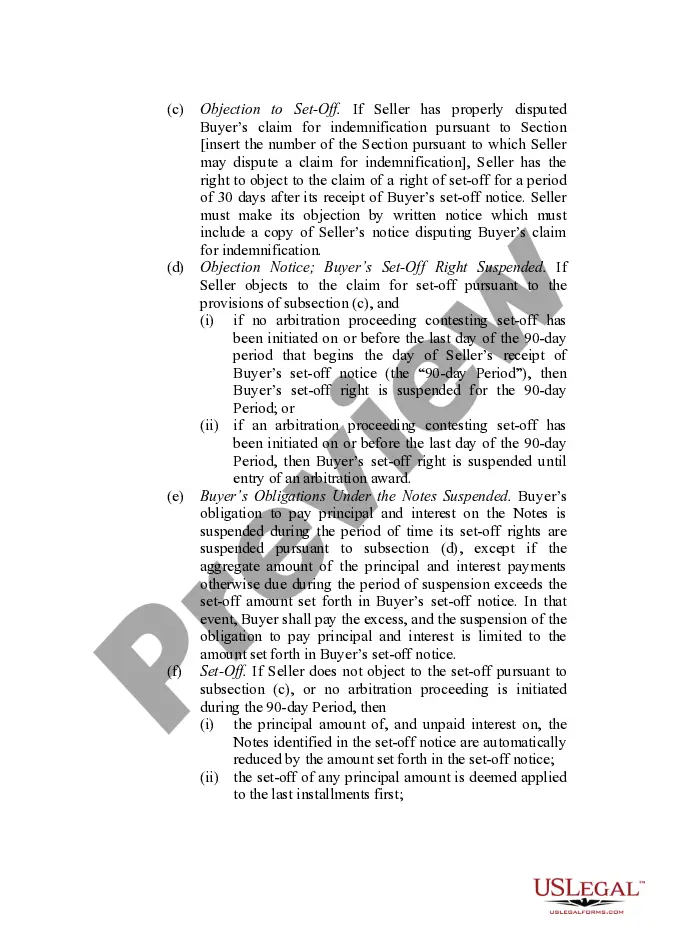

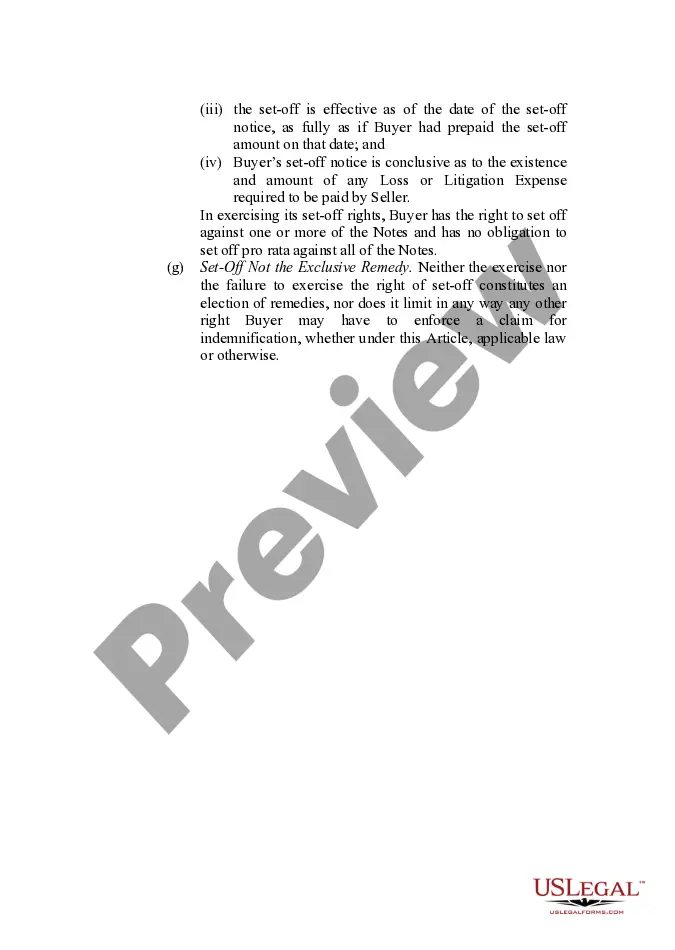

This form provides boilerplate contract clauses that outline means of securing the funds for payment of any indemnity, including use of an escrow fund or set-offs.

San Bernardino, California is a city located in the Inland Empire region of Southern California. It is known for its scenic beauty, rich history, and diverse culture. When it comes to indemnity provisions, San Bernardino has several means of securing the payment of indemnity. One commonly used type is financial security in the form of insurance. Many businesses and individuals in San Bernardino opt for insurance policies to protect themselves from potential liabilities or damages. These policies often include indemnity provisions that outline the extent of coverage and how claims should be handled. Another means of securing indemnity in San Bernardino is through contractual agreements. In various business transactions, parties may include indemnity provisions in their contracts to ensure that one party will be compensated if certain risks or losses occur. These provisions help allocate responsibilities and minimize financial risks by securing the payment of indemnity. Additionally, San Bernardino utilizes surety bonds for indemnity purposes. Surety bonds involve three parties- a principal, an obliged, and a surety company. The principal secures the bond to ensure that their obligations will be fulfilled, while the obliged is the entity or person who is protected by the bond. The surety company guarantees the performance of the principal and pledges to compensate the obliged if the principal fails to meet their obligations. San Bernardino's legal system also plays a crucial role in enforcing indemnity provisions. Courts and arbitration panels in the city provide a fair and neutral platform for parties to resolve disputes related to indemnity agreements. They ensure that the payment of indemnity happens according to the terms agreed upon by the parties involved. Overall, San Bernardino, California has multiple means of securing the payment of indemnity, including insurance, contractual agreements, surety bonds, and a robust legal system. These provisions aim to protect businesses and individuals from potential losses and ensure a fair and secure environment for conducting transactions.San Bernardino, California is a city located in the Inland Empire region of Southern California. It is known for its scenic beauty, rich history, and diverse culture. When it comes to indemnity provisions, San Bernardino has several means of securing the payment of indemnity. One commonly used type is financial security in the form of insurance. Many businesses and individuals in San Bernardino opt for insurance policies to protect themselves from potential liabilities or damages. These policies often include indemnity provisions that outline the extent of coverage and how claims should be handled. Another means of securing indemnity in San Bernardino is through contractual agreements. In various business transactions, parties may include indemnity provisions in their contracts to ensure that one party will be compensated if certain risks or losses occur. These provisions help allocate responsibilities and minimize financial risks by securing the payment of indemnity. Additionally, San Bernardino utilizes surety bonds for indemnity purposes. Surety bonds involve three parties- a principal, an obliged, and a surety company. The principal secures the bond to ensure that their obligations will be fulfilled, while the obliged is the entity or person who is protected by the bond. The surety company guarantees the performance of the principal and pledges to compensate the obliged if the principal fails to meet their obligations. San Bernardino's legal system also plays a crucial role in enforcing indemnity provisions. Courts and arbitration panels in the city provide a fair and neutral platform for parties to resolve disputes related to indemnity agreements. They ensure that the payment of indemnity happens according to the terms agreed upon by the parties involved. Overall, San Bernardino, California has multiple means of securing the payment of indemnity, including insurance, contractual agreements, surety bonds, and a robust legal system. These provisions aim to protect businesses and individuals from potential losses and ensure a fair and secure environment for conducting transactions.