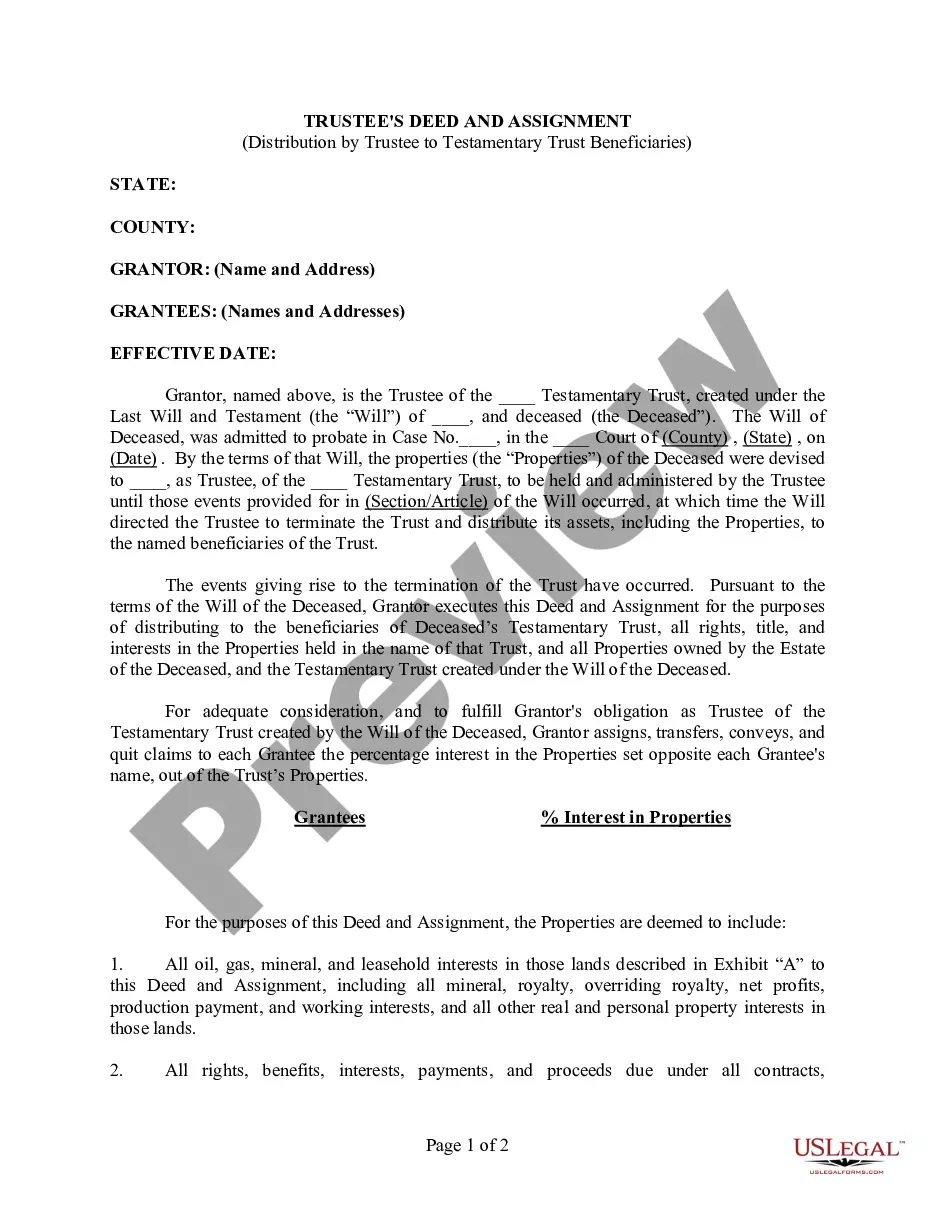

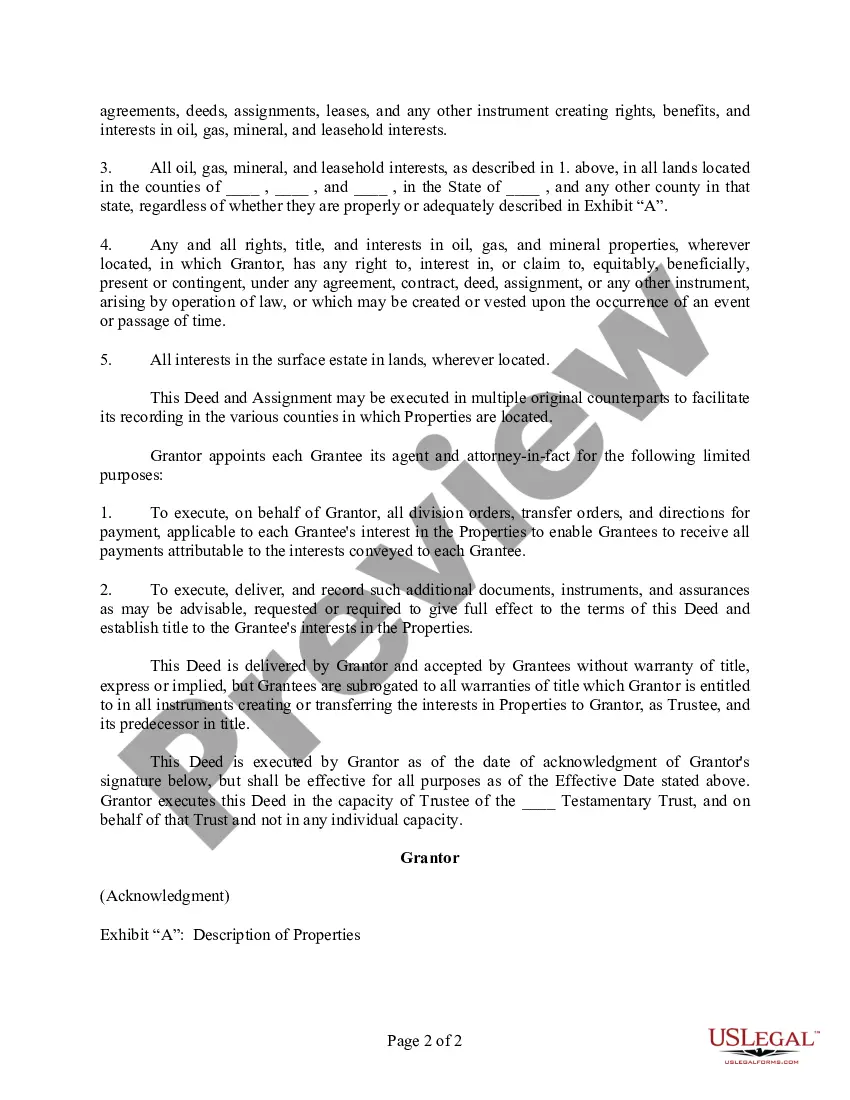

Orange California Trustee's Deed and Assignment for Distribution by Trustee to Testamentary Trust Beneficiaries

Description

How to fill out Orange California Trustee's Deed And Assignment For Distribution By Trustee To Testamentary Trust Beneficiaries?

Creating paperwork, like Orange Trustee's Deed and Assignment for Distribution by Trustee to Testamentary Trust Beneficiaries, to manage your legal affairs is a challenging and time-consumming task. A lot of cases require an attorney’s participation, which also makes this task not really affordable. Nevertheless, you can consider your legal affairs into your own hands and take care of them yourself. US Legal Forms is here to the rescue. Our website features more than 85,000 legal forms created for different cases and life circumstances. We ensure each document is in adherence with the laws of each state, so you don’t have to worry about potential legal issues associated with compliance.

If you're already aware of our website and have a subscription with US, you know how easy it is to get the Orange Trustee's Deed and Assignment for Distribution by Trustee to Testamentary Trust Beneficiaries form. Simply log in to your account, download the form, and personalize it to your needs. Have you lost your document? No worries. You can get it in the My Forms tab in your account - on desktop or mobile.

The onboarding flow of new customers is just as simple! Here’s what you need to do before downloading Orange Trustee's Deed and Assignment for Distribution by Trustee to Testamentary Trust Beneficiaries:

- Make sure that your template is specific to your state/county since the rules for writing legal documents may differ from one state another.

- Find out more about the form by previewing it or going through a brief description. If the Orange Trustee's Deed and Assignment for Distribution by Trustee to Testamentary Trust Beneficiaries isn’t something you were looking for, then use the header to find another one.

- Sign in or create an account to start using our service and download the form.

- Everything looks great on your end? Click the Buy now button and select the subscription option.

- Pick the payment gateway and enter your payment information.

- Your template is all set. You can try and download it.

It’s an easy task to locate and purchase the needed template with US Legal Forms. Thousands of organizations and individuals are already taking advantage of our rich library. Subscribe to it now if you want to check what other perks you can get with US Legal Forms!

Form popularity

FAQ

Distribute trust assets outright The grantor can opt to have the beneficiaries receive trust property directly without any restrictions. The trustee can write the beneficiary a check, give them cash, and transfer real estate by drawing up a new deed or selling the house and giving them the proceeds.

In the case of a good Trustee, the Trust should be fully distributed within twelve to eighteen months after the Trust administration begins.

The trustee can set up new brokerage accounts in the name of the beneficiaries, or the beneficiaries can create their own brokerage accounts at an institution of their choosing. The Trustee can then instruct that all stocks and bonds be transferred in-kind (meaning without being sold) to the Trust beneficiaries.

This law allows a trust to distribute appreciated assets in kind while treating them as having been sold. This way, the trust would in fact distribute stock, but would reap the benefit of its prior losses. And the distributed stock would take a basis for the beneficiary equal to the value on the date of distribution.

Notice to beneficiaries and heirs: If the trust becomes irrevocable when the settlor dies, the trustee has 60 days after becoming trustee or 60 days after the settlor's death, whichever happens later, to give written notice to all beneficiaries of the trust and to each heir of the decedent.

How does Testamentary Trust Taxation Work? Testamentary Trusts are taxed as a whole, though beneficiaries will not be forced to pay taxes on distributions from the Trust. Note that you could be responsible for the capital gains tax, depending on your state.

Allocating Capital Gains to Distributable Net Income in Estates and Trusts. A common question that arises when preparing an estate or trust return is, can capital gains be distributed to the beneficiary? Most often, the answer is no, capital gains remain in and are taxed at the trust level.

Real estate is deeded out of the trust and into the names of beneficiaries. Stocks and bonds can be transferred from the trust into the beneficiary's brokerage accounts. Beneficiaries typically have to pay taxes on trust income, except for distributions from the trust's principle.

In the case of a good Trustee, the Trust should be fully distributed within twelve to eighteen months after the Trust administration begins. But that presumes there are no problems, such as a lawsuit or inheritance fights.

Basis in the assets received by a beneficiary in a distribution from an estate or trust is the adjusted basis of the property in the hands of the fiduciary immediately before the distribution, adjusted for gain or loss recognized by the trust or estate, if any.